Review of Professional Management

Search

Search

1Banasthali Vidyapith, Jaipur, Rajasthan, India

2Department of Commerce and Management, Banasthali Vidyapith, Jaipur, Rajasthan, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Herding is a phenomenon which has become a matter of curiosity among researchers. As herding amplifies the reaction of the retail investors to the developments in the stock market, and researchers are finding an answer to this problem in the personality traits of the investors. With a sample size of 100 respondents, the research took place in Delhi-NCR. Data collection took place with the help of a structured questionnaire. In this process, factor analysis was used to identify key variables, and multiple regression test was conducted to ascertain the association between the two variables. The study concluded that agreeableness and neuroticism were the personality traits which were highly vulnerable to herding bias. The findings of the study were that neuroticism and agreeableness are the two personality traits which are highly vulnerable to the problem of herding in stock market, whereas other personality traits did not show any significant relation with herding bias. The research will be immensely beneficial for the research advisors to develop plans in accordance with personality traits of the upcoming investors to save them from the fluctuations in the stock market.

Delhi-NCR, herding, multiple regression, personality traits

Introduction

Developments in the stock market have always been perplexing and yet attracted people from all walks of life to earn additional returns on their investments. The task of understanding the behaviour of retail investors becomes tedious with the application of traditional theories of finance as it presumes investors to be rational.

To address this lacunae behavioural finance as a separate discipline evolved to understand the behavioural facets of investors to find the root cause of their irrational decisions and hence has been relied upon by experts to delve deeper into the matters of investing pattern of retail investors (Barnewall, 1987; Chang, 2008; Kumar & Goyal, 2015).

Herding bias is another important bias which affects the decision-making of the investors and pushes them towards irrationality. During the herding bias investors instead of using their calculations, simply follows others in their footsteps (Blythe, 2013; Borghans, 2008; Clark-Murphy & Soutar, 2004; Keynes, 1930; Kumar & Goyal, 2015).

Personality is another important part of our psychology and acts as a motivator to propel investors to act in a certain way and germinates inclination in them to invest in a particular pattern and resulting in exhibition of different biases while investing. Manu’s previous studies have found cause and effect relations between the two variables (Kumar & Goyal, 2015; Liang & Kelson, 2018).

As the Indian economy is counted among the fastest-growing economies, analysing the equation between the two variables assumes even more importance.

Literature Review: Herding Behaviour

Herding bias is another feature that has been primarily tracked by many experts to understand the behaviour and actions of investors facing this bias, as the investors under the influence of herding bias tend to follow other people. Furthermore, herding bias is mainly held responsible for creating artificial bubbles in the market and heavily swayed the investors’ decisions in those turbulent phases (Chiang et al., 2013; Lakshman et al., 2016; Nofsinger, 1999; Vo & Phan, 2016).

Previous studies have indicated the prevalence of herding bias in advanced as well as emerging or developing economies but some notable differences emerged in relation to Chinese and Indian investors, Chinese investors usually got influenced by herding bias during a downward spiral in the market, whereas Indian people usually exhibit herding bias during the bullish trend in the market as per the previous studies (Fama, 1970; Guney et al., 2017; Lao & Singh, 2011).

Many reasons can be cited for the prevalence of herding bias in the market usually people behave differently in relation to any piece of information and sometimes they purposely follow other people in terms of investment (Economou et al., 2018).

Personality Traits and Linkages with Investment Decisions

Human beings are known to have different mindsets and personalities as well, this difference of opinion usually results in different approaches towards investment. Personality in this way leaves a deep imprint on the investing style of any person. Previous studies have always found linkages between personality traits and their usual reaction to the movements in the stock market. However, past studies were mostly focused on correlating personality traits with portfolio decisions but less on proclivity towards different biases (Sreedevi & Chitra, 2011).

In the behavioural finance domain, to understand or carry out research in the area of personality traits, the theory of Big Five personality traits has gained a lot of credibility among the researchers, according to this theory personalities are divided among the following five categories, namely, extraversion, neuroticism, openness, conscientiousness and agreeableness (Costa & Mcrae, 1992; Mayfield et al., 2008).

Many previous studies have relied upon the Big Five personality model to carry out their research studies and their results have been documented to understand the relation between personality traits and different variables, it also highlights the estimating of the impact of personality traits (Sadi et al., 2008).

Hypothesis Development

The study strives to explore the relationship between Big Five personality traits and herding bias in the investment behaviour of Indian investors. The following hypothesis were framed to guide the study:

H1: Herding bias is significantly impacted by neuroticism.

H2: Herding bias is significantly impacted by extraversion.

H3: Herding bias is significantly impacted by openness.

H4: Herding bias is significantly impacted by agreeableness.

H5: Herding bias is significantly impacted by conscientiousness.

Methodology

Questionnaire

This study employed a structured questionnaire to collect data pertaining to behavioural biases and personality traits (Table 1). Questions related to personality traits were framed with the Big Five personality model.

Table 1. Personality Traits and their Features.

The questionnaire was segregated into three parts, the first part was dealing with the demographic profile of the respondents, the second part dealt with questions related to behavioural biases and the third part eventually carried questions related to personality traits five-point Likert Scale was used to assess the responses from the investors.

Data

The study was conducted on a sample size of 100 respondents of the National Capital Region. The data collection took place with the help of a questionnaire based on previous studies, to analyse the relation.

Sample

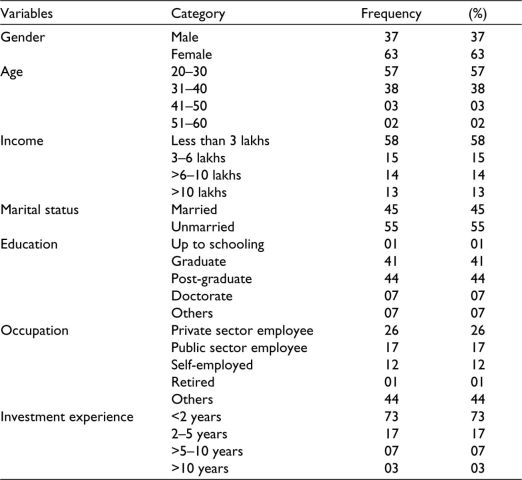

In the sample taken to study the behaviour of the Indian investors, female investors were outnumbering male investors. Education wise the respondents were not highly educated but fairly educated. In the annual income segment, investors were mostly from middle income, and experience wise most of the investors were in the initial stages of the investment cycle. Further, in terms of age, more than half the number of respondents were in their twenties. The same trend was observed in the case of marital status. Details about the demographic profile are given in Table 2.

Table 2. Details of the Sample.

Data Analysis

The study involved the use of reliability test, exploratory factor analysis and multiple regression test to analyse the data in the study and examine the hypotheses set in the study.

Reliability Assessment

Before starting the analysis of data to arrive at any result, it is essential to examine the reliability of the variables in the study. To assess the reliability Cronbach’s alpha test was performed to check the internal reliability of the constructs. A construct is considered reliable when its alpha value is more than 0.70. Summarised results of the Cronbach’s alpha test are provided in Table 3.

Table 3. Results of the Cronbach’s Alpha Test.

Exploratory Factor Analysis

After performing Cronbach’s alpha, it is essential to identify important factors so that concentrated studies can be focused upon. Using principal component analysis, the various factors are judged on the basis of factor loadings, minimum factor loading for particular factor is 0.50, and variables loading below 0.50 are not considered in the studies.

The significance of correlation among variables is adjudged by Bartlett’s test of sphericity, and the result of the test is significant hinting towards high correlation among variables.

During the factor analysis, some factors like Neuro 1 (I often feel inferior to others) were found to be loading onto other factors and hence removed. In addition to this, OP4 was loading onto other variables and Agreeable 1 and 2 were removed for the same reasons.

Testing of Hypotheses

The study proposes to study the imprint of personality traits on herding bias with the help of the hypothesis set above:

H1: Herding bias is significantly impacted by neuroticism.

H2: Herding bias is significantly impacted by extraversion.

H3: Herding bias is significantly impacted by openness.

H4: Herding bias is significantly impacted by agreeableness.

H5: Herding bias is significantly impacted by conscientiousness.

Table 4 shows the details about the regression model. Herding bias was the dependent variable whereas personality traits were taken as independent variables.

Table 4. Details about the Regression Model.

Note: aPredictors: (Constant), conscientiousness, extraversion, neuroticism, openness, and agreeableness.

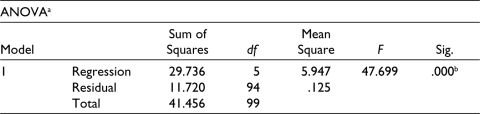

The multiple regression test was conducted involving independent variables in the form of personality traits and herding bias as dependent variables. Table 5 suggests the overall significance of the regression model, which is below 0.01 and considered highly significant.

Table 5. Overall Significance of the Regression Model.

Notes: aDependent variable: Herding.

bPredictors: (Constant), conscientiousness, extraversion, neuroticism, openness, agreeableness.

To assess the individual impact of the personality traits on the herding bias, coefficients were further examined and on examination, we found that neuroticism and agreeableness were the two variables which had significant relation with herding bias, as can be seen in Table 6 and Table 7, both the variables, namely, neuroticism and agreeableness are showing p-value = .00 which is highly significant. Other variables did not have significant relation with herding bias.

Table 6. Assessment of Variables.

Note: aDependent variable: Herding.

Table 7. Individual Regression Weights.

.jpg/10_1177_09728686231180968-table7(2)__480x137.jpg)

Note: p < .05.

Conclusion

The study examines the linkages between personality traits and herding bias while taking investment decisions in the case of retail investors. Retail investors nowadays are not afraid of investing in the stock market for getting additional returns and of late they have started playing a prominent role in the stock market besides foreign portfolio investors. The presence of retail investors works as a counterweight to the foreign portfolio investors. As already personality of retail investors are classified into the following five categories, namely, neuroticism, agreeableness, openness, conscientiousness and extraversion, whereas herding bias is the propensity of individuals to follow other people while taking investment decisions.

Neurotic investors usually are fearful and they are not known to take sound positions on their investments and volatility is easily observable in their actions. Any sudden spurt or drop in stock prices make them behave irrationally, and they start following other people for making investment decisions. This research also corroborates the findings of past research studies and found a significant relation between neuroticism and herding bias. Financial advisors can recommend financial products to such a category of investors in which there is less exposure to the equity market or they should be encouraged to invest in the stock market through the route of systematic investment plan and also push them to use stop-loss while actively trading.

Further, people associated with conscientiousness and extraversion are known to be resolute in their decision-making and they are known to systematically plan their investments and carry out research studies before entering the market. Due to this, our study did not find any linkage between herding bias and conscientiousness as well as extraversion. Conscientiousness usually propels investors towards investing in safe stocks, and they generally prefer large caps.

In addition to this, agreeable investors are considered very empathetic and they listen to the advice of all the people around them. However, the major disadvantage associated with agreeable investors is they lack self-discipline, and they attach a lot of importance to the recent events that have taken place in the stock market making it highly vulnerable to the herding bias.

Limitations of the Study

The study is based on the respondents residing in Delhi-NCR, small sample size used in the study cannot be used for a more generalised conclusion and for this data from other cities should be included. Further studies can be conducted by employing questionnaires and conducting interviews to collect data in a more credible manner. Future research can be conducted by involving more variables to have a deeper understanding of the investment decisions.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Barnewall, M. (1987). Psychological characteristics of the individual investor in asset allocation for the individual investor. The Institute of Chartered Financial Analysts.

Blythe, J. (2013). Cyber security in the workplace: Understanding and promoting behaviour change. Proceedings of CHItaly 2013 Doctoral Consortium, 1065, 92–101. https://ceur-ws.org/Vol-1065/paper11.pdf

Borghans, L., Duckworth, A. L., Heckman, J. J., & Ter Weel, B. (2008). The economics and psychology of personality traits. Journal of Human Resources, 43(4), 972–1059.

Chang, C. H. (2008). The impact of behavioral pitfalls on investors’ decisions: The disposition effect in the Taiwanese warrant market. Social Behavior and Personality: An International Journal, 36(5), 617–634.

Chiang, T. C., Li, J., Tan, L., & Nelling, E. (2013). Dynamic herding behavior in Pacific-Basin markets: Evidence and implications. Multinational Finance Journal, 17(3/4), 165–200.

Clark-Murphy, M., & Soutar, G. N. (2004). What individual investors value: Some Australian evidence. Journal of Economic Psychology, 25(4), 539–555.

Costa, P. T., Jr., & McCrae, R. R. (1992). Four ways five factors are basic. Personality and Individual Differences, 13(6), 653–665.

Economou, F., Hassapis, C., & Philippas, N. (2018). Investors’ fear and herding in the stock market. Applied Economics, 50(34–35), 3654–3663.

Fama, E. F. (1970). Efficient capital markets: A review of theory and empirical work. The Journal of Finance, 25(2), 383–417.

Guney, Y., Kallinterakis, V., & Komba, G. (2017). Herding in frontier markets: Evidence from African stock exchanges. Journal of International Financial Markets, Institutions and Money, 47, 152–175. https://doi.org/10.1016/j.intfin.2016.11.001

Keynes, J. M. (1930). Treatise on money. Macmillan.

Kumar, S., & Goyal, N. (2015). Behavioural biases in investment decision making: A systematic literature review. Qualitative Research in Financial Markets, 7(1), 88–108.

Lakshman, M. V., Basu, S., & Vaidyanathan, R. (2013). Market-wide herding and the impact of institutional investors in the Indian capital market. Journal of Emerging Market Finance, 12(2), 197–237.

Lao, P., & Singh, H. (2011). Herding behaviour in the Chinese and Indian stock markets. Journal of Asian Economics, 22(6), 495–506.

Liang, H. Y., & Kelsen, B. (2018). Influence of personality and motivation on oral presentation performance. Journal of Psycholinguistic Research, 47(4), 755–776.

Nofsinger, J. R., & Sias, R. W. (1999). Herding and feedback trading by institutional and individual investors. The Journal of Finance, 54(6), 2263–2295.

Sadi, R., Asl, H. G., Rostami, M. R., Gholipour, A., & Gholipour, F. (2011). Behavioral finance: The explanation of investors’ personality and perceptual biases effects on financial decisions. International Journal of Economics and Finance, 3(5), 234–241.

Sreedevi, V. R., & Chitra, K. (2011). Does personality traits influence the choice of investment? The IUP Journal of Behavioral Finance, 8(2), 47–57.

Vo, X. V., & Phan, D. B. A. (2016). Herd behavior in emerging equity markets: Evidence from Vietnam. Asian Journal of Law and Economics, 7(3), 369–383.