Review of Professional Management

Search

Search

Rachna Mahalwala1  and Girish Ahuja2

and Girish Ahuja2

1 Bhagini Nivedita College, University of Delhi, New Delhi, Delhi, India

2 GD Goenka University, Sohna Rural, Haryana, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

The smooth running of business operations demands an efficient management of working capital by properly managing the inventory, accounts receivables and accounts payables of the business. This helps companies not only fulfil their short-term financial commitments but also boost their earnings. Therefore, the present study aims at verifying the impact of working capital management on the profitability of the companies under pharmaceutical industry in India. For empirical analysis, the data of 618 pharmaceutical companies is taken over a period of seven years from 2014–2015 to 2020–2021 and multivariate panel data regression technique is applied on data for estimating the results. The findings of the study validate that the profitability of companies is significantly influenced by working capital management. These findings will provide an insight to corporate managers and owners of pharmaceutical companies in deciding appropriate working capital strategy.

Working capital, return on assets, fixed effects, random effects

Submitted 20 September 2022; accepted 22 May 2023

Introduction

The management of working capital (WC) involves the administration of all short-term assets, that is, current assets and all short-term liabilities, that is, current liabilities of the business. Though a vast literature in corporate finance has paid attention to the impact of long-term financial decisions, namely, capital budgeting decisions, financing decisions and dividend decisions, on the financial success of firms, the impact of management of short-term financial decisions involving working capital management (WCM) on firm’s financial performance largely remains neglected. Since WCM is crucial to a company’s profitability, risk and value, the management of short-term assets and liabilities requires a thorough investigation (Smith, 1980). Wrong estimation of WC requirement may lead the creditors and investors of firms to an unexpected risk of default (Richards & Laughlin, 1980). Thus, WCM is a critical decision-making area for finance managers as shortage of funds for WC may affect profitability and commercial solvency position of a firm. Besides efficient management of WC will help in maintaining an adequate liquidity level while increasing the profitability and market value of the firm. Effective WCM provide an aid to finance managers to enhance the value of the firm and to circumvent probable financial difficulties (De Almeida & Eid Jr, 2014).

The present study aims at finding out the impact of WCM on the profitability of pharmaceutical companies. The core stimulus to select the pharmaceutical industry of the economy is due to the following reasons: (a) India is a rising player in the global pharmaceuticals sector. According to the Indian Economic Survey 2021, India’s domestic pharmaceutical market is estimated at US$42 billion in 2021 and likely to reach US$65 billion by 2024 and further expected to expand to reach approximately US$120–130 billion by 2030. Thus, the domestic market is expected to grow thirty times in the next decade. (b) The Indian pharmaceutical industry, which includes 3,000 pharmaceutical companies and 10,500 production units, supplies more than half of the global demand for vaccines, 40% of generic drug demand in the United States, and one-fourth of the medicine demand in the United Kingdom (Groww, 2021). In terms of volume, India is the world’s third-largest producer of pharmaceuticals and in terms of value, India ranks 14th (IBEF, 2021). (c) The Indian pharmaceutical industry contributes around 2% to India’s GDP and approximately 8% to the country’s total merchandise exports (RBI, 2021). (d) Being part of a manufacturing industry, the pharmaceutical companies rely heavily on WC for its successful operation and raw material happens to be the major component of cost. Therefore, the length of time in converting raw material in finished goods, finished goods to sales and sales into cash become crucial for the success and profitability of companies.

In the light of this backdrop, it becomes important to explore the impact WCM decisions on the profitability of the companies under pharmaceutical industry of the Indian economy. The rest of the study is structured as follows: The ‘Literature Review’ section discusses the existing literature relating to conceptualisation of WCM and its effect on the profitability. It also describes the objective and the expected contribution of the study. The ‘Research Methodology’ section elaborates the research methodology. The ‘Empirical Results’ section presents empirical results. The ‘Discussion and Conclusion’ section deliberates the results and concludes the study.

Literature Review

In finance, though the management of WC has received adequate attention in empirical literature to examine the relationship/trade-off between liquidity and profitability, there is dearth of the extant theoretical research and perspective concerning with WCM to guide the financial managers regarding how to optimise the use of short-term assets to improve the long-term financial performance of the business. Gitman (1974) in his seminal research established the concept of cash cycle (CC) for WC optimisation in terms of liquidity. However, Richards and Laughlin (1980) invoked the concept of CC into the cash conversion cycle (CCC) to assess the efficiency of a company’s WCM. The cash conversion cycle, often known as the WC cycle, is a crucial instrument for evaluating the effectiveness of WCM (Richard & Laughlin, 1980). To improve the financial performance of firms, the CCC needs to be shortened to the period where the operations of the business do not get compromised (Cheatham et al., 1989; Moss & Stine, 1993). It is emphasised that with the shorter the CCC, the internal processes of the business become more efficient (Gentry et al., 1990). However, the lengthier the CCC is, the higher will be the dependence of the business on external funds (Maness, 1994). This external funding can be in the form of short-term debts, long-term debts or equity (Gallinger, 1997).

Deloof (2003) asserted that receivable accounts, payable accounts and inventory are three aspects of the WC cycle that must be managed in effective ways to maximise profit or raise the company’s worth. WCM tries to maximise profitability while avoiding the danger of incapability to redeem short-term debts as they mature. WCM efficacy is determined by a company’s capacity to strike a balance between profitability and liquidity (Filbeck et al., 2007). The true association between WCM and profitability is dependent upon the choice of a company’s WCM strategy (Tauringana & Afrifa, 2013). A company has an option to choose between two WCM strategies: conservative and aggressive (Nazir & Afza, 2009). Both strategies are diametrically opposed. According to the conservative approach, more investment in WC may boost profitability of business. On the other side, an aggressive approach recommends less investment in WC may increase profitability.

The existing theoretical and empirical literature about true linkage between the variables, WC and profitability, is not translated into a coherent theory (Falope & Ajilore, 2009). Canina and Carvell (2008) asserted that a high current ratio may not always indicate a company’s good financial performance in the short run as a high current ratio could result from improved collection of receivables rather than greater sales.

To study the relationship between WCM and profitability, several empirical research are conducted in different countries for different industries. This section will briefly shed light on select studies which examined the impact of short-term financing decisions relating to WC policy on the profitability and value of the firm.

Mandal and Goswami (2010) assessed the effect of WCM on cash flows, profits and non-insurable risk of ONGC during 1998–1999 to 2006–2007 with the help of various statistical tests like t-test, F-test and Durbin–Watson test. The results showed a significant relationship between profitability and liquidity of the firm. This implied that the performance of the company should not be judged only on the basis of surplus generating capability/profitability measured in terms of return on sales and investment, the company should always try to attain a thoughtful level of WC within its risk-bearing capacity for enhancing profitability.

Nazir and Afza (2009) explored the association and influence of the type of WCM policy (aggressive/conservative) on the financial success of non-financial firms listed on Karachi stock exchange that belonged to varied industrial sectors. The study adopted Tobin’s Q and panel data regression technique to empirically validate the results and reported a negative association between the profitability and aggressive WC policy. This indicated that the firms adopting the aggressive WC policy will fail to generate good returns.

Mohamad and Saad (2010) conducted an empirical study to provide evidence of effect of WCM on firm performance by taking 172 Malaysian companies’ data for the period 2003–2007 and used regression analysis. The results concluded a significant negative linkage amid WCM and firm’s value and profitability and stressed that proper management of WC is critical for improving firm’s financial performance.

Ogundipe et al. (2012) researched how the management of WC affects the financial performance and the market value of the firm by taking a sample of 192 listed companies on Nigerian Stock Exchange and collecting the data for the period 1995–2009. The study employed correlation analysis and regression analysis to get empirical evidence. The results reported a significant negative relation between WCM and the market value and the financial performance of the companies. The results inferred that by shortening the length of CCC, the goal of maximising the profits and consequently, increasing the market value of firm may be achieved.

Sharma and Kumar (2011) explored the connection between WCM and profitability of 263 companies forming part of BSE 500 index from 15 different industries by taking data for the period 2000–2008. By running ordinary least squares multiple regression model, the findings of the study indicated a positive association between WCM and profitability leading to the conclusion that the longer the CCC, the better it is from the point of view of profitability. The findings of the study were in vast contrast to the results of many previous studies.

Bagchi and Khamrui (2012) investigated the relation between WCM and profitability by studying some select FMCG companies in India. The study concluded that there is a robust negative connection between components of the WC decisions and profitability of the firm. With an increase in the CCC, the decline in the profitability of the firm is evident. There is also a weak negative connection between debt employed by the firm and its profitability.

Arunkumar and Ramanan (2013) in their paper inspected the effect of WC on the profitability of Indian manufacturing companies and the results validated a significant positive linkage between return on assets and debtors’ holding period and inventory holding period. Creditors’ conversion period, however, was found to have negative connection with return on assets. Sensitivity analysis was also conducted to with respect to return on assets and explanatory variables.

Singhania et al. (2014) carried out a study to find out how the WCM exerts an influence on the profitability of 82 firms over the period 2005–2012 along with analysing the impact of worldwide recessionary conditions on the said relationship. Using correlation analysis and regression equation, the results evidenced that curtailing the CCC positively influences the profitability of firms. The results further supported that expanding the number of days receivables has an adverse impact on the profitability, while increasing the number of days payables results to enhancing the financial performance.

Ismail and Bandara (2015) checked the influence of WCM on profits of 183 companies from four different industries of Expolanka subsidiaries for the period 2009–2014 and the results confirmed a strong positive linkage between receivables conversion period and net profit and the gross profit, a strong positive association between days payable outstanding and gross profit, and a strong positive relationship amid inventory days outstanding and gross profit. The results further showed an inverse connection between CCC and gross profit and net profit making it apparent the shorter the CCC, the more will be the profits of firms.

Samiloglu and Akgün (2016) aimed at highlighting the influence of WCM on the operating performance of manufacturing companies listed on Istanbul Stock Exchange by employing multiple linear regression models on panel data for the period 2003–2012. The results of the study indicated a significant inverse linkage between accounts receivable period and various profitability indicators, namely, return on assets, return on equity, operating profit margin and net profit margin. This suggests that corporate managers may enhance value of the firm by dipping the accounts receivable period and the CCC.

Hingurala Arachchi et al. (2017) studied the effect of efficient of WCM on market value of companies listed on Colombo Stock Exchange with panel data regression techniques. The findings of the study revealed the negative effect of the CCC on Tobin’s Q, signifying that an efficient WCM has potential to augment the current value of the firms. The results infer that lowering the accounts receivable conversion cycle and inventories conversion cycle helps in maximising the shareholders’ wealth.

Paul and Mitra (2018) in their research paper examined the influence of WC policy on the profitability of the firms taking evidence from Indian Steel Industry and the results corroborated that profitability of companies is influenced by WC decisions. The results showed a noteworthy positive impact of quick ratio and debtors’ turnover ratio on return on assets and no notable impact of finished goods turnover ratio and current ratio on return on assets.

Boisjoly et al. (2019) explored the effect of aggressive WC policy relating to metrics like receivables turnover, inventory turnover, days payables outstanding and CCC on firm valuation and profitability by applying ordinary least squares regressions on panel data of firms belonging to varied industries for the period 1990–2017. The results suggested that CCC exerts more prominent influence on firm valuation and profitability in comparison to individual metrics of WCM.

Khan et al. (2020) evaluated the effect of WCM on the profitability of the companies in the telecom sector in Pakistan. It examined the influence of the average receivable collection period, inventory conversion period, average payment period and CCC on the profitability of the companies with five years data (2013–2017). The result of this study supported that there is a negative and significant effect of WCM on the profitability of companies.

Anton and Afloarei Nucu (2021) considered the connection between WC and profitability of firms for an emerging economy, Poland, by taking a sample of 719 Polish companies for the 10-year period (2007–2016). The results reveal an inverted U-shape relationship between WC level and profitability of firms which implies that there exists an ideal level of WC that maximises Polish firm performance and if WC is increased above its optimum level, it will establish a negative relationship with profitability. Thus, finance managers should aim at achieving the finest level of WC through its major components, namely, receivables, payables and inventory, to maximise the influence of efficient WC on firm financial success in the best interest of the shareholders.

Jaworski and Czerwonka (2022) investigated the connection between WCM using measures such as CCC and WC value and the performance of Polish companies using measures such as liquidity and profitability. They considered data of 326 companies during the period 1998–2016. The empirical findings established a significant non-linear relationship between WC and performance of companies. The results showed that as WC and liquidity measured with current ratio increases, profitability too increases, but at a lower rate. The association amid the CCC and profitability turned out to be linear and negative. The results validate that to increase the profitability, the businesses try to defer payments to trade creditors and tend to settle the bank loans from the cash payments thus deferred. The study, thus, vouches the theories on linkage between the profitability and the WCM. The results imply that companies looking for growth in profitability should try to shorten CCC. For some industries, where the profitability found to have decreased as liquidity increases, it may indicate that current assets are not efficiently used.

Aldubhani et al. (2022) researched as to how WC policies affected the profitability of companies from different industries listed on the Qatar Stock Exchange. To find out this relationship, they adopted the technique of multiple regression analysis taking data of 10 manufacturing companies for the period 2015–2019. The WCM is proxied with average collection period, average payment period, inventory turnover and CCC and profitability of companies is quantified with operating profit margin, return on assets, return on capital employed and return on equity. The results inferred that shorter receivables collection periods and shorter CCC lead to high profitability and lengthier accounts payable payment periods and inventory turnover periods tend to increase the profitability of the companies.

Mandipa and Sibindi (2022) considered the data of 16 retail companies listed on the Johannesburg Stock Exchange over 10 years from 2010 to 2019 and studied the plausible linkage among WCM practices and the financial success. They employed a fixed-effects estimator for empirical analysis. The findings of the study established that WCM policies of South African retail companies affected their financial performance. Thus, optimising the WCM proxies ‘average age of inventory, average collection period, average payment period and CCC’ used in study have potential to improve the financial performance of companies ‘net operating profit margin, return on assets, and return on equity’ without jeopardising the loss of customers.

Extant research which is conducted in various countries of the world using different exogenous variables and different methodology, in different time-frame and for different sectors and industries of the economy have reported mixed results relating to impact of WCM on profitability of companies. As the literature review of empirical studies concludes inconsistencies and vagueness in findings and one of the major factor responsible for such results is the heterogenous nature of companies belonging to different sectors/industries as most of the empirical studies used a general mix of companies of varied industries, instead of industry-specific companies; therefore, the present study aims to focus a particular industry, namely, pharmaceutical industry, having good future growth prospects. This approach is expected to help in consensus-building and reaching unambiguous conclusions regarding the impact of WCM on profitability of companies.

Therefore, the objective of the present study is to investigate the impact of WCM decisions on the profitability of companies belonging to Indian pharmaceutical industry taking a sample of 618 companies over a sample period of seven years from 2014–2015 to 2020–2021.

The contribution of the present study to the extant literature on the linkage between the WCM and the profitability of firms is twofold, that is, first, it specifically focuses on Indian pharmaceutical companies where limited research is done in the area of WCM vis-à-vis financial performance and, second, this study enriches the existing literature on issue under consideration with respect to manufacturing companies, in general, for their real dependence on WC cycle for managing routine operations of business while aiming to ultimately earn good profits.

The findings are expected to provide help to corporate managers and owners in devising appropriate WCM strategy that help in enhancing the profitability of companies.

Research Methodology

With the objective of finding out the repercussion of WCM decisions on the profitability of the firm in case of companies belonging to pharmaceutical industry in India, the researchers downloaded the data of 911 companies belonging to drugs and pharmaceutical industry in India from the ‘Centre for Monitoring Indian Economy’ (CMIE)—Prowess financial database over a span of seven years, from 2014–2015 to 2020–2021. However, due to missing data during the sample period in case of many companies, a final selection of 618 companies is made for empirically examining the results.

Methodology

Description of Variables

To explore the weight of WC decisions on profitability of companies under the Indian pharmaceutical industry, the current study takes returns on assets (ROA) as a dependent variable and working capital cycle (WCC), inventory conversion period (ICP), receivables conversion period (RCP), creditors deferral period (CDP) and quick ratio as independent variables along with sales, size of firm and debt-equity ratio (D-E Ratio) as control variables.

Dependent Variables

ROA: ROA is a financial ratio that measures how much profit a company is generating by investing its total assets. A rising ROA tells improving profitability of the company in relation to its total assets.

Independent Variables

WCC: WCC, also known as cash conversion cycle (CCC) is the length of time between making payment to suppliers and receiving cash from sales. It is calculated with the following formula: WC cycle = Inventory conversion period + receivables conversion period  creditors deferral period.

creditors deferral period.

Inventory Conversion Period: ICP refers to the length of time taken to convert inventory into sales. It is calculated with the following formula: inventory conversion period = (inventory ÷ cost of sales) × 365.

Receivables Conversion Period (RCP): RCP indicates the length of time it takes for the company to collect cash from its credit sales. It is calculated with the following formula: receivables conversion period = (receivables ÷ sales) × 365.

Creditors Deferral Period (CDP): CDP indicates the length of time taken by the company to delay payment of its suppliers and creditors. It is calculated with the following formula: creditors deferral period = (trade payables ÷ purchases) × 365.

Quick Ratio (QR): QR is a metric of liquidity which indicates the ability of acompany to use its near cash assets to meet its short-term liabilities immediately. It is computed with the following formula: quick ratio = (current assets inventory prepaid expenses)/current liabilities.

Control Variables

Sales: Sales in accounting terms refers to the revenue earned by the company from the sales of products or services. It is calculated with the following formula: Sales = Units Sold × Sales Price. As high sales volume means high profits, it is taken as a control variable.

Size of Firm: There are various variables that can be used to measure the size of the firm, namely, total assets, total sales, total employees, and market value of equity. In this study, natural logarithm of total assets is taken as a measure of firm size.

Debt-equity ratio (D-E ratio): The D-E ratio is a leverage ratio that quantifies the relative amount of debt as against shareholders’ equity to finance a company’s assets. It is calculated as debt equity ratio = Total liabilities/total shareholders’ equity.

Figure 1. Conceptual Framework of the Study.

Empirical Model

As a preliminary exercise before applying empirical model, the descriptive statistics of data are studied and correlation analysis is done to check for existence of multicollinearity among independent variables. Also, before running regression on the panel data, it is to be ensured that all the variables are stationary since if the variable(s) data has a unit root, it may establish false results. Therefore, all the variable series are subjected to the panel unit root test. The study adopts three-panel unit tests, namely, Levin et al. (2002) test, ADF-Fisher test and PP-Fisher test (Maddala & Wu, 1999).

To find out the impact of WCM on profitability of companies under Indian pharmaceutical industry, the present study adopts panel data analysis technique. Panel data technique is appropriate in present case as data for different financial variables is collected over time, that is, the study is using longitudinal data of all variables discussed above. The results are estimated with the three generally used panel data methods, namely, pooled ordinary least squares (POLS), fixed effects (FE) and random effects (RE). However, to begin with, POLS is first applied to the data ignoring any cross-sectional and time-varying heterogeneity of panel data. Then with the help of post-estimation test, Breusch–Pagan Lagrange multiplier (BP-LM) test (Breusch & Pagan, 1979); the results of POLS are checked for panel effects. When BP-LM test rejects the null hypothesis of ‘no random effects’, the FE and RE estimations are done. Further, to check which model, FE or RE, fits best for data, another post-estimation test, namely, the Hausman test developed by Hausman (1978) is employed to test the null hypothesis ‘RE is appropriate’. On the basis of Hausman test results, the study reaches to best-fit model. Taking the dependent variables, independent variables and control variables, the panel regression equation with intercept and error can be detailed as follows:

.jpg/10_1177_09728686231184951-eq1(1)__300x89.jpg) (1)

(1)

In the above equation, ‘i’ is denoting companies, ‘t’ is denoting year, ‘α’ is used for intercept, ‘βi’ are denoting coefficient of independent and control variables, ni is the unobservable time-invariant company effect and fit is the random error.

Testing of Hypotheses

To attain the objective of finding out the impact of WCM on profitability of companies, the following hypothesis is developed in its null form:

H0: There is no statistically significant impact of working capital management on the profitability of companies.

The above hypothesis can be studied with hypotheses of individual elements of WCM and profitability in the following forms:

H1: The impact of WCC on ROA is not statistically substantial.

H2: The impact of ICP on ROA is not statistically substantial.

H3: The impact of RCP on ROA is not statistically substantial.

H4: The impact of CDP on ROA is not statistically substantial.

H5: The impact of QR on ROA is not statistically substantial.

H6: The impact of sales on ROA is not statistically substantial.

H7: The impact of size on ROA is not statistically substantial.

H8: The impact of D/E ratio on ROA is not statistically substantial.

Empirical Results

The empirical results start with a brief description of the descriptive statistics of all the variables used in the study summarised in Table 1. The mean value of return on assets is 1.570118 with a standard deviation of 25.90403%. The average WC cycle of all the companies taken together is around () 53 days, the average receivables conversion period is around 217 days, the average creditors deferral period is around 659 days and the average inventory conversion period is around 108 days. The average quick ratio of all the companies taken together is 1.687185, the average sales revenue is `4,663.575 million and the average debt-equity ratio is around 1.6. The evidences of skewness and high kurtosis are evident for all the variables. The Jarque-Bera statistics is significant for all the variables at 1% level of significance, indicating that the data is not normal.

Table 1. Descriptive Statistics of All Variables.

.jpg/10_1177_09728686231184951-table1%20(1)__800x159.jpg)

Source: Author’s calculation using EViews.

Table 2 presents the correlation matrix of all the variables. ROA is found to have a negative correlation with WCC, RCP, CDP, ICP and sales and a positive correlation with QR, size and D/E ratio. If we look at bivariate correlations between the independent and/or control variables, WCC is having a positive correlation with RCP, QR, size and D/E ratio but a negative correlation with CDP, ICP and sales. RCP is seen to have a positive correlation with CDP, ICP, QR and sales and a negative correlation with size and D/E ratio. CDP has a constructive association with ICP and sales and adverse association with QR, size and D/E ratio. ICP is having a positive correlation with QR and sales and a negative correlation with size and D/E ratio. QR is showing a negative correlation with sales a positive correlation with size and D/E ratio. Since the results do not show high value of correlation coefficient (>0.08) amid any two independent variables used in the study, the problem of multicollinearity is not established. Gujarati (2004) suggested that if the value of correlation coefficients among independent variables does not outdo the threshold value of 0.80, the problem of multicollinearity becomes implausible.

Table 2. Correlation Matrix.

Source: Author’s calculation using EViews.

Source: Author’s calculation using EViews.

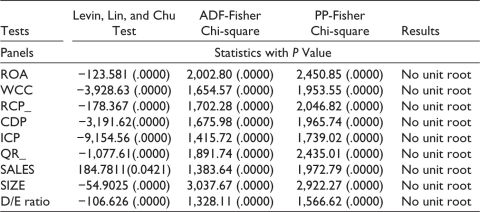

Before explaining the regression results, the results of the three-panel unit root tests, namely, Levin, Lin, and Chu test, ADF-Fisher test, and PP-Fisher test, are reported in Table 3 relating to inspecting the stationarity of all variable series. The results show all the variable series (ROA, WCC, RCP, CDP, ICP, QR, sales, size and D/E ratio) are stationary with p value < .00 or <.05.

Table 3. Results of Panel Unit Root Test.

Source: Author’s calculation using EViews.

Table 4 highlights the results of POLS. If we look at the impact of independent variables on dependent variable, the results reveal a negative significant impact of WCC, CDP and ICP on ROA and a positive significant impact of RCP and QR on ROA. In case of the control variables, there is a significant positive impact of sales on ROA and significant negative impact of size and D/E ratio on ROA. However, because of possible random effect in data, the results are tested for panel effect.

Table 4. Results of Pooled Ordinary Least Squares (POLS) Estimation.

Source: Author’s calculation using EViews.

Table 5 presents the results of Breusch–Pagan test. The results confirm the presence of random effects because the reported LM statistics (1,394.389) is significant at 1% level of significance. This indicates that POLS results are not efficient and FE or RE model can be applied.

Table 5. Breusch–Pagan Test Results.

Source: Author’s calculation using EViews.

Table 6 provides the results of fixed effects model. The results disclose a significant and negative impact of WCC, CDP, size and D/E ratio on ROA, while a significant and positive impact of RCP, QR and sales on ROA. No significant impact of ICP on ROA is reported.

Table 6. Fixed Effects Model Estimation Results.

Source: Author’s calculation using EViews.

Table 7 reports the results of random effects estimation. The results are alike the results of fixed effects model. The results show a significant negative impact of WCC, CDP, size and D/E ratio on ROA; however, a substantial positive impact of RCP, QR and sales on ROA is found. ICP is found to have no substantial relationship with ROA.

Table 7. Random Effects Model Estimation Results.

Source: Author’s calculation using EViews.

To check which model, FE or RE, is best fit in the present case, the results of RE model are subjected to post-estimation Hausman test. The results of Hausman test are shown in Table 8. The test outcomes rejected the null hypothesis of appropriateness of RE model as reported chi-square statistic (28.472727) is significant with a p value (.0004). This infers that fixed effect estimation is best fit for the panel data of 618 Indian pharmaceutical companies.

Table 8. Hausman Test Results.

Source: Author’s calculation using EViews.

Thus, the overall empirical exercise concludes that according to the best fit ‘fixed effects model’, WCM decisions proxied with WCC, RCP, CDP, QR, sales, size and D/E ratio puts a significant impact on profitability proxied with ROA. ICP does not exert any noteworthy impact on profitability. Therefore, the null hypotheses H1, H3, H4, H5, H6, H7 and H8 are rejected and the null hypothesis H2 does not get rejected. The null hypothesis (H0) for overall impact of WCM on profitability of companies is rejected.

Discussion and Conclusion

With the objective of finding out the impact of WCM on profitability in case of companies under the Indian pharmaceutical industry, the present study took a sample of 618 companies over a period of seven years and employed panel data methodology for empirical analysis. As fixed effects model found to be the most appropriate model, the discussion on results and concluding remarks are based on fixed effects model’s findings. The study depicts a negative influence of WC cycle and creditors deferral period on profitability, a positive impact of receivables conversion period and quick ratio on profitability, and no influence of inventory conversion period on profitability. The negative impact of WC cycle on profitability is in conformity with many previous studies including Deloof (2003), Nazir and Afza (2009), Mohamad and Saad (2010), Ogundipe et al. (2012), Bagchi and Khamrui (2012), Singhania et al. (2014), Hingurala Arachchi et al. (2017), Khan et al. (2020) and many others. The results convey that shortening of the WC cycle can positively affects the profitability of Indian pharmaceutical companies. The negative affiliation between the creditors’ deferral period and profitability indicates that decreasing the average payment period for suppliers can increase the profitability of companies while increasing the average payment period can lead to decline in profitability. Thus, the shortening of creditors deferral period can enhance the profitability of the companies. These findings are supported with the studies conducted by Raheman and Nasr (2007), Lazaridis and Tryfonidis (2006) and Sharma and Kumar (2011). A significant positive impact of receivables conversion period on profitability infers that increasing the collection days from debtors for credit sales can enhance the profitability of the companies. The same result is reported by Sharma and Kumar (2011) and Arunkumar and Ramanan (2013), however, is in contrast with many previous studies (Falope & Ajilore, 2009; Raheman & Nasr, 2007). This implies that a delay in collection of receivables, that is, extending the receivables conversion period has potential to increase the profitability of the companies. The significant positive impact quick ratio on return on assets suggests that a higher quick ratio, that is, higher liquidity can also positively impact profitability of pharmaceutical companies in contrast to the classical concept of trade-off between liquidity and profitability (Smith, 1980). However, this result is in conformity with the studies conducted by Shakoor et al. (2012), Pandey et al. (2016), Bala et al. (2016), Janjua et al. (2016). An insignificant positive relationship between inventory conversion period and return on assets indicates that there are inconsequential evidences that lengthening of inventory conversion period can cause increased profitability. This result contrasts with most of the earlier empirical research suggesting an inverse relationship between inventory conversion period and profitability of companies (Filippini & Forza, 2016; Nazir & Afza, 2009). Further, the results suggest that there is a significant positive impact of sales on profitability, that is, as sales increase, the profitability of pharmaceutical companies increases, a significant negative impact of size on profitability, that is, as the firm size increases, profitability decreases and a significant negative impact of debt-equity ratio on profitability, that is, as debt capital increases in proportion to equity, profitability decreases. Overall, the empirical findings suggest that WCM decisions significantly influence the profitability of Indian pharmaceutical companies.

The relationship of WCM cycle and profitability supports aggressive WC strategy. It implies that if the companies minimise their investment in current assets and speed up their WC cycle, it will positively influence the profitability. However, the results of individual components of WC support the conservative approach of WCM. According to results, if the companies invest a high amount of capital in current assets by adopting liberal credit policies, maintaining higher liquidity, making payment to suppliers in short duration of time and maintaining a higher inventory level, they will experience uninterrupted high sales volume and profitability and would be able to meet short-term liabilities promptly, thus, reducing the chances of bankruptcy. Thus, the results are mixed and inconclusive.

The reasons for no clear-cut results may be due to the fact that the present study is restricted to seven years secondary data of only 618 pharmaceutical companies for the period 2014–2015 to 2020–2021 and the data are downloaded from the ‘CMIE’ Prowess Database. Therefore, the reliability of the study is purely dependent upon the selection of companies, sample period, nature of industry and accuracy of data source. Future studies could be done by taking different proxies for profitability and different control variables over different time period to validate or vitiate the results of the present study. Further, more sophisticated panel data techniques like the generalised method of moments (GMM) can be employed for analysis.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Rachna Mahalwala  https://orcid.org/0000-0002-6091-6614

https://orcid.org/0000-0002-6091-6614

Aldubhani, M. A., Wang, J., Gong, T., & Maudhah, R. A. (2022). Impact of working capital management on profitability: Evidence from listed companies in Qatar. Journal of Money and Business, 2(1), 70–81.

Anton, S. G., & Afloarei Nucu, A. E. (2020). The impact of working capital management on firm profitability: Empirical evidence from the Polish listed firms. Journal of Risk and Financial Management, 14(1), 9.

Arunkumar, O. N., & Ramanan, T. R. (2013). Working capital management and profitability: A sensitivity analysis. International Journal of Research and Development, 2(1), 52–58.

Bagchi, B., & Khamrui, B. (2012). Relationship between working capital management and profitability: A study of selected FMCG companies in India. Business and Economics Journal, 2012, BEJ-60.

Bala, H., Garba, J., & Ibrahim, I. (2016). Corporate liquidity and profitability of listed food and beverages firms in Nigeria. Net Journal of Social Sciences, 4(1), 10–22.

Boisjoly, R. P., Conine Jr, T. E., & McDonald IV, M. B. (2020). Working capital management: Financial and valuation impacts. Journal of Business Research, 108, 1–8.

Breusch, T. S., & Pagan, A. R. (1979). A simple test for heteroscedasticity and random coefficient variation. Econometrica: Journal of the Econometric Society, 47(5), 1287–1294. https://doi.org/10.2307/1911963

Canina, L., & Carvell, S. A. (2008). A comparison of static measures of liquidity to integrative measures of financial and operating liquidity: An application to restaurant operators and restaurant franchisors. The Journal of Hospitality Financial Management, 16(1), 35–46.

Cheatham, L. R., Dunn, J. P., & Cheatham, C. B. (1989). Working capital financing and cash flow in the small business. Journal of Business and Entrepreneurship, 1(2), 1.

De Almeida, J. R., & Eid Jr, W. (2014). Access to finance, working capital management and company value: Evidences from Brazilian companies listed on BM&FBOVESPA. Journal of Business Research, 67(5), 924–934.

Deloof, M. (2003). Does working capital management affect profitability of Belgian firms?. Journal of business finance & Accounting, 30(3–4), 573–588.

Falope, O. I., & Ajilore O. T. (2009). Working capital management and corporate profitability: Evidence from panel data analysis of selected quoted companies in Nigeria. Research Journal of Business Management, 3, 73–84.

Filbeck, G., Zhao, X., & Knoll, R. (2017). An analysis of working capital efficiency and shareholder return. Review of Quantitative Finance and Accounting, 48(1), 265–288.

Filippini, R., & Forza, C. (2016). The impact of the just-in-time approach on production system performance: a survey of Italian industry. A review and outlook. In E. Bartezzaghi, R. Cagliano, F. Caniato & S. Ronchi (Eds), A Journey through manufacturing and supply chain strategy research (pp. 19–39), Springer.

Gallinger, G. (1997). The current and quick ratios: Do they stand up to scrutiny. Business Credit, 99(5), 22–25.

Gentry, J. A. (1994). Short-term financial management. https://www.semanticscholar.org/paper/SHORT-TERM-FINANCIAL-MANAGEMENT-Emery/0991e7a698c7c4ea7ced050ae94ab7fa2351506b

Gentry, J. A., Vaidyanathan, R., & Lee, H. W. (1990). A weighted cash conversion cycle. Financial Management, 19(1), 90–99.

Gitman, L. J. (1974). Estimating corporate liquidity requirements: A simplified approach. The Financial Review, 9(3), 79–88.

Groww. (2021, November 23). An overview of the Pharma Industry in India. https://groww.in/blog/overview-of-pharma-industry-in-india

Gujarati, D. N (2004). Basic econometrics (4th ed.). The McGraw-Hill Companies.

Hausman, J. A. (1978). Specification tests in econometrics. Econometrica, 46(6), 1251–1271.

Hingurala Arachchi, A., Perera, W., & Vijayakumaran, R. (2017). The impact of working capital management on firm value: Evidence from a frontier market. Asian Journal of Finance & Accounting, 9(2), 399–413.

IBEF. (2021). Indian pharmaceuticals industry. https://www.ibef.org/industry/pharmaceutical-india#:~:text=The%20Indian%20pharmaceutical%20sector%20is,from%2013.7%25%20in%20July%202020

Ismail, I., & Bandara, R. M. S. (2015). The impact of working capital management on profitability: Expolanka case study.

Janjua, A. R., Asghar, A., Munir, U., Raza, A., Akhtar, N., & Shahzad, K. (2016). Influence of liquidity on profitability of cement sector: Indication from firms listed in Pakistan stock exchange. Business Management Dynamics, 6(5), 1.

Jaworski, J., & Czerwonka, L. (2022). Profitability and working capital management: evidence from the Warsaw Stock Exchange. Journal of Business Economics and Management, 23(1), 180–198.

Khan, M. M., Shafique, D. Z., Safdar, M. Z., Mustafa, K., Awan, A. M., & Qasim, A. (2020). Impact of working capital management on firm’s profitability (a case of telecom sector in Pakistan). International Journal of Management (IJM), 11(7), 1494–1502.

Lazaridis, I., & Tryfonidis, D. (2006). Relationship between working capital management and profitability of listed companies in the Athens stock exchange. Journal of Financial Management and Analysis, 19(1), 12.

Levin, A., Lin, C.-F., & James Chu, C.-S. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1–24.

Maddala, G. S., & Wu, S. (1999). A comparative study of unit root tests with panel data and a new simple test. Oxford Bulletin of Economics and Statistics, 61(s1), 631–652.

Mandal, N., & Goswami, S. (2010). Impact of working capital management on liquidity, profitability and noninsurable risk and uncertainty bearing: A case study of Oil and Natural Gas Commission (ONGC). Great Lakes Herald, 4(2), 21–42.

Mandipa, G., & Sibindi, A. B. (2022). Financial performance and working capital management practices in the retail sector: Empirical evidence from South Africa. Risks, 10(3), 63.

Mohamad, N. E. A. B., & Saad, N. B. M. (2010). Working capital management: The effect of market valuation and profitability in Malaysia. International Journal of Business and Management, 5(11), 140.

Moss, J. D., & Stine, B. (1993). Cash conversion cycle and firm size: A study of retail firms. Managerial Finance, 19(8), 25–34.

Nazir, M. S., & Afza, T. (2009). Impact of aggressive working capital management policy on firms’ profitability. IUP Journal of Applied Finance, 15(8), 19–30.

Ogundipe, S. E., Idowu, A., & Ogundipe, L. O. (2012). Working capital management, firms’ performance and market valuation in Nigeria. World Academy of Science, Engineering and Technology, 61(1), 1196–1200.

Pandey, N. S., Sugumari, G., & Azhagaiah, R. (2016). The impact of working capital management on profitability of pharmaceutical industry in India. Pacific Business Review International, 9(6), 1–7.

Paul, P., & Mitra, P. (2018). Analysis of the effect of working capital management on profitability of the firm: Evidence from Indian steel industry. Asia-Pacific Journal of Management Research and Innovation, 14(1–2), 32–38.

Raheman, A., & Nasr, M. (2007). Working capital management and profitability—Case of Pakistani firms. International Review of Business Research Papers, 3(1), 279–300.

RBI. (2021, July 15). Drivers of Indian pharmaceuticals exports. https://www.rbi.org.in/Scripts/BS_ViewBulletin.aspx?Id=20379#:~:text=The%20Indian%20pharmaceutical%20sector%20contributes,the%20country’s%20total%20merchandise%20exports

Richards, V. D., & Laughlin, E. J. (1980). A cash conversion cycle approach to liquidity analysis. Financial Management, 9(1), 32–38.

Samiloglu, F., & Akgün, A. İ. (2016). The relationship between working capital management and profitability: Evidence from Turkey. Business and Economics Research Journal, 7(2), 1.

Shakoor, F., Khan, A. Q., & Nawab, S. (2012). The inter-linkages of working capital and profitability in Pakistan (2001–2010). Academic Research International, 3(2), 562.

Sharma, A. K., & Kumar, S. (2011). Effect of working capital management on firm profitability: Empirical evidence from India. Global Business Review, 12(1), 159–173.

Smith, K. (1980). Profitability versus liquidity tradeoffs in working capital management. Readings on the Management of Working Capital, 42(1), 549–562.

Singhania, M., Sharma, N., & Yagnesh Rohit, J. (2014). Working capital management and profitability: Evidence from Indian manufacturing companies. Decision, 41(3), 313–326.

Tauringana, V., & Afrifa, G. A. (2013). The relative importance of working capital management and its components to SMEs’ profitability. Journal of Small Business and Enterprise Development, 20(3), 453–469.