Review of Professional Management

Search

Search

Isha Narula1 and Kriti Dhingra1

1 Vivekananda Institute of Professional Studies, Pitampura, Delhi, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Global economic markets are encountering apprehensions and susceptibilities after the pandemic of COVID-19. Investment patterns are becoming restrained because of uncertain global scenarios and reduced GDP worldwide. World economies are moving towards digital era and investors are becoming more open towards the newest forms of investments. Due to the uncertain scenarios, investors globally are looking forward to some lucrative forms of investments and cryptocurrencies are the ray of hope for global investors. The present study is attempt to explore the changing dynamics of cryptocurrencies with the market uncertainties. Volatility of five cryptocurrencies, namely Bitcoin, Ethereum, XRP, Chainlink and Bitcoin Cash are analysed using the Generalised AutoRegressive Conditional Heteroskedasticity Model. Results showed that the investors preferred taking cautious decisions and invested more in famous bitcoin rather than other cryptocurrencies.

Cryptocurrency, volatility, GARCH, spillover

Introduction

The global outburst, COVID-19 which has been labelled a pandemic by the World Health Organisation (WHO) has significantly impacted economy of the world (Yarovaya et al., 2020). Sales of products declined, consumer behaviour changed, production reduced, organisations had financial burdens and there was increase in the unemployment rate worldwide (Lahmiri & Bekiros, 2020). Amid these circumstances, the financial market undoubtedly responded.

The revolutionary utopia that the technology growth promises seems to come closer at an astounding pace, yet unexpected challenges have come up. This pandemic has destabilised the entire world in the past few months, not only putting lives in danger but also plundering the economic well-being of deep-rooted global businesses and subsequently the world’s financial structure.

The world was not prepared for this global pandemic, not even back in 1918–1920 during the Spanish flu. But the difference between then and now lies in the fact the world has been more technologically sound, people can work remotely, shop online, have teleconsultations with a doctor through video calling and also buy digital currencies. Even before the onset of COVID-19, digital assets were maturing gradually. During the last decade, the evolution of a new currency called ‘cryptocurrency’ was seen.

In the past few years, ‘cryptocurrency market’ has attracted the attention of various investors, researchers and government (Makarov & Schoar, 2020; Nasir et al., 2019). The philosophy behind cryptocurrency lies in the famous quote by Richard Kovacevich, ‘banking is necessary, banks are not’ (Baur et al., 2018). Cryptocurrencies are an unruly payment mechanism which does not require any intermediation from the banks. They can be used by business organisations that use blockchain technologies for the production and circulation of cryptocurrencies. Therefore, cryptocurrencies are not measured by any central bank or government and they are not a part of the real economy (Böhme et al., 2015).

There has been a rapid increase in the size of the cryptocurrency market. The reasons behind this increase can be (Yousaf & Ali, 2020):

Now, financial sphere is more digitised and virtualised because of technological advancements, it is important that we are able to overcome the problem of dynamically predicting the cryptocurrency market. The tools used for predicting and modelling the cryptocurrency market need proper improvisation so that the distrust of the public for cryptocurrency as a pioneering financial asset can be duly managed (Danylchuk et al., 2020).

Cryptocurrency market is considered a volatile market, also a substantial portion of the purchase of cryptocurrency is considered speculations (Fry & Cheah, 2016). With the rising number of cryptocurrencies and the increase in market capitalisation of the cryptocurrency market (Ji et al., 2019) many studies have been conducted to understand the cryptocurrency market in terms of its volatility (Corbet et al., 2018; Liu, 2019; Liu & Tsyvinski, 2018). Moreover, cryptocurrency can also be seen as a commodity where people can benefit from the increase and decrease in value of the currency (Amanzholova & Teslya, 2018).

Despite the increasing interest of people in this form of money, many countries are not in the favour of its adoption. As of March 2018, five nations have received enactment that makes owning or executing cryptographic forms of money illicit. For instance, in 2017, Bangladesh banned Bitcoin and other virtual monetary forms. As per Bangladeshi law, exchanges utilising Bitcoin or other virtual monetary forms are unlawful, and violators are liable to a sentence of as long as 12 years in jail.

Despite having a mixed reaction to its advantages and disadvantages, cryptocurrencies have always drawn attention of many researchers. Previous studies have shown the cross-market volatilities between cryptocurrency market and other markets (Bouri et al., 2017; Gajardo et al., 2018). Thus far, from an investment point of view, it is vital to comprehend the altering aspects of the digital currency marketplace, especially how the cryptocurrency market’s efficiency got affected during the uncertainties in the market. This makes it significant to study the impact of one cryptocurrency on another cryptocurrency during such times.

Objectives of the Study

Literature Review

Many studies have been conducted to inspect the profits and instability transmission among various cryptocurrencies. Yi et al. (2018) studied the instability interconnection among 52 cryptocurrencies for estimating the high-dimensional VARs by making use of the LASSO-VAR approach. They found that the 52 cryptocurrencies were strongly interconnected and also analysed the volatility spillover from bitcoin to the supplementary cryptocurrencies.

Koutmos (2018) measured the volatility and return broadcast among the 18 foremost cryptocurrencies. He revealed that Bitcoin was the main contributor to volatility spillovers among the 18 cryptocurrencies. He also explained that the return and volatility spillovers had increased with time and also there can be spikes in the spillovers whenever there is any major news regarding cryptocurrencies.

Katsiampa (2019) employed the diagonal BEKK model and investigated the instability between Bitcoin and Ethereum. They found that cryptocurrencies in the cryptocurrency market were interdependent on each other, and their volatility and correlation were responsive to any major news event. They analysed that Ethereum could be a tough hedge in counter to Bitcoin.

Ji et al. (2019) studied the profits and unpredictability among six cryptocurrencies (Bitcoin, Ethereum, Ripple, Litecoin, Stellar and Dash) by applying the measures developed by Diebold and Yilmaz (2012) and found that Bitcoin followed by Litecoin was the net spreaders of Profits and instability to additional cryptocurrencies. Also, Ripple and Ethereum were the net receivers of the spillovers.

Katsiampa et al. (2019a) analysed the shockwave and instability spillover among three cryptocurrencies (Bitcoin, Litecoin and Ethereum) using the BEKKMGARCH model and found that there was bi-directional shock spill-over among Bitcoin and Ethereum, Bitcoin and Litecoin. Also, bi-directional volatility spill-over was pragmatic among Bitcoin and Ethereum, Bitcoin and Litecoin, and Litecoin and Ethereum pairs.

Canh et al. (2019) investigated the unpredictability undercurrents in the seven foremost cryptocurrencies Bitcoin, Stellar, Dash, Litecoin, Ripple, Monero and Bytecoin by using the DCC-MGARCH model and found that there was noteworthy volatility transmission between all seven cryptocurrencies. They also observed that structural breaks were present in all these cryptocurrencies and the shift in market capitalisation spreads from smaller to larger cryptocurrencies.

Liu and Serletis (2019) in their study examined the shockwave and insta- bility transmission across three foremost cryptocurrencies, namely Bitcoin, Litecoin and Ethereum. They used the Generalised AutoRegressive Conditional Heteroskedasticity (GARCH) in the mean model to conduct their study and found that there was substantial shock and volatility spillover among the three of them.

Beneki et al. (2019) applied the BEKK-GARCH modelling procedure to explore the instability transmission among Bitcoin and Ethereum. They found a one-directional instability transmission from Ethereum to Bitcoin.

Motivation of the Study and Research Gap

In times of the pandemic of COVID-19, investors worldwide were in state of confusion and dilemmas about investment decisions. As the future looks very gloomy and investors are losing confidence in stocks of even renowned and well-established companies, cryptocurrencies can be a ray of hope for investors to bag profits. At present times, investors are looking for a safer and more profitable form of investment where they feel more secure and confident. In such uncertain financial and economic scenarios, this study is an attempt to understand the role of cryptocurrency as potential investment avenue. The study majorly focuses on the performance and predictability of cryptocurrency with the help of the GARCH model. The researchers have tried to explore the changes in volatility patterns pre- and during-COVID times. Such shifts in volatility will also contribute to assessing the behavioural shifts of investors.

On the basis of the literature review, it could be observed that many researchers are working to study the spill-overs among cryptocurrencies throughout a phase of the crisis. Numerous researchers have observed the instability spill-over among various assets such as a bond, equity and commodity during a crisis period (Aloui et al., 2011; Bekaert et al., 2014; Diebold & Yilmaz, 2009) but the cryptocurrencies have still not been investigated. Therefore, this literature gap will be addressed by our study.

Research Methodology

The contemporary research has discovered the behaviour of volatility of selected five cryptocurrencies, namely Bitcoin, Ethereum, XRP, Chainlink and Bitcoin Cash with the help of GARCH (p,q) model. The purpose of selecting these five cryptocurrencies is that they are the top five traded cryptocurrencies. The study is considering the scenario of pre and during COVID-19. As per WHO’s report, the first case of COVID-19 was detected in December 2019. So, the data prior to December 2019 are considered to be pre-COVID and data after December 2019 are considered to be during-COVID. The study is an attempt to understand the shift in the volatility behaviour of the selected cryptocurrencies because of pandemic. The two-year daily cryptocurrency prices are taken from coinmarketcap.com ranging from 1 December 2018 to 30 November 2019 (pre-COVID) and 1 December 2019–30 November 2020 (during-COVID).

The market prices are changed into returns with the support of the subsequent formulary:

![]() (1)

(1)

Here, Rt designates revenues at period t, whereas Pt and Pt–1 are the prices of the cryptocurrencies at period t and t–1. The stability of the data has been weighed by employing Augmented Dickey–Fuller (ADF) Test. The Null Hypothesis of ADF test conditions that ‘Return has Unit Root’. This hypothesis has been forbidden during all the regimes selected for all the currencies.

Model Advancement for Cryptocurrency Return Volatility (Degree of Modification in the Construction of Conditional Volatility)

GARCH (1,1) Model

The architype of GARCH (p,q) model is originated by Bollerslev (1986) who acclaims that conditional variance of the revenues generated by any stock or currency is directly related to its previous conditional variance and squared values of its previous error terms. Conditional mean equation of GARCH (1,1) prototype is detailed as follows:

![]() (2)

(2)

Conditional volatility prototype is demonstrated as follows:

(3)

(3)

In Equation (2), Rt is the revenue derived from the prices of cryptocurrencies. Here, α can be defined as the influence of previously logged revenues on present revenues. In the present prototype, εt is independently and identically distributed. Which again states that the error terms have stable variance and zero mean. Equation (3) explains the conditional variance, and ht is the conditional variance of εt. Here the value of εt demonstrates a constant fluctuation throughout the selected time frame. α1 demonstrates the impact of recent news on today’s revenues. This phenomenon is also acknowledged as ‘news coefficient’ and popularly identified as ARCH effect in financial history. Another constant identified as β1 in the prototype also significantly influence the performance of the currency. This is prevalently acknowledged as ‘persistent coefficient’ or the ‘GARCH effect’. This outcome explores the influence the older information on the cryptocurrency. The GARCH (p,q) prototype, explores both ARCH (p) and GARCH (q) effects.

In this contemporary research, GARCH model is implied to inspect the movement of instability or the consequences of volatility spillover among the cryptocurrencies in pre-COVID and during-COVID regimes. To extract the results, the residual series of the cryptocurrencies is derived and furthermore it is squared. The series is squared with the purpose of eradicating the negative influence. The residual of the cryptocurrency data which is squared afterwards is positioned as shockwave instigator in the volatility prototype as a regressor. The coefficients of these shockwave instigators are significant as well as validate spillover effect transmitting among the cryptocurrencies.

GARCH (1,1) model to validate spillover effect is having subsequent stipulations:

(4)

(4)

The prototype mentioned above recognises ht which symbolises conditional variance of the cryptocurrency. This ht is regressed and also a function of mean identified as ω0. Here, α1 is the function of ‘news coefficient’ and β1 is the function of ‘persistence coefficient’. Furthermore, ψ signifies the residual of cryptocurrency. This residual series of cryptocurrency is placed in variance equation as a shockwave instigator.

The typical GARCH (1,1) archetypal takes up a symmetrical reply of instability in the direction of ‘good’ and ‘bad’ newscasts.

Data Analysis

The contemporary segment of the research debates the outcomes of the tests run on the pre- and during-COVID phases/regimes.

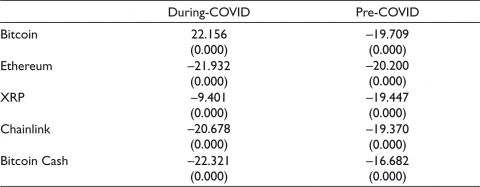

Table 1 depicts the outcomes of the unit root test on the returns of five selected cryptocurrencies, namely Bitcoin, Ethereum, XRP, Chainlink and Bitcoin Cash. The data have been selected in two phases, pre-COVID and during COVID. Pre-COVID period ranges from 1 December 2018 to 30 November 2019 and during-COVID period ranges from 1 December 2019 to 30 November 2020. The data have been reported stationary on observing the results of unit root test on selected five cryptocurrencies in two phases.

Table 1. Results of Unit Root Test.

Notes: Pre-COVID: 1 December 2018–30 November 2019.

During-COVID: 1 December 2019–30 November 2020.

Table 2 demonstrates the result of volatility spillover in pre-COVID period ranging from 1 December 2018 to 30 November 2019. The study has considered five cryptocurrencies, namely Bitcoin, Ethereum, XRP, Chainlink and Bitcoin Cash. For each cryptocurrency, the volatility spillover from the rest of the four cryptocurrencies has been assessed. On observing the outcome, Bitcoin returns have been influenced by the volatility of Ethereum (0.648) and XRP (0.033). Ethereum’s returns have been affected by Bitcoin (0.519), XRP (0.679) and Bitcoin Cash (0.1004 at 10% level of significance) respectively. XRP’s returns have been affected by Ethereum (0.561) and Bitcoin Cash (0.054). Chainlink’s returns are influenced by Bitcoin (–0.043), Ethereum (–0.080), XRP (0.135) and Bitcoin Cash (0.011). Bitcoin Cash’s returns are influenced by Ethereum (1.067) only. The ARCH effect has been observed on all the cryptocurrencies except Ethereum, whereas GARCH effect has been reported on Ethereum (–0.039) and Chainlink (1.003). The results report that recent news affects the returns of all the currencies except Ethereum whereas persistency effect is only visible in two cryptocurrencies. Chainlink is one of the most vulnerable currencies which is getting influenced by all the other cryptocurrency and demonstrate both ARCH and GARCH effect. Bitcoin, XRP and Bitcoin Cash are the least vulnerable and do not get affected by maximum number of cryptocurrencies. For investors, Ethereum can be one of the good investments as it is not as vulnerable as Chainlink and not as indifferent as Bitcoin, XRP and Bitcoin Cash. Most of the significant spillovers are directly impacting the returns of respective cryptocurrencies except Ethereum (–0.080) on Chainlink and GARCH (–0.039) effect on Ethereum.

Table 2. Volatility Spillover of Cryptocurrencies in Pre-COVID (from 1 December 2018 to 30 November 2019).

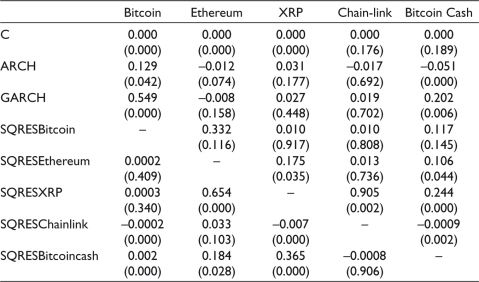

Table 3 demonstrates the outcomes of spillover effect among the designated five cryptocurrencies during the time frame ranging from 1 December 2019 to 30 November 2020. This regime has been identified as during-COVID period. On observing the outcome, it is identified that Bitcoin is affected by Chainlink (–0.0002) and Bitcoin Cash (0.002), although the impact is very minimum. Ethereum is influenced by XRP (0.654) and Bitcoin Cash (0.184), XRP is affected by Ethereum (0.175), Chainlink (–0.007) and Bitcoin Cash (0.365). On observing the results of Chainlink, it has been reported that only XRP (0.905) could influence its returns. Ethereum (0.106), XRP (0.244) and Chainlink (–0.0009) have significantly influenced the returns of Bitcoin Cash. ARCH effect also known as new effect has been observed on Bitcoin (0.129), Ethereum (–0.012) and Bitcoin Cash (–0.051). GARCH effect also known as persistency effect is observed on Bitcoin (0.549) and Bitcoin Cash (0.202).

Table 3. Volatility Spillover of Cryptocurrencies in During-COVID (from 1 December 2019 to 30 November 2020).

It has been discovered that Chainlink is one of the cryptocurrencies which is getting volatility spillover only from XRP but affecting the returns of all the cryptocurrencies except Bitcoin. Hence, Chainlink’s volatility can be employed to predict the reruns of other cryptocurrencies. Bitcoin Cash is one of the most vulnerable cryptocurrencies among all the five as it is getting volatility spillover from Ethereum, XRP and Chainlink and also reporting ARCH and GARCH effect. Bitcoin can be a good investment opportunity as it is not as vulnerable as Bitcoin Cash but can also be predictable in comparison to others.

Findings of the Study

The present study is an attempt to explore the impact of the pandemic on the cryptocurrencies. In recent times, it has been observed that investors’ focus has shifted to digital currencies instead of traditional forms of investment. The study has identified a shift in the behaviour of investors due to pandemic where the impact of recent information has been reduced and investors are a little less sensitive to recent piece of information, whereas older news was not that significant in pre-COVID times also. Bitcoin is one of the most popular forms of cryptocurrency in the history of cryptocurrencies. One of the major findings of the study states that earlier investors were exploring other forms of cryptocurrencies, for example, Ethereum and Chainlink as these cryptocurrencies were receiving volatility spillover from maximum number of cryptocurrencies. But the scenario has been completely transformed due to COVID. During-COVID Bitcoin Cash, XRP and Bitcoin are receiving volatility spillover from maximum number of cryptocurrencies. A major shift has been observed in Chainlink as in pre-COVID times it received volatility spillover from rest of the four cryptocurrencies and during-COVID times it received volatility spillover only from XRP. The study confirmed that the pandemic has made the investors more cautious about their investments and they do not want to invest their money in less reliable forms of investments.

Conclusion and Implications of the Study

On comparing the pre- and during-COVID results, ARCH effect has been reduced from four to three cryptocurrencies. Ethereum has been demonstrating ARCH effect during-COVID times, whereas earlier it was not showing any impact of the recent news. GARCH effect has been observed on two currencies earlier while it is still visible on two cryptocurrencies only, whereas in pre-COVID times it was observed on Ethereum and Chainlink and during-COVID times it is observed on Bitcoin and Bitcoin Cash. It can be seen that during COVID times investors have switched to the most famous cryptocurrency rather than putting their money in other forms of investments. This investor behaviour shows that investors want to play safe in the market by just investing in renowned investment avenues. The study also contributes to understanding the role of investor sentiments while selecting any form of investment. The present scenario has forced the investors to go for most reliable form of cryptocurrencies while earlier investors were more open to newer forms of investments. The present scenario has made them more vulnerable and cautious.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Kriti Dhingra  https://orcid.org/0000-0002-4137-9550

https://orcid.org/0000-0002-4137-9550

Aloui, R., Aïssa, M. S. B., & Nguyen, D. K. (2011). Global financial crisis, extreme interdependences, and contagion effects: The role of economic structure? Journal of Banking & Finance, 35(1), 130?141.

Amanzholova, B. A., & Teslya, P. N. (2018, October). Threats and opportunities of cryptocurrency technologies [Paper Presented]. 2018 XIV International Scientific-Technical Conference on Actual Problems of Electronics Instrument Engineering (APEIE) (pp. 335?339). IEEE.

Baur, D. G., & Dimpfl, T. (2018). Asymmetric volatility in cryptocurrencies. Economics Letters, 173, 148?151.

Bekaert, G., Ehrmann, M., Fratzscher, M., & Mehl, A. (2014). The global crisis and equity market contagion. The Journal of Finance, 69(6), 2597?2649.

Beneki, C., Koulis, A., Kyriazis, N. A., & Papadamou, S. (2019). Investigating volatility transmission and hedging properties between Bitcoin and Ethereum. Research in International Business and Finance, 48, 219?227.

Böhme, R., Christin, N., Edelman, B., & Moore, T. (2015). Bitcoin: Economics, technology, and governance. Journal of Economic Perspectives, 29(2), 213?238.

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 33, 307?327.

Bouri, E., Jalkh, N., Molnár, P., & Roubaud, D. (2017). Bitcoin for energy commodities before and after the December 2013 crash: Diversifier, hedge or safe haven? Applied Economics, 49(50), 5063?5073.

Canh, N. P., Wongchoti, U., Thanh, S. D., & Thong, N. T. (2019). Systematic risk in cryptocurrency market: Evidence from DCC-MGARCH model. Finance Research Letters, 29, 90?100.

Corbet, S., Meegan, A., Larkin, C., Lucey, B., & Yarovaya, L. (2018). Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters, 165, 28?34.

Danylchuk, H., Kovtun, O., Kibalnyk, L., & Sysoiev, O. (2020). Monitoring and modelling of cryptocurrency trend resistance by recurrent and R/S-analysis [Paper presentation]. E3S Web of Conferences (Vol. 166, p. 13030). EDP Sciences.

Diebold, F. X., & Yilmaz, K. (2009). Measuring financial asset return and volatility spillovers, with application to global equity markets. The Economic Journal, 119(534), 158?171.

Diebold, F. X., & Yilmaz, K. (2012). Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting, 28(1), 57?66.

Fry, J., & Cheah, E.-T. (2016). Negative bubbles and shocks in cryptocurrency markets. International Review of Financial Analysis, 47, 343?352.

Gajardo, G., Kristjanpoller, W. D., & Minutolo, M. (2018). Does Bitcoin exhibit the same asymmetric multifractal cross-correlations with crude oil, gold and DJIA as the Euro, Great British Pound and Yen? Chaos, Solitons & Fractals, 109, 195?205.

Ji, Q., Bouri, E., Lau, C. K. M., & Roubaud, D. (2019). Dynamic connectedness and integration in cryptocurrency markets. International Review of Financial Analysis, 63, 257?272.

Katsiampa, P. (2019). Volatility co-movement between Bitcoin and Ether. Finance Research Letters, 30, 221?227.

Katsiampa, P., Corbet, S., & Lucey, B. (2019a). Volatility spillover effects in leading cryptocurrencies: A BEKK-MGARCH analysis. Finance Research Letters, 29, 68?74.

Koutmos, D. (2018). Return and volatility spillovers among cryptocurrencies. Economics Letters, 173, 122?127.

Lahmiri, S., & Bekiros, S. (2020). The impact of COVID-19 pandemic upon stability and sequential irregularity of equity and cryptocurrency markets. Chaos, Solitons & Fractals, 138, 109936.

Liu, J., & Serletis, A. (2019). Volatility in the cryptocurrency market. Open Economies Review, 30(4), 779?811.

Liu, W. (2019). Portfolio diversification across cryptocurrencies. Finance Research Letters, 29, 200?205.

Liu, Y., & Tsyvinski, A. (2018). Risks and returns of cryptocurrency (Nr. 0898?2937). National Bureau of Economic Research.

Makarov, I., & Schoar, A. (2020). Trading and arbitrage in cryptocurrency markets. Journal of Financial Economics, 135(2), 293?319.

Nasir, M. A., Huynh, T. L. D., Nguyen, S. P., & Duong, D. (2019). Forecasting cryptocurrency returns and volume using search engines. Financial Innovation, 5(1), 2.

Weber, B. (2016). Bitcoin and the legitimacy crisis of money. Cambridge Journal of Economics, 40(1), 17?41.

Yarovaya, L., Brzeszczynski, J., Goodell, J. W., Lucey, B. M., & Lau, C. K. (2020). Rethinking financial contagion: Information transmission mechanism during the COVID-19 pandemic. Journal of International Financial Markets, Institutions and Money, 79(C). https://doi.org/10.1016/j.intfin.2022.101589

Yi, S., Xu, Z., & Wang, G. J. (2018). Volatility connectedness in the cryptocurrency market: Is Bitcoin a dominant cryptocurrency? International Review of Financial Analysis, 60, 98?114.

Yousaf, I., & Ali, S. (2020). Discovering interlinkages between major cryptocurrencies using high-frequency data: New evidence from COVID-19 pandemic. Financial Innovation, 6(1), 1?18.