Review of Professional Management

Search

Search

Rinku Manocha1

1 Department of Commerce, Hindu College, University of Delhi, Delhi, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

South, Southeast and East (S, SE and E) Asian economies comprise a number of emerging economies that are significantly contributing to the world market. Asian economies are coming up with strong policy frameworks to strengthen trade and investment. Simultaneously, Asian economies (S, SE and E regions) are strategically negotiating a number of vital intra-regional as well as extra-regional trade agreements (RTAs) with an intent to not only boost trade but also to provide an environment for investors to stimulate foreign direct investment (FDI) flows. The study examined the trends and dynamics of regional integration, trade and investment in the said Asian region. The trend for RTAs indicates that economies in S, SE and E Asian regions have negotiated a significant number of bilateral and plurilateral trade agreements. Moreover, export values of three significant RTAs (Association of Southeast Asian Nations [ASEAN], Asia Pacific Trade Agreement [APTA], and South Asian Association for Regional Cooperation [SAARC] trading bloc) in the region suggest that export performance of ASEAN and APTA vis-à-vis intra-bloc and the world at large has been far better than the SAARC trading bloc. The dynamics of trade and investment suggest that East Asian economies are contributing a significant percentage to world trade and investment, and Southeast Asian economies are slowly improving trade and investment trends. However, Southern Asian economies need to revisit and revamp existing trade and investment policies to gear up trade and investment flows.

Trade, FDI, trade agreements, Asian

Introduction

Each economy is unique having distinctive features in terms of geographical distribution, cultural heritage, historical diversity, technological development and political arrangements (Shu, 2018). Economies either produce or import (Thirlwall & Gibson, 1992) depending upon the indigenous expertise of an economy. In the case of expertise, economies prefer self-production whereas economies do import wherein limitations associated with domestic production are viewed. Hence, a global market for trade and investment is inevitable. In addition, to facilitate the global market, economies world over are working towards reducing trade barriers. Moreover, globalisation wave has encouraged economies world over to actively participate in trade agreements (Bhasin & Manocha, 2014), tax treaties, investment treaties and other measures to boost the global market. Trade agreements and investment treaties not only act as a tool of navigating foreign markets but also provide benefits associated with reduction of barriers (tariff and non-tariff).

‘The World Trade Organization (WTO1) is the only global international organisation dealing with the rules of trade between nations’. Regional trade agreements (RTAs) (also popularly known as free trade agreements [FTAs]) are trade agreements negotiated under the aegis of WTO among nations to liberalise tariff and non-tariff barriers to facilitate the flow of goods and services. Hence, RTAs are building blocks (Baldwin, 2006). With the changing dynamics on the world map RTAs currently negotiated under WTO not only cover trade-related liberalisation measures but also capture the norms to stimulate investment and service flows among nations. New age RTAs are getting expanded and hence ‘new regionalism’ era (Cihelkova & Frolova, 2014; Cihelková & Hnát, 2008) can be identified and, therefore, more coverage and attributes can be stated as follows:

Therefore, economies across the globe can experience various advantages, namely, reduction in the price associated with distribution and consumption of goods and services; ease in the flow of factors of production, goods and associated services; extended markets; and better trading mechanisms across the globe which in turn has promoted global productivity and supply chains (Thomas, 2014). Moreover, trade blocs have been promoting an environment wherein the members of a bloc are encouraged to jump the boundaries of the partner countries (due to supportive policy measures among the members of a bloc) and, hence, stimulate investment along with trade (Park & Park, 2008). Hence, trade blocs are platforms that promote trade and investment-friendly environment among member nations.

Rationale of the Study

Following the world trends (post-liberalisation era), Asian economies have also taken a number of initiatives to stimulate trade and investment via various policy measures and, hence, have actively participated in the formation of various intra-regional and extra-RTA. As per the Asian economic integration report (ARIC, 2023), Economic Union (EU) and North American intra-regional trade remained stagnated over the last three decades whereas Asia’s intra-regional trade has witnessed a steady rise. Further, the report stated that Asian global value chains and regional value chains have seen a massive boost in the said region. Hence, a linkage in trade; production process; investment opportunities; capital flows; liberalisation measures; and deeper economic integrations are gaining momentum. In the given scenario, Asian economies are significantly contributing to trade, investment and other macroeconomic variants. As per Finance and Development2 (a quarterly magazine of IMF), Asia is emerging as one of the key players in the world economy with three major (China, Japan and India) boosting economies and with a share of more than 35% of the world’s GDP. Workman (2022) suggested that Asian economies accounted for USD 8.512 trillion in exports to the world in 2021 leading to a growth of 34.1% growth of Asian exports since 2017. Similarly, as per ESCAP-75 (2019), the share of Asia-pacific world FDI (foreign direct investment) inflow share has dropped to 35% (in 2019) from 45% (in 2018) and FDI outflow share has decreased to 41% (in 2019) from 52% (in 2018) but the region still manages to bag the largest share of world FDI flows. Further, as per ESCAP (2021), Asia has emerged as the top most destination for FDI inflows as China (in East Asia) and India (in South Asia) have seen a rise of 23% and 20% since the last two decades. Therefore, to study the changing dynamics of emerging economies of Asia, the coverage of our study extends to identify the role, nature and trends of trade, investment and trade agreements for South, Southeast and East (S, SE and E) Asian economies.

Literature Review

The present study attempts to examine the trends and changing dynamics of trade, investment and trade agreements in S, SE and E Asian economies. Therefore, we divide our LR into three subsections, namely, studies examining trade trends; studies capturing investment trends; and studies roping trends of RTAs.

Studies Capturing Trade Trends

We were able to have our hand on a few studies that have examined trade trends for country-specific and region-specific sample sizes. Starting with the studies examining country-specific trade trends. Adebayo (2019) examined the trade trends and policies for Nigeria over the period of 1981–2017, and the results depicted that trade trends are compatible with sustainable development of Nigeria. Rafiq et al. (2016) evaluated the trends of trade balances for Pakistan over the period of 1972–2015 and the forecasts suggested that policymakers need to work towards improving trade balances. Shree and Sridhar (2016) evaluated the trends of livestock products for India over the period of 20 years and stated that both the exports and imports of livestock products have increased for India largely due to an increase in income and changes in the preference for dairy products. Kunze (1972) evaluated the trends of trade between Britain and Eastern EU countries over the period of 1960–1971. The results suggested that the rise in trade is largely due to consistent efforts on the part of Britain’s government and Britain’s corporate houses. Islam (2019) captured the trends of trade between Bangladesh and India over the period of 2009–2016 and concluded that India holds a strong place in Bangladesh’s international trade. Taneja et al. (2019) explored India-Pakistan trade trends over the period of 2012–2017 and suggested that informal channels rather than formal channels are dominating India-Pakistan trade. Manocha and Bhasin (2022) studied the trends of India-UK trade over the period of 1991–2021 and stated that both counties are strategically working to enhance trade.

Few studies have also captured the trends of trade with region-specific sample sizes. Dimitris and Pinna (2013) examined the trade trends between the EU and its neighbouring economies over the period of 1991–2011 and stated that the EU can explore exponential trade with its neighbouring countries in the years to come. Similarly, Oehler-Sincai (2009) explored the trends and structure of trade-in-goods for EU countries over the period of 2004–2008 and indicated that EU trade is more inclined towards manufacturing goods both for exports and imports. Straubhaar (1986) explored the nature and trends of trade between developing economies over the period of 1969–1983. Borin et al. (2018) examined the world trade trends over the period of 2011–2016 and suggested that cyclical factors have contributed to weakness in world trade. Similarly, Nikoloski and Paceskoski (2015) evaluated the trends of world trade over the period of 1937–2013.

Studies Capturing the Investment Trends (FDI Trends)

Like trade, investment-related trends have also been explored by a few researchers both for country-specific and region-specific sample sizes. Sahiti et al. (2020) examined the trends of FDI inflows for Kosovo over the period of 2006–2017 and concluded that FDI received in Kosovo is catering to business sector, rental sector and real estate. Ergano and Rambabu (2020) examined the pattern and trends of FDI inflows of Ethiopia from India and China over the period of 1997–2016. Molla (2018) studied the trends of FDI for Bangladesh over the period of 2008–2018 and suggested that FDI inflows are significantly contributing towards the sectors that are contributors of economic growth. Bista (2017) explored the trends of FDI inflows for Nepal over the period of 1982–2007 and suggested that liberalisation and privatisation measures are contributing towards FDI inflows in Nepal. Rao and Dhar (2011) studied the trends of FDI inflows for India and stated that liberalisation policies and mergers and acquisitions have strengthened FDI flows for India.

Regional-specific FDI flows have also been explored by a few researchers. Chattopadhyay et al. (2022) examined the trends of FDI inflows for BRICS economies over the period of 1990–2020 and concluded that BRICS economies need to bring better and enhanced reforms to attract FDI inflows in future. Similarly, Bose and Kohli (2018) examined the trends of FDI for BRICS economies over the period of 1990–2015. Hattari and Rajan (2008) evaluated the trends of FDI inflows into developing Asian economies and stated that developing economies are emerging hubs for FDI inflows. Daisuke (2006) evaluated outwards FDI from Association of Southeast Asian Nations (ASEAN) economies and intraregional ASEAN investment trends and suggested that ASEAN countries are emerging as regional and global players of FDI. Like global trade trends, global investment trends have also been examined by a few researchers. Banik and Bhaumik (2006) evaluated the global FDI trends and concluded that FDI inflows and outflows are enhancing the world over but the growth rate of FDI inflows has declined in 2003 as compared to FDI inflows in 2000. Fischer (2000) examined the global FDI trends since 1990 and suggested that economic integrations are supporting interdependent production and service networks and, hence, an increase in FDI trends on the world map can be seen.

Studies Associated with Trends of RTA

This section of the literature review captures studies that have discussed the trends of RTAs. Haokip (2012) examined the trends of RTAs for India starting from the end of the Cold War and stated that India’s Look East policy is the result of India’s attempt to expand regional integrations with East and Southeast Asian countries. Sapkota et al. (2018) examined the trends of RTAs in the Asian region over the period of 1990–2015 using a sample of 34 Asian countries and revealed that integrations are increasing within Asian region. Kirillov and Paweta (2014) examined the changing trends of work economic integrations and the study employed a few major RTA and concluded that countries that are geographically near and with similar economic development tend to form unions. Sakakibara and Yamakawa (2003) examined the challenges and opportunities of regional integration in East Asia and stated that the East Asian region is stimulating both global and intra-regional RTAs. Park et al. (2021) examined the integrations in the Asian and European regions and stated that Asian economies are opting for loose cooperation whereas the European region is strengthening institutionalisation with a single currency setup. Kawai and Wignaraja (2010) evaluated the trends and challenges of FTAs in the Asian region and suggested that political considerations are required to come up with better and strong FTAs in the said region.

An insight into the literature indicates that studies have either captured trends for trade, or investment, or RTAs by employing varied sample sizes. Talking about the Asian region, both country-specific and region-specific studies are accessible. Rafiq et al. (2016) evaluated trade trends for Pakistan; Islam (2019) studied the trade trends between India and Bangladesh. Similarly, Molla (2018) studied the FDI trends for Bangladesh; Bista (2017) explored the FDI trends for Nepal; Rao and Dhar (2011) studied the FDI trends for India. Further, Hattari and Rajan (2008) evaluated the FDI trends for developing Asian economies. Sapkota et al. (2018) and Kawai and Wignaraja (2010) examined the trends of RTAs in the Asian region. But an aggregate study capturing the trends for trade, investment and RTAs for S, SE and E Asia was not found; therefore, the current study attempts to capture the changing dynamics of trade, investment and regional integrations in the said region.

Data Source

To study the trends and changing dynamics of RTAs in S, SE and E Asian regions vis-à-vis trade, investment and trade agreements, the data was collected from varied sources. RTA-associated data was collected from the WTO database over the period of 1991–2022. To gather intra-ASEAN, intra-SAARC (South Asian Association for Regional Cooperation), intra-APTA (Asia Pacific trade agreement) export values, data was collected from the trade map (ITC) database over the period of 2002–2021 (based on the availability of data). To study the regional flow of imports and exports, data was collected from the UNCTAD database over the period of 1991–2021; and to study the trends of FDI inflows and outflows of S, SE and E Asian region, data was gathered from FDI statistics UNCTAD database over the period of 1991–2021.

Scope of the Study

To study the changing dynamics of S, E and SE Asian trade and investment markets since 1991, the current study intents to talk down the trends of trade, investment and trade agreements in the said region. Moreover, the study aims to study the changes in the nature (quantity and quality) of trade agreements in the region. Hence, we can list the objectives of the study as follows:

Trade Agreements (Trade Blocs) in S, E and SE Asian Regions

Trade agreements are negotiated to stimulate trade, liberalise trade barriers and enhance market access (Mukherjee et al., 2019). Countries negotiating trade agreements under the umbrella of WTO have an intent to provide more and better access to the member countries of the bloc towards the domestic market vis-à-vis the rest of the world. However, trade agreements may differ in nature/type depending on the extent and depth of liberalisation among the member countries (World Bank, 2005). The most elementary and easily negotiable trade agreement is FTA wherein the member countries opt to liberalise tariff barriers among the member nations either for a few or all goods. The next level of integration can be associated with Custom Union (CU). CUs are like FTA but member nations part of CU further extend the liberalisation measures and tend to enforce common trade policies among the member nations. As compared to FTA, CUs are more difficult to conclude. The next stage of integration is associated with Common Market (CM) wherein not common trade policies are structured but also a free movement of labour and capital among the bloc members is promoted. Though CM requires a major negotiation platform, this stage of integration provides no restriction on immigration, emigration and cross-border free movement of labour and capital among member countries. A deeper stage of integration in form of the EU can also be recognised. EU supports a common monetary and fiscal policy among nations of the bloc and supports identical tax structures, fixed exchange rates, free currency convertibility and free movement of capital for all members of the bloc. The last and deepest stage of integration is associated with Political Union (PU). With PU, member countries tend to form a common government and single constitution, but a major dilution of the sovereignty and democratic rights of the member countries is registered. Apart from the above-stated integration, Partial Scope Agreements (PSA) are also negotiated under the umbrella of WTO. PSA also known as preferential trade agreements (PTA) are like FTA wherein the member nations try to reduce tariff barriers for a few products rather than all traded products. In addition to the above, EIAs are also noted with WTO that cover trade in services, unlike FTAs that are largely associated with trade in goods. Figure 1 depicts a pictorial representation of various trade agreements based on the stage (and nature) of integration.

Figure 1. Stages of Integration.

Each stage of integration has its own attributes and advantages, and with the depth of integration more intra-bloc liberalisation among the members of the bloc can be seen. As per WTO,3 currently (as of 31st March 2022) 354 trade agreements are in force that corresponds with 577 notifications and separating counting goods, services and accessions. The sizeable number of RTAs on the world map indicates an urge among the economies to open gates for investment, goods, services and various other parameters of the global market. Further, the new generation (currently) RTAs that are more diversified in nature and have coverage of not only trade-in-goods but also other dimensions of the global market such as trade-in-services, environment and investment provisions (Wu et al., 2017) are seen.

Following the world trends, a diverse range of RTAs are also negotiated (and are in force) in the Asian subcontinent where a number of emerging economies (India, China, Japan, Korea, Singapore, Thailand, etc.) are trying to strengthen growth parameters vis-à-vis world at large and, hence, are coming with a reasonable number of intra-regional as well as extra-regional RTAs. More than 100 RTAs are negotiated (and in force) in S, SE and E Asia (see Table 1).

Table 1. RTAs Negotiated (and in Force) in South, Southeast and East Asia (Cumulative Year-Wise 1991 Onwards).

Source: Based on the data collected from the WTO RTA database.

An upsurge in the number of RTAs negotiated in the region indicates an environment that boosts trade, investment, economic growth and social welfare. A number of significant bilateral (Japan-India, Republic of Korea-India, Japan-Malaysia, Japan-Indonesia and many more) and multilateral (ASEAN, APTA, SAPTA, RCEP [Regional Comprehensive Economic Partner]) RTAs have been negotiated in the said region. Furthermore, the countries within S, SE and E Asia are not only negotiating intra-regional RTAs but are also actively participating in negotiating RTAs with economies world over/cross-regional (Japan-UK, New Zealand and Japan-Australia). Moreover, Asian economies are looking for deepening the existing integrations, SAPTA (a regional bloc among SAARC countries) formed FTA, South Asian Free Trade Agreement (SAFTA) in 2006 and similarly, ASEAN expanded its country coverage in 2022 to form RCEP. As per World Bank,4 regional integrations world over are getting deeper and more expanded, and hence are better devices for trade and non-trade cost reduction and global supply chain boosters (de Melo et al., 2020). They are also coming up with a cross-country policy balancing platform, especially for member countries. Furthermore, to stimulate economic growth, Asian economies are trying to minimise divergence. As per the WTO database, Asian economies are registering as the second largest hub of RTAs followed by European countries. Therefore, they are actively stimulating the quality and quantity of RTAs, bilateral investment treaties, investment and environment agreements, and EIA in the said region.

As the study tries to briefly capture the changing dynamics of regional integration in S, SE and E Asian regions therefore few subsections have also been captured to discuss the emerging and existing RTAs region-wise (SE, S and E Asia). Therefore, the study tabulates and discusses the number of RTAs negotiated (and in force) for countries within the regions under study and also tries to talk about significant and grooming RTAs in S, SE and E Asia. To identify countries within each region, the United Nations’ geographical regional classification has been opted for. Table 2 tabulates countries region wise.

Table 2. Region-Wise Countries.

Source: Based on data collected from the UN geographical regional classification.

RTAs in Southeast Asia

The Southeast Asian region is not only acting participating in strengthening trade and investment relations but also significantly contributing towards negotiating some vital RTAs both intra- and extra-regional (such as ASEAN, RCEP and others). Table 2 depicts the countries that constitute Southeast Asia, and Table 3 tabulates the number of RTA in force and negotiated country wise within Southeast Asian economies. Table 3 depicts that not only Singapore has negotiated the highest RTAs in SE Asia but countries such as Brunei, Myanmar, Laos, Vietnam, Malaysia, Thailand and Philippines are also following the race with 10 or even more than 10 RTAs negotiated as of 30th September 2022.

Table 3. RTAs Negotiated by Southeast Asian Economies (as of 30th September 2022).

Source: Based on the data collected from the WTO RTA database.

Furthermore, 10 leading economies of Southeast Asia have negotiated a vital RTA, ASEAN Free Trade Area (AFTA) in 1992. AFTA was initially negotiated among six Southeast Asian economies, namely, Brunei Darussalam; Malaysia; Indonesia; Thailand; Philippines; and Singapore but subsequently, Vietnam became part of ASEAN in 1995; Laos and Myanmar joined in 1997; and Cambodia entered in 1999. Currently, ASEAN has 10 signatories from the Southeast Asian region, namely, Brunei Darussalam; Laos; Philippines; Malaysia; Indonesia; Singapore; Thailand; Vietnam; Myanmar; and Cambodia. Furthermore, as of 30th September 2022, ASEAN is one of the signatories of six vital RTAs, out of which one is plurilateral RTA (ASEAN-Australia-New Zealand negotiated and in force since 2010) and five are bilateral RTA, namely, ASEAN-China (in force since 2005); ASEAN-India (in force since 2010); ASEAN-Japan (in force since 2008); ASEAN-Hong Kong, China (in force since 2019) and ASEAN-Republic of Korea (in force since 2010). ASEAN countries are stretching their arms to cover various intra-regional as well as extra-regional economies to facilitate trade (and investment) in compatible environment.

ASEAN has also worked upon various expansion forums, namely, RCEP (a platform for ASEAN+6) and ASEAN plus three (APT) (China, Japan and the Republic of Korea). APT is currently a cooperation forum initiated to address the financial crisis in the East Asian region and the forum is committed to taking care of issues such as energy, reduction of economic inequalities, inter-country labour mobility, poverty concerns, environmental and sustainability issues, transnational criminal activities and many more.5

However, RCEP was a step ahead to further strengthen Southeast economies and to provide more meaning to ASEAN economic potentials. Japan took the lead to establish a trade agreement among 10 ASEAN members and 6 vital economies. In 1992 at the ASEAN summit, negotiations for RCEP formally began. RCEP was initially proposed FTA among ASEAN and six emerging economies, namely, Japan; China; New Zealand; Australia; India; and Republic of Korea. However, India stayed away from the RCEP, and RCEP came into force (in 2022) with 15 countries (10 ASEAN and Japan; China; New Zealand; Australia; and the Republic of Korea). With RCEP, the socio-economic coverage of ASEAN enhanced as RCEP covers 30% of the world population and accounts for 30% of the world GDP6 leading to the formation of a strong regional integration in the Asian Continent.

RCEP came into force in 2022; therefore, potential gains and growth of the regional bloc can be studied in the years to come. However, currently, we can tabulate intra-ASEAN exports, and ASEAN export trends vis-à-vis world at large. A tabulation (see Table 6) of intra-ASEAN exports suggests that ASEAN exports among ASEAN economies have grown around 4.02 times since 2002. Moreover, intra-ASEAN exports account for around 20% of ASEAN world exports in 2021. Though the agreement has large regional diversity among member nations but intra-ASEAN export trends indicate that the agreement is likely to emerge as one of the most durable and successful RTA in the years to come (Hill & Menon, 2010).

RTAs in East Asia

People’s Republic of China; Republic of Korea; Mongolia; Japan; and Taiwan constitute Eastern Asian economies. The region carries three most significant economies, namely, China; Korea; and Japan. These three economies are leading the tally of RTAs negotiated in the region (see Table 4).

Table 4. RTAs Negotiated by Southeast Asian Economies (as of 30th September 2022).

Source: Based on the data collected from the WTO database.

As of 30th September 2022, these three major economies of the East Asian region have negotiated more than 15 RTAs individually (see Table 3 and Table 4). Furthermore, China; Republic of Korea and Japan have bilateral RTAs with ASEAN and are also members of currently negotiated (in 2022) RCEP. Such trends suggest an intent of Eastern Asian economies to extend trade liberalisation measures towards all neighbouring economies of Asia and even, collaborate with cross-continent economies to negotiate trade agreements. The trends also suggest that East Asian economies are looking for better trade partners to emerge as vital and strong economies of Asia. Eastern region also accounts for various significant intra-regional as well as extra-regional RTAs namely, China-Singapore; Japan-Korea; and many more. However, countries like Mongolia and Taiwan still need to gear up towards trade progressive measures.

RTAs in Southern Asia

As per UN geographical regional division, India; Afghanistan; Iran; Bangladesh; Bhutan; Maldives; Nepal; Sri Lanka; and Pakistan comprise of South Asia.

Tabulation (see Table 5) of RTAs in South Asia depicts that India has negotiated the largest number of RTAs and, currently, India is member of 20 trade-in-goods agreements and 8 trade-in-services agreements. Countries like Afghanistan and Maldives are still struggling to open gates for trade liberalisation and, hence, have negotiated very few RTAs as of 30th September 2022. Furthermore, in comparison to Southeast and East Asian economies, the South Asian region has negotiated lesser RTAs but almost all South Asian economies are members of the SAARC trading bloc. SAARC was a political platform formed in 1985 to stimulate regional strength and economic synergy among South Asian economies. SAARC was initiated with an intent to provide a political and economic forum for South Asian economies to build a strong, healthy and progressive environment in the region. However, in 1995, SAARC countries decided to initiate trade liberalisation measures and, hence, negotiated a PTA, SAPTA (Chowdhury, 2005). SAPTA came into force in December 1995 and had seven member nations of South Asia as its members (Bangladesh; Bhutan; India; Maldives; Nepal; Pakistan; and Sri Lanka). To further boost growth, SAARC countries in 2006 negotiated an FTA, South Asian Free Trade Area (SAFTA). SAFTA was a deeper integration wherein all members agreed to systematically reduce trade duties. In 2007, Afghanistan joined the SAARC club and became the eighth member of SAFTA. The key aspect of SAFTA formation was to promote the tariff liberalisation program wherein the member countries were committed to substantially reduce and remove tariff structure among the bloc members (Raghurampatruni et al., 2021). Table 6 shows that the intra-SAARC export value has increased 10 times in 2021 since 2002 but the intra-SAARC export to the world export is still as low as 7%. Currently (in 2021), total intra-SAPTA exports amount to 39 million USD of which India contributed 30.7 million USD.7 Hence, India contributes around 78.7% (in 2021) of intra-SAPTA exports (a significant share). India holds a predominant position in SAARC and is highly committed to the bloc (Jain, 2005), which might be because India is one the largest and emerging market of Asia. Moreover, the bloc’s contribution to world exports is too insignificant (only 7%) as the bloc is highly exposed to political and cross-border disturbances (Gauchan & Sarin, 2018).

Table 5. RTAs Negotiated by South Asian Economies (as of 30th September 2022).

Source: Based on the data collected from the WTO database.

Table 6. A Comparative Tabulation of Intra-SAARC, Intra-APTA and Intra-ASEAN Exports (2002–2021).

Source: Based on the data collected from www.trademap.org.

The study also talks about a plurilateral trade agreement, APTA negotiated between a few countries of South, Central and East Asian regions. APTA also known as the Bangkok agreement is one of most effectively operational and oldest PSA (Manocha, 2018) negotiated in June 1976. The agreement had Bangladesh, Korea, India, Sri Lanka and Laos as its original signatory member, and China joined APTA in 2002. APTA has drawn the best of three major markets in Asia, namely, India; Republic of Korea; and China. The bloc is working well towards developing a trade and investment-supportive environment. Table 6 reflects that intra-AFTA exports have grown 10 times in 2021 since 2002 and APTA exports to the world have been 10.2% in 2021.

Figure 2.Trends of Trade (X+M) and RTAs for S, SE and E Asia.

Source: Based on the data collected from the WTO database and the UNCTAD database.

Table 6 also provides a comparative tabulation of intra-SAARC, intra-ASEAN and intra-APTA exports since 2002. The trends of intra-bloc(s) indicate that intra-bloc export growth rate of APTA and ASEAN is much more than the intra-SAARC export growth. Table 6 also summarises the percentage of intra-bloc exports as a percentage of world exports for each bloc under study. The trends show a significant upsurge in the share of ASEAN followed by APTA and SAARC. However, Asian economies still need to strengthen the intra-bloc operations to generate better trends of exports in the years to come. In the nutshell, we can state that S, E and SE Asian economies are fast promoting trade via negotiating meaningful and significant RTAs (both bilateral and plurilateral) but the magnitude and impact of each RTA for exports is varied. ASEAN is fast expanding and growing RTA with intra-ASEAN export as 20% of total world exports (in 2021), whereas SAARC exports to world export is just 7%.

Trade and Investment in South, Southeast and East Asia

This section of the article talks about the trends of trade and investment in S, SE and E Asia. Trends of RTA along with the changing dynamics of trade and investment will help us to understand changing markets and economic structures of Asian economies. This section tabulates the trends of trade (export and import) and investment (inward and outward stock) for the region under study. We also try to provide a pictorial trend of trade and RTA, and investment and RTA for S, SE and E Asian regions.

Trade Trends in South, Southeast and East Asia

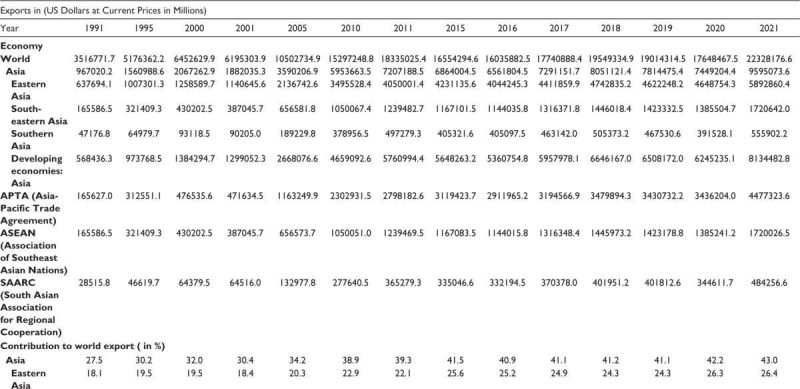

This subsection captures the trends of exports and imports in the S, SE and E Asian regions. Starting with the exports, Table 7 depicts that Asian share in world export has grown from 27.5% (in 1991) to 43% (in 2021), and S, SE and E Asian regions have been consistently contributing around 80% of total Asian exports since 1991. Hence, Asian countries (especially S, SE and E Asian countries) are significantly contributing to the world exports and S, SE and E Asian economies have the lion’s share of Asian exports. Trends also depict that East Asian exports to world exports have also grown from 18.1% (in 1991) to 26.4% (in 2021). Similarly, an upsurge in Southeast Asian exports to world exports from 4.7% (in 1991) to 7.7% (in 2021) has been seen. However, the share of South Asian exports to world exports has been insignificant and, hence, a growth of only 1.2% since 1991 (in aggregate 2.5% in 2021) is registered.

Table 7. Export and Import Trends of South, Southeast and East Asian Regions (1991–2021).

Source: Based on the data collected from the UNCTAD database.

Similar trends for imports were also depicted. Table 7 depicts that Asian imports as a percentage of world imports have also grown to 39.1% (in 2021) as compared to 25% (in 1991). Like exports, imports of S, SE and E Asian regions have been around 85% of Asian imports since 1991. A remarkable growth in East Asian imports to world imports is registered, and a rise from 15.2% (in 1991) to 23% (in 2021) is seen. However, the share of world imports of Southeast Asia and South Asia in 2021 has been 7.2% and 3.6% (2021) respectively. The trends of imports and exports for the said region of Asia have been more or less the same.

Hence, we can summarise the reason for growth of exports and imports in S, SE and E Asian regions as follows:

The region is opening gates for trade with intra-Asian economies as well as the rest of the world and, hence, boosting trade-related infrastructure, trade-supportive policies and tariff reduction measures via negotiating significant RTAs both intra-regional and extra-regional to fetch trade for the region. A pictorial representation of RTA and trade trends of S, SE and E Asian are depicted in Figure 2.

A rising trend for both RTAs and trade (export and import) for S, SE and E Asian regions can be seen. However, the rise in the number of RTAs negotiated in the region is steady during the last 30 years (starting from 1991) but for trade small variations are depicted in 2008–2009, 2016–2017 and 2019–2020, which might be due to global financial crisis 2007–2008 and Covid-19. Nevertheless, a long-term perspective seems to be upward sloping both for trade and RTAs negotiated in the region under the study.

Investment Trends in South, Southeast and East Asia

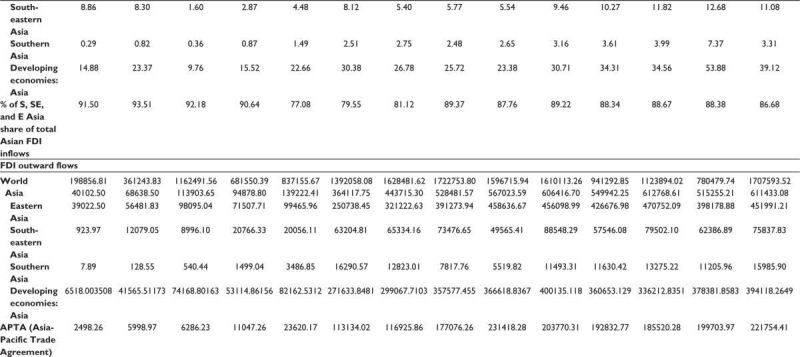

The study not only tabulates trade patterns for S, SE and E Asian economies but also captures the movements of investment in the region. ‘Asia continues to be the world’s top recipient region of foreign direct investment (FDI), accounting for nearly 30 per cent of global FDI inflows’, UNCTAD’s World Investment Report 2014. This indicates that Asia is emerging as one of the most prominent destinations for investment inflows. To study the direction, nature and pattern of investment flows in S, SE and E Asia, we have tabulated (see Table 8) FDI inward flows and FDI outward flows in the region.

Investment (FDI) refers to acquisition of business ventures by an entity in a foreign land. Asian economies such as China, Japan, Hong Kong, Korea, Singapore, India, Thailand and others are emerging as the most preferred destination for FDI inward flows. Table 8 depicts that in 2021, Asian economies were able to fetch 43.6% of world FDI inflows and S, SE and E Asian regions contributed 86.6% of total Asian FDI inflows (in 2021). Trends of the East Asian region depict that the region was able to fetch FDI inflows of 23.4% of world FDI inflows in 2021. A tremendous increase in FDI inflows for East Asia has been registered since 1991 (in 1991, East Asia received only 6.12% of world’s FDI inflows). Similarly, Southeast Asia accounted for growth in FDI inflows as 11.08% of world FDI inflows (in 2021) as compared to 8.86% inflows in 1991. FDI inflows for South Asia are depicting an upward trend but the growth is still slow and limited, South Asian economies received FDI inflows of 0.29% in 1991 and 3.3% of world FDI in 2021. South Asian region still needs to work towards inviting sizeable FDI flows in the region.

Talking about FDI outflows, prior to 1991 FDI outflows were prerogative of developed countries. As evident from Table 8, only 3.28% of FDI outflows went from developing Asian economies in 1991. However, the liberalisation wave promoted FDI outflows from developing economies too and, in 2021, developing Asian economies registered FDI outflows as 23.08% of world FDI outflows. Talking about the trends of East Asian economies, a significant rise from 19.62% (in 1991) to 26.47% of world FDI outflows (in 2021) is seen. However, the FDI outflows for Southeast and South Asia are still limited, which might be because the regions largely constitute of emerging economies where the liberalisation measures are limited and/or the industrial development in the region is not equipped enough to venture into a foreign land. For South Asian economies, FDI flows are even less than 1% of the world FDI outflows in 2021.

Table 8. FDI Inward and Outward Trends of South, Southeast and East Asian Regions (1991–2021).

Source: Based on the data collected from the FDI UNCTAD database.

To summarise, we can say that like trade flows, investment flows in an economy are indicators of liberalisation and the willingness of economies to expand (and diversify). The reasons for growth of FDI inflows and outflows in S, SE and E Asia can be stated as follows:

However, to boost FDI inflows and outflows Asian (especially Southeast and South Asian) economies still need to revisit and revamp FDI policies and strategies. FDI policies should be more towards fit-to-purpose and green technology in order to witness a sustainable flow of FDI in years to come (ESCAP-75, 2020).

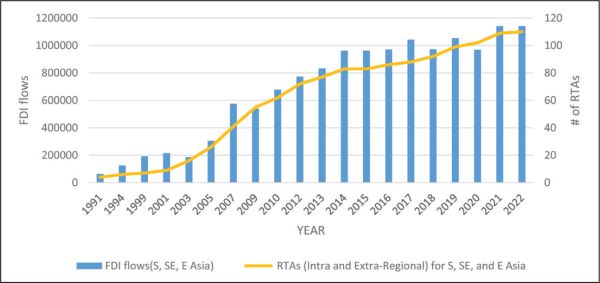

The study also tries to present (see Figure 3) the trends of RTAs and FDI flows (inward and outward) in Figure 3. Like trade trends, FDI trends were also upward moving since 1991. However, a reduction is registered during 2019–2020, which might be due to the Covid-19 pandemic.

Figure 3. Trends of RTAs and FDI Flows in S, SE and E Asian Economies.

Source: Based on the data collected from the WTO database and the FDI UNCTAD database.

The trends for RTAs, trade and investment depict that Asian economies are sincerely working towards liberalisation measures and are taking steps towards making the Asian subcontinent a major hub of global trade and investment. Also, countries in Asia are working towards promoting strong global value chains and global production networks by promoting trade and investment-associated norms and policies.

Conclusion

The regional trends of S, SE and E Asian RTAs depicted an upsurge in the number and intricacy. The present study was an attempt to examine the changing dynamics of regional integrations by examining the trends of three major RTAs of the said region, namely, ASEAN; APTA; and SAARC/SAFTA. The salient features of the trends can be stated as follows:

While summarising the trends of trade and investment in the S, SE and E Asian region, we were able to see an upsurge in the regional flows both for trade and investment and depicting compatibility with a significant rise in RTAs in the region:

Since 1991, not only an upsurge in the number (and depth) of regional economic integration can be seen but also a consistent rise in the investment flows, trade flows and production avenues can be registered. Emerging economies in the said region such as China, India, Korea, Singapore, Thailand and others seem to be major contributors. Though the trends for Southeast and East Asia for RTAs, trade and investments are found to be encouraging, trends for South Asia suggest that except India all other South Asian economies need to have better liberalisation policies and strong economic reforms in order to attract more quality and quantity of trade and investment flow. Further, the trends in the region indicate that economies in the said region are consistently working towards supporting global and regional supply chains, global production (and distribution) networks, strengthening digital trade, better investment ventures and adapting to changing dynamics of trade and investment on the global platform. However, as per the Asian economic integration report 2023 (ARIC, 2023), ‘Asian economies are able to register strong growth but headwinds are increasing’. To curtail inflation, Asian economies are tightening monetary policies but such measures are exerting pressure on external demand and, hence, exports. Further, almost all Asian economies are coming up with trade policies that are compatible with intra-regional and extra-regional production cycles. Hence, the trade structures for Asia are largely associated with exports and imports of intermediate goods but less with consumer goods.

Conclusion

Using the trends, we can state that S, SE and E Asian economies are significantly contributing to the world trade and investment market. However, the economies in the said region should work on a few aspects to further strengthen the trade and investment flows (both intra-regional as well as extra-regional). The regional integration negotiated in the region should be deepened to further support regional value chains and global value chains. Further, the upcoming RTAs should cater to the needs of digital trade flows and should be drafted towards making trade (and investment) flows resilient towards global shocks. Talking about the trade flows, trade policies should not only be compatible with the production cycle (catering to intermediate goods) but should also synchronise with the consumer needs and demands to further boost trade flows in the said region. In order to boost FDI flows, a number of Asian economies are providing corporate income tax incentives in terms of tax holidays, tax credits, investment allowances, etc. However, global (or regional) tax rules (and norms) would further strengthen cross-border investment. Further, economies in the region should focus on both aggregate and key sector-oriented trade and investment especially to boost eco-friendly products, green technology, energy-efficient flows and sustainable production (and distribution) networks.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Rinku Manocha https://orcid.org/0000-0001-7125-4858

Notes

1. www.wto.org

2. https://www.imf.org/external/pubs/ft/fandd/2006/06/picture.htm

3. https://www.wto.org/english/tratop_e/region_e/region_e.htm

4. https://www.worldbank.org/en/topic/regional-integration/brief/regional-trade-agreements

5. https://aseanplusthree.asean.org/

6. ‘India stays away from RCEP talks in Bali’. Nikkei Asian Review. Jakarta. February 4, 2020.

Adebayo, E. O. (2019). Trade trend and sustainable development in Nigeria. Izvestiya, Journal of Varna University of Economics, 63(4), 294–308.

Ahmed, A. (2021, December 17). Southeast Asia Ecommerce: What is trending now (Q1, 2022). Ced Commerce. https://cedcommerce.com/blog/what-are-high-demand-products-2022/

ARIC. (2023). Asian economic integration report 2023. https://aric.adb.org/aeir2023

Asian Development Bank. (2008). Foreign direct investment in South Asia. https://www.adb.org/publications/foreign-direct-investment-south-asia

Baldwin, R. E. (2006). Multilateralising regionalism: Spaghetti bowls as building blocs on the path to global free trade. The World Economy, 29(11), 1451–1518.

Banik, A., & Bhaumik, P. K. (Eds.). (2006). FDI: Global trends and assessments. In Foreign capital inflows to China, India and the Caribbean (pp. 7–22). Palgrave Macmillan.

Bhasin, N., & Manocha, R. (2016). Do bilateral investment treaties promote FDI inflows? Evidence from India. Vikalpa, 41(4), 275–287. https://doi.org/10.1177/0256090916666681

Bista, R. (2017). Economic liberalization in Nepal: Determinants, structure and trends of FDI (MPRA Paper 100070). University Library of Munich, Germany.

Borin, A., & Nino, V., Mancini, M., & Sbracia, M. (2018). Trade weakness: Cycle or trend? Financial and monetary policy studies. In L. Ferrara, I. Hernando, & D. Marconi (Eds.), International macroeconomics in the wake of the global financial crisis (pp. 99–114). Springer.

Bose, S., & Kohli, B. (2018). Study of FDI trends and patterns in BRICS economies during the period 1990-2015. Emerging Economy Studies, 4(1), 78–101.

Chattopadhyay, A. K., Rakshit, D., Chatterjee, P., & Paul, A. (2022). Trends and determinants of FDI with implications of COVID-19 in BRICS. Global Journal of Emerging Market Economies, 14(1), 43–59.

Chaudhury, D. R. (2022, July 29). Maritime outreach: Shipping route inaugurated between India & Central Vietnam. The Economic Times. https://economictimes.indiatimes.com/news/india/maritime-outreach-shipping-route-inaugurated-between-india-central-vietnam/articleshow/93216630.cms

Chowdhury, M. B. (2005). Trade reforms and economic integration in South Asia: SAARC to SAPTA. Applied Econometrics and International Development, 5(4). https://ssrn.com/abstract=1238219

Cihelkova, E., & Frolova, Y. D. (2014). The impact of regionalism on regional development under the conditions of a globalized economy. Экономика региона, CyberLeninka; Федеральное государственное бюджетное учреждение науки «Институт экономики Уральского отделения Российской академии наук». 4, 45–57. https://cyberleninka.ru/article/n/the-impact-of-regionalism-on-regional-development-under-the-conditions-of-a-globalized-economy/viewer

Cihelková, E., & Hnát, P. (2008). Budoucnost Evropské unie v kontextu nového regionalismu [Future of the European Union within the new regionalism context]. Politická ekonomie, Prague University of Economics and Business, 2008(1), 67–79.

Crawford, J. A., & Florentino, R. V. (2005). The changing landscape of regional trade agreements (WTO Discussion Paper No 8). https://www.wto.org/english/res_e/booksp_e/discussion_papers8_e.pdf

Daisuke, H. (2006). Outward FDI from and intraregional FDI in ASEAN: Trends and drivers (IDE Discussion Papers 77). Institute of Developing Economies, Japan External Trade Organization (JETRO). https://ideas.repec.org/p/jet/dpaper/dpaper77.html

de Melo, J., Solleder, J.-M., & Sorgho, Z. (2020). A primer on African market integration with a hard look at progress and challenges ahead (FERDI Working Paper No. P268). http://hdl.handle.net/10419/269548

Dimitris, K., & Pinna, A. M. (2013). Trade activity between the EU and its neighboring countries: Trends and potential (Working Paper CRENoS 201320). Centre for North South Economic Research, University of Cagliari and Sassari, Sardinia. https://ideas.repec.org/p/cns/cnscwp/201320.html

Dorosh, P. (2002, July 11–12). Trade and related economic reforms in Asian countries: What were the impacts of actual policy changes on agricultural development, trade and food security? [Paper presented]. FAO Expert Consultation on Trade and Food Security: Conceptualizing the Linkages, Rome.

Ergano, D., & Rambabu, K. (2020). Ethiopia’s FDI inflow from India and China: Analysis of trends and determinants. Journal of Economic Structures, 9(1), 1–20.

ESCAP. (2021). Foreign direct investment: Trends and outlook in Asia and Pacific 2020/2021.?https://unescap.org/kp/2021/foreign-direct-investment-trends-and-outlook-asia-and-pacific-20212022

ESCAP-75. (2019). Foreign direct investment: Trends and outlook in Asia and Pacific 2020/2021. https://artnet.unescap.org/fdi/resources/publications/foreign-direct-investment-trends-and-outlook-asia-and-pacific-20202021

ESCAP-75. (2020). Foreign direct investment: Trends and outlook in Asia and Pacific 2020/2021. https://www.unescap.org/resources/foreign-direct-investment-trends-and-outlook-asia-and-pacific-20202021#

Fischer, P. (2000). Global FDI trends. In Foreign direct investment in Russia (pp. 79–115). Palgrave Macmillan.

Gauchan, B., & Sarin, V. (2018). Is South Asia an optimum currency area? Journal of Economic Integration, 33(3), 572–603. https://doi.org/10.11130/jei.2018.33.3.572

Haokip, T. (2012). Recent trends in regional integration and the Indian experience. International Area Studies Review, 15(4), 377–392.

Hattari, R., & Rajan, R. S. (2008). Trends and drivers of bilateral FDI flows in developing Asia (Working Papers 112008). Hong Kong Institute for Monetary Research. https://ideas.repec.org/p/hkm/wpaper/112008.html

Hill, H., & Menon, J. (2010). ASEAN economic integration: Features, fulfillments, failures and the future. ADE.

Idris, H., & Ramli, M. (2018). Southeast Asian region maritime connectivity and the potential development of the Northern Sea route for commercial shipping. Journal of Southeast Asian Studies, 23(2), 25–46.

Islam, A. M. (2019). Bangladesh trade with India: Trends and patterns. Athens Journal of Business & Economics, 5(2), 123–140.

Jain, R. (2005). India and SAARC: An analysis. Indian Journal of Asian Affairs, 18(2), 55–74. http://www.jstor.org/stable/41950459

Kapadia, J., & Agrawal, H. (2011). Role of FDI in infrastructure development in India. 1, 61–68.

Karymshakov, K., & Sulaimanova, B. (2021). The impact of infrastructure on trade in Central Asia. Asia European Journal, 19(Suppl. 1), 5–20. https://doi.org/10.1007/s10308-021-00613-7

Kawai, M., & Wignaraja, G. (2010). Asian FTAs: Trends, prospects, and challenges (Asian Development Bank Economics Working Paper Series No. 226). https://ssrn.com/abstract=1721911 or http://doi.org/10.2139/ssrn.1721911

Kirillov, Y., & Paweta, E. (2014). Modern trends in international economic integration development. Ekonomia Mi?dzynarodowa, (8), 199–208. https://www.ceeol.com/search/article-detail?id=154896

Kunze, B. (1972). Trends in Britain’s eastern trade. Intereconomics, 7(10), 317–320. https://doi.org/10.1007/BF02929651

Mahnaz, M., Ali, M., Ahmad, I., & Khalil, K. (2022). Role of foreign direct investment in employment generation: Evidence from FDI recipient economies. Pakistan Languages and Humanities Review, 6(3), 94–107.

Manocha, R. (2018). Impact of regional trade agreements on India’s trade potential: the case of SAARC and APTA. FOCUS: Journal of International Business, 5(1), 14–36.

Manocha, R., & Bhasin, N. (2022). Proposed India-UK free trade agreement: Estimating potential export gains for India. Productivity, 63(2), 156–168.

Molla, M. E. (2018). Trend of FDI and economic growth: A study on Bangladesh. International Journal of Science and Business, 2(4), 588–597.

Mukherjee, A., Paul, A., Sarma, A. P., & Sinha, S. (2019). Trade, trade agreements and subsidies: The case of the Indian apparel industry (Working Papers id:13002). eSocialSciences. https://ideas.repec.org/p/ess/wpaper/id13002.html

Nikoloski, K., & Paceskoski, V. (2015). Contemporary trends in the world trade. Annals: Economy Series, 6, 21–26. https://ideas.repec.org/a/cbu/jrnlec/y2015v6p21-26.html

Oehler-Sincai, I. M. (2009). Recent trends in the EU trade in goods. The Journal of Global Economics, 1(2). https://ideas.repec.org/a/iem/journl/v1y2009i2id2822000008753047.html

Pant, M., & Mondal, S. (2010). FDI, technology transfer and spill over: A case study of India (Discussion Paper 10-04). Centre for International Trade and Development,JNU. https://www.jnu.ac.in/sites/default/files/citd/DP04_2010.pdf

Park, S. C., Kim, C. J., Taghizadeh-Hesary, F., & Sirivunnabood, P. (Eds.). (2021). Economic integration in Asia and Europe: Lessons and policies. ADBI Books.

Park, I. and Park, S. (2008). Reform creating regional trade agreements and Foreign Direct Investment. Pacific Economic Review, 13(5), 550–566.

Rafiq, S., Yun, L. H., & Ali, G. (2016). Forecasting the trend analysis of trade balance of Pakistan: A theoretical and empirical investigation. International Journal of Academic Research in Business and Social Sciences, 6(7), 188–214.

Raghurampatruni, R., Senthil, M., & Gayathri, N. (2021). The future potential and prospects of SAARC regional grouping: A study. India Quarterly, 77(4), 579–604. https://doi.org/10.1177/09749284211047722

Rao, K. S. C., & Dhar, B. (2011). India’s FDI inflows: Trends and concepts (MPRA Paper 29153). University Library of Munich, Germany. https://mpra.ub.uni-muenchen.de/29153/1/MPRA_paper_29153.pdf

Sahiti, A., Ahmeti, A., & Sahiti, A. (2020). FDI trends and characteristics in Kosovo. Baltic Journal of Real Estate Economics and Construction Management, 8(1), 12–21.

Sakakibara, E., & Yamakawa, S. (2003). Regional integration in East Asia: Challenges and opportunities, Part 1. History and institutions (Policy Research Working Paper No. 3078). © World Bank, Washington, DC. https://openknowledge.worldbank.org/entities/publication/0f8ccf2a-8b68-5c39-baa6-00eaf4149b7c

Sapkota, J. B., Acharya, C. P., Minowa, M., & Neupane, P. (2018). Trade integration in Asia: Trends and determinants (MPRA Paper 106063). University Library of Munich, Germany. https://mpra.ub.uni-muenchen.de/106063/1/MPRA_paper_106063.pdf

Shimada, R. (2019). Southeast Asia and international trade: Continuity and change in historical perspective. In K. Otsuk & K. Sugihara (Eds.), Paths to the emerging state in Asia and Africa. Emerging-economy state and international policy studies (pp. 55–71). Springer. https://doi.org/10.1007/978-981-13-3131-2_3

Shree, S., & Sridhar, S. (2016). Changing growth trend and competitiveness in the trade of livestock products in India. Journal of Global Economy, 12(4), 259–268.

Shu, M. (2018). Trade, competitiveness, and the China factor. In S. Khorana & M. García (Eds.), Handbook on the EU and international trade (pp. 315–332). Edward Elgar Publishing.

Straubhaar, T. (1986). South-South trade: Some recent trends. Intereconomics, 21(5), 239–245, https://doi.org/10.1007/BF02926978

Taneja, N., Bimal, S., & Sivaram, V. (2019). Emerging trends in India-Pakistan trade (Working Papers No. 13004). eSocialSciences. https://ideas.repec.org/p/ess/wpaper/id13004.html

Thirlwall, A. P., & Gibson, H. D. G. (1992). Import functions. In Balance-of-payments theory and the United Kingdom experience (pp 272–290). Palgrave Macmillan.

Thomas, Z. (2014). Not all free trade agreements have the same advantages (School of Economics Working Paper Series 2014-9). LeBow College of Business, Drexel University. https://ideas.repec.org/p/ris/drxlwp/2014_009.html

Workman, D. (2022). Top Asian export countries. World’s top exports. https://www.worldstopexports.com/top-asian-export-countries/#:~:text=International%20sales%20of%20products%20originating%20from%20Asia%20represent,

2017%20but%20below%20the%2042.3%25%20portion%20for%202020

World Bank. (2005). Global economic prospects 2005: Trade, regionalism and development. World Bank.

Wu, P. J., Qari, S., Banach, C., & Azarhoushang, B. (2017). A database for investigating foreign direct investment and regional trade (IPE Working Papers 94/2017). Berlin School of Economics and Law, Institute for International Political Economy (IPE). http://hdl.handle.net/10419/172762

Yang, C. (2016). Relocating labour-intensive manufacturing firms from China to Southeast Asia: A preliminary investigation. Bandung Journal of Global South, 3(1), 1–13. https://doi.org/10.1186/s40728-016-0031-4