Review of Professional Management

Search

Search

Animesh Bhattacharjee1 , Joy Das2 and Sunil Kumar3

, Joy Das2 and Sunil Kumar3

1 The Techno India University Tripura, Maheshkhola, Tripura, India

2 Department of Commerce, Nagaland University, Kohima Campus Nagaland, India

3 The ICFAI University Tripura, Kamalghat, Tripura, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

The market mood index is a novel sentiment indicator for the Indian stock market, designed to assess the overall mood within the market. This tool purportedly enables investors to become aware of their emotional state and predispositions that may impact their decision-making processes. Given the context, this study aims to explore the relationship between the market mood index and the Indian stock market index in order to verify the effectiveness of the index. The study used data from March 2012 to May 2023. Various analytical techniques are utilised for this purpose, such as unit root tests, cointegration tests, pair-wise Granger causality tests and the DCC-GARCH approach. The results indicate that the Indian stock market and the market mood index are cointegrated in the long term, suggesting a sustained connection between them. Additionally, a feedback mechanism between the variables is apparent. The GARCH analysis confirms the presence of volatility transmission from the market mood index to the Indian stock market in both the long and short term. Furthermore, the DCC model reveals the changing correlation of volatility between the market mood index and the Indian stock market. Trading tactics should be formulated with the association between the two variables in mind. It can be concluded that the studied index, developed by TickerTape, shows good association with the market index suggesting being a good investment indicator.

India, mood index, stock market, ARDL, volatility

Traditional theories of the stock market have long been grounded in the assumption of rationality. Nonetheless, contemporary research conducted by Verma et al. (2008), Dimson et al. (2004) and Singh (2012) have revealed that such an assumption is fundamentally flawed. Instead, the irrational behaviour of investors has emerged as a critical factor in the market’s fluctuations. This irrationality is often attributed to a number of factors, including cognitive dissonance, confirmation bias, endowment effect, mental accounting, active trading and loss aversion. It is clear that these psychological phenomena have a significant impact on the market’s performance and cannot be ignored in any analysis of its dynamics.

Over the previous 20 years, there has been a notable examination of sentiment analysis within the realm of finance (Prasad et al., 2023). Scholars have engaged in the application of sentiment analysis as a means of constructing an investor sentiment index (ISI), which reveals the mood of the market. Investor sentiment pertains to the anticipation held by market participants with respect to future cash flows as well as the investment risk (De Long et al., 1990). Baker and Wurgler (2007), Pandey and Sehgal (2019), Alsabban and Alarfaj (2020), PH and Rishad (2020) and Pillada and Rangasamy (2023) constructed ISI and measured the indexes’ efficacy in predicting the volatility of stock markets.

The market mood index, a novel market sentiment indicator, serves to prognosticate opportune moments for entering and exiting the stock market. This index is computed by taking into consideration six distinct factors. The first factor, termed the FII activity, is established by gauging the net open interest of foreign institutional investors in index Futures on the Nifty Stock Exchange. The second factor, known as volatility and skew, is represented by the Indian VIX index. The third factor pertains to the momentum of the Nifty and is determined by the variance between the 90-day and 30-day exponential moving averages. The fourth factor, referred to as market breadth, is derived by dividing the AD ratio by the AD volume. The fifth and sixth factors are related to the price strength and demand for gold, respectively. Given that the market mood index is an indicator of the sentiment prevailing in the Indian stock market, it evinces a significant linkage with the Indian stock market, particularly in the short term, as it is classified as a technical indicator.1

Against this backdrop, the present study aims to delve into an in-depth analysis of the interrelatedness between the market mood index and the Indian stock market, as represented by the Nifty 50 Index.

The following is a detailed organisation and structure of the subsequent portions of this study: A thorough review of the literature is provided in the second section; information about the data and methodology used in this study is provided in the third section; by using various econometric techniques, a thorough and meticulous analysis of the data is provided in the fourth section; and lastly, a summary of the conclusions and their implications for investors are provided in the fifth section.

Literature Review

In the current decade, extensive research has been carried out to identify the factors that influence investors’ trading behaviour. Additionally, several researchers have devised diverse sentiment indices for investors to measure the impact of their sentiment on stock market volatility. A concise summary of these research initiatives is presented below.

Baker and Wurgler (2007) employed a distinctive ‘top-down’ methodology to illustrate the feasibility of gauging investor sentiment. The findings of their study indicate that waves of sentiment bear noteworthy consequences for both individual firms and the stock market in its entirety. Hudson and Green (2015) investigated the effect of investor sentiment on equity returns in the United Kingdom by constructing two indices. The findings suggested that US investor sentiment can help predict UK equity returns. Using multivariate Markov-switching, Chung et al. (2012) examined the predictive power of investor sentiment for stock returns across the state of economic expansion and recession. The findings showed that during a recession state, the sentiment’s predictive power is insignificant. The finding of Lutz (2015) suggested that during times when the federal funds rate was constrained at zero, the implementation of expansive unconventional monetary policies exerted a substantial and favourable influence on investor attitudes.

Pandey and Sehgal’s study (2019) involved experimentation with alternative investor sentiment indices and an evaluation of sentiment-based factors in asset pricing, leading to the development of a superior composite sentiment index. Additionally, they conducted an evaluation of the influence of sentiment-based factors in asset pricing to provide an explanation for notable equity market anomalies, including size, value and price momentum, for India. The results of their research confirmed that the composite sentiment index that they developed leads to other currently prevalent sentiment indices in the investment literature.

Alsabban and Alarfaj (2020) analysed the overconfidence behaviour among investors in the Saudi stock market. To examine this phenomenon, a market-wide VAR model was employed. Their findings indicated that overconfidence is a pervasive trait among Saudi market investors. PH and Rishad (2020) conducted a study to investigate the impact of irrational investors’ sentiments on stock market volatility in India. The research involved the development of an irrational sentiment index through principal component analysis and its incorporation into the GARCH and Granger causality framework for assessing its influence on volatility. Findings indicated that irrational sentiment plays a significant role in driving excessive market volatility, a crucial insight for individuals such as retail investors and portfolio managers aiming to optimise their portfolios for maximum profitability. Baek et al. (2020) undertook an in-depth investigation at the industrial level to ascertain whether the US stock market exhibited any fluctuations during the COVID-19 period. The findings revealed that stock market volatility was significantly influenced by certain economic factors and held a high sensitivity towards COVID-19–related news. Wang et al. (2022) used the turnover ratio as a sentiment proxy and GARCH models to confirm the influence of investor sentiment on stock returns. Pillada and Rangasamy (2023) investigated the impact of investor sentiment on the volatility of the real estate market between November 2019 and June 2022. To achieve this objective, the scholars employed the principal component analysis methodology to develop an ISI. The research outcomes revealed the presence of an asymmetric effect of the sentiment on the realty sector and affirmed the existence of a bidirectional correlation between asset return and investor sentiment. Dash and Maitra (2018) examined the relationship between the Indian stock market and investor sentiment using a wavelet approach. Their research yielded proof that the investment activities of both short-term and long-term investors were closely intertwined with sentiment, highlighting the interconnected nature of sentiment and investment decisions. The literature survey above indicates that the sentiment of investors is a crucial factor in elucidating stock market volatility. Various methodologies have been employed by researchers to assess investor sentiment. Some researchers have viewed the consumer confidence index as a representation of investor sentiment, whereas other scholars have produced their own indices for this purpose.

A sentiment indicator, introduced recently by TickerTape, is designed to gauge the mood of investors. It is claimed that the new market mood index has the capability to assess the current behaviour of the overall market. To validate this argument, advanced econometric techniques must be employed. Consequently, the investigation endeavours to scrutinise the correlation between the market mood index and the Nifty 50 Index ranging from 2012 to 2023 by utilising methodologies such as the unit root test, cointegration test, pair-wise Granger causality test and DCC-GARCH. The article aims to answer the following questions: (a) Is there a long-run equilibrium relationship between the market mood index and the Nifty 50 Index? (b) Is there short-run predictive causality between the market mood index and the Nifty 50 Index? (c) Is there volatility spillover between the market mood index and the Nifty 50 Index? (d) Is co-movement (correlation) between the market mood index and the Nifty 50 Index time-varying? (e) What effect did the COVID-19 pandemic have on the co-movement of the market mood index and the Nifty 50 Index?

The study has established the following hypotheses for examination:

H1: There is no cointegrating relationship between the market mood index and the Nifty 50 Index.

H2: The short-run predictive causality does not flow from the market mood index and the Nifty 50 Index or vice versa.

H3: There is no short-run volatility spillover from the market mood index to the Nifty 50 Index.

H4: There is no long-run volatility spillover from the market mood index to the Nifty 50 Index.

H5: There is no time-varying co-movement (correlation) between the market mood index and the Nifty 50 Index.

Data and Methodology

Data Description

The data series (market mood index and Nifty 50 Index) being used in this study is obtained from the TickerTape website and Yahoo Finance covering the period between 12 March 2012 and 2 May 2023. EViews 10.0 economteric software and RStudio are used to analyse the dataset. The market mood index (proxied for market sentiment) ranges from 0 to 100. A value of less than 20 indicates a high extreme fear zone (suggesting a good time to open a fresh position) while a value of more than 80 indicates a high extreme greed zone (suggesting to be cautious in opening fresh positions).

Econometric Methods

The study uses two types of data, namely original index series and return series. The original index series is used for determining the cointegration and direction of predictive causality between the market mood index and the Nifty 50 Index. For determining the short-run and long-run spillover from the market mood index and the Nifty 50 Index, we have used the return series. Both the original index series and the return series are subject to unit root testing using the augmented Dickey–Fuller (ADF) test. The ADF test expands the Dickey–Fuller test equation to include high-order regressive process in the model. The null hypothesis of the ADF test is that a unit root is present in a first-order AR model. The ADF test is executed using the following equation:

The autoregressive distributed lag (ARDL) bounds test, developed by Pesaran et al. (2001), is applied to determine the cointegration between the market mood index and the Nifty 50 Index. Many researchers used the ARDL bounds test as a cointegration test; for example, Bhattacharjee and Das (2022) investigated the cointegration between monetary variables and the Indian stock market, Sahoo et al. (2021) determined the long-run relationship among information and communication technology, financial development and environmental sustainability in India, Furthermore, in a recent study Seth and Kumar (2023) employed the ARDL model to study the long-run equilibrium linkage between the market mood index and Indian stock market.

We employ a pair-wise Granger causality test to investigate the direction of predictive causality between the variables. The Granger causality approach statistically tests the hypothesis of whether variable X Granger causes variable Y and vice versa. If the probability (p) value is less than any alpha level, then the null hypothesis would be rejected. There can be four outcomes of the pair-wise Granger causality test. First, if variable X granger causes variable Y, then it can be said that variable X helps in the prediction of variable Y. If variable Y Granger causes variable X, then it can be said that variable Y is helpful in predicting variable X. There can be a situation where both variable X and variable Y Granger causes each other. Under such circumstances, it might be said that a feed mechanism exists between the variables. The last outcome of the test is when neither variable X nor variable Y does not Granger cause each other. It implies that no predictive causality exists between the variables. An earlier study by PH and Rishad (2020) employed the Granger causality test to determine the flow of causality between investor sentiment and stock market index.

For determining the short-run and long-run spillover from the market mood index and the Nifty 50 Index and investigating whether time-varying co-movement exists between the variables, the dynamic conditional correlation–generalised autoregressive conditional heteroskedasticity (DCC-GARCH) approach is applied. DCC-GARCH, or dynamic conditional correlation GARCH, is a statistical model used in finance to estimate the time-varying correlation between asset returns. It is an extension of the traditional GARCH model, which models the volatility of financial returns, but it also incorporates the correlation dynamics between different assets.

In the DCC-GARCH model, each asset’s volatility is modelled using a standard GARCH process, while the correlation between assets is modelled using a separate equation that captures the dynamics of correlation. This allows for a more accurate representation of how correlations between assets change over time, which is particularly useful in risk management, portfolio optimisation and other areas of financial analysis where understanding the interdependencies between assets is important. DCC-GARCH models are widely used in empirical finance because they can capture the time-varying nature of correlations, which are known to be important for portfolio diversification and risk management. They are particularly valuable during periods of financial turbulence when correlations between assets tend to increase.

GARCH and DCC-GARCH techniques have been used by Haritha and Rishad (2020) and Pillada and Rangasamy (2023) to examine the relationship between investor sentiment and stock market volatility.

Results

Both the original index series are subject to the ADF unit root test. From the observation, it can be said that the market mood index is stationary at a level while the Nifty 50 Index achieves stationarity at first difference. Thus, it can be said that the market mood index is integrated of order 0 or I(0) and the Nifty 50 Index is integrated of order 1 or I(1) (see Table 1). Since the variables are mixed order integrated, the ARDL bounds test is employed to investigate whether both the market mood index and the Nifty 50 Index are cointegrated. To execute the ARDL bounds test, optimum lag length is required. The optimum lag order is found to be eight months (refer to Table 2).

Table 1. Unit Root Test Result (Original Index Series).

Notes: Auto-selection = SIC, trend and intercept included in the test equation.

*Significant at the 1% level.

Table 2. Lag Selection Criterion.

Table 3 presents the result of the ARDL bounds test. In the case of the ARDL bounds test, if the computed F-statistic is more than the critical values at the upper bound, then we can say that there is cointegration or a long-run relationship between the variables. If the computed F-statistic is in between the lower bound critical value and upper bound critical value, then it can be said that there is inconclusive evidence of cointegration. If the computed F-statistic is lower than the critical value at the lower bound, it can be said that there is no cointegration. It can be seen from the table that the calculated F-statistic (62.609) is greater than the upper bound critical values at 1% (5.58), 5% (4.16) and 10% (3.51) levels, suggesting that the variables are strongly cointegrated. Thus, H1 can be rejected, which means that there is a long-run equilibrium relationship between the market mood index and the Nifty 50 Index.

Table 3. F-Bounds Test.

The direction causality is investigated by employing pair-wise Granger causality test and the results are summarised in Table 4. We document that there is bidirectional causality between the Nifty 50 Index and the market mood index, suggesting that the Nifty 50 Index helps in predicting the market mood index and vice versa. Thus, H2 can be rejected, indicating that short-run predictive causality flows from the market mood index and the Nifty 50 Index and vice versa.

Table 4. Pair-wise Granger Causality Test (at 8 Lags).

Note: *Significant at the 1% level.

For volatility modelling, both the index series are transformed into return series and are subjected to a stationarity test (unit root test). The results of the ADF unit root test are presented in Table 5. The results indicate that returns of both the market mood index series and the Nifty 50 Index series are stationary at a level and, hence, fit for DCC-GARCH.

Table 5. Unit Root Test Results (Return Series).

Notes: Auto-selection = SIC, trend and intercept included in the test equation.

*Significant at the 1% level.

The estimates of the DCC-GARCH (1, 1) model are summarised in Table 6. In the table, mu stands for the overall mean and omega denotes the intercept term. Beta1 represents the impact of past changes. The table shows that the sum of the ARCH and the GARCH term is less than 1, for both mmi (α+β = 0.9465) and nii (α+β = 0.9797), showing that there is a reduction in unpredictability perseverance over the long run.

Table 6. DCC-GARCH Estimates.

Notes: mmi, market mood index; nii, Nifty 50 Index.

P value is given in parentheses.

Furthermore, the dcc terms, that is, dcca1 and dccb1 (which indicates volatility spillover), are positive and significant, which shows that there is volatility spillover both in the short run and long run from the market mood index to the Nifty 50 Index. Thus, H3 and H4 are rejected.

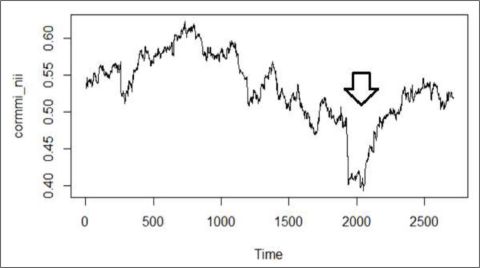

Figure 1 exhibits the dynamic conditional correlation between the market mood index and the Nifty 50 Index. From the figure, it can be seen that the volatility correlation between the variables lingers around 0.40 to 0.60 throughout the studied time frame. The volatility correlations reached their peak in May 2015. However, in 2020, the volatility correlation between the market mood index and the Nifty 50 Index saw a steep descent, possibly driven by the worldwide spread of COVID-19 (a black swan event)2 and also due to the uncertain economic events taking place. As per the result presented in Figure 1, H5 can be rejected.

Figure 1. Time-varying Correlation Between Market Mood Index and Nifty 50 Index from 12 March 2012 to 2 May 2023.

Note: The downward arrow sign shows the period of the COVID-19 pandemic.

Conclusion

The study’s main objective is to explore the linkage between the market mood index and the Indian stock market. We have established the ARDL bounds test and DCC-GARCH approach to explore the linkage between the variables. From the analyses, we have drawn four conclusions.

First, the market mood index is found to have a long-run equilibrium relationship with the Indian stock market. Second, a feedback mechanism is observed between the market mood index and the Indian stock market, which suggests that the market mood index helps in predicting the Indian stock market in the short run. Third, DCC-GARCH estimates indicate that there is volatility spillover from the market mood index to the Indian stock market both in the long run and short run. Fourth, there is a time-varying (usually ranging from 0.40 to 0.60) correlation between the volatility of the market mood index and the Indian stock market, and the COVID-19 pandemic resulted in a drop in the correlation between the variables under study. Our findings show the new sentiment index to be connected with the Indian stock market in the long run. In the short run, the market mood index volatility is a strong predictor of the volatility of the Indian stock market.

The findings are extremely important for scholars, policymakers and traders. Developing nations such as India exhibit informational inefficiency and constrained arbitrage opportunities. Consequently, these financial markets could be susceptible to sentiment or emotional biases. Our investigation offers empirical support for the bidirectional relationship between investor sentiment and the stock market index. Therefore, trading tactics should be formulated with this association in mind. Moreover, such findings could assist policymakers in implementing suitable measures to prevent the occurrence of speculative bubbles or market crashes during periods of excessive optimism and fear. Furthermore, the studied index, developed by TickerTape, shows a good association with the market index, suggesting it is a good investment indicator.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iDs

Animesh Bhattacharjee https://orcid.org/0000-0003-2513-1253

Sunil Kumar https://orcid.org/0000-0003-4167-598X

Notes

Alsabban, S., & Alarfaj, O. (2020). An empirical analysis of behavioral finance in the Saudi stock market: Evidence of overconfidence behavior. International Journal of Economics and Financial Issues, 10(1), 73–86. https://doi.org/10.32479/ijefi.8920

Baek, S., Mohanty, S. K., & Glambosky, M. (2020). COVID-19 and stock market volatility: An industry-level analysis. Finance Research Letters, 37, 101748.

Baker, M., & Wurgler, J. (2007). Investor sentiment in the stock market. Journal of economic perspectives, 21(2), 129–151.

Bhattacharjee, A., & Das, J. (2022). Assessing the long-run and short-run effect of monetary variables on stock market in the presence of structural breaks: Evidence from liberalised India. The Review of Finance and Banking, 14(2), 121–131.

Chung, S. L., Hung, C. H., & Yeh, C. Y. (2012). When does investor sentiment predict stock returns? Journal of Empirical Finance, 19(2), 217–240.

Dash, S. R., & Maitra, D. (2018). Does sentiment matter for stock returns? Evidence from Indian stock market using wavelet approach. Finance Research Letters, 26, 32–39.

De Long, J. B., Shleifer, A., Summers, L. H., & Waldmann, R. J. (1990). Noise trader risk in financial markets. Journal of Political Economy, 98(4), 703–738.

Dimson, E., Marsh, P., & Staunton, M. (2004). Irrational optimism. Financial Analysts Journal, 60(1), 15–25.

Hudson, Y., & Green, C. J. (2015). Is investor sentiment contagious? International sentiment and UK equity returns. Journal of Behavioral and Experimental Finance, 5, 46–59.

Lutz, C. (2015). The impact of conventional and unconventional monetary policy on investor sentiment. Journal of Banking & Finance, 61, 89–105.

Pandey, P., & Sehgal, S. (2019). Investor sentiment and its role in asset pricing: An empirical study for India. IIMB Management Review, 31(2), 127–144. https://doi.org/10.1016/ j.iimb.2019.03.009

Pesaran, M. H., Shin, Y., & Smith, R. D. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

PH, H., & Rishad, A. (2020). An empirical examination of investor sentiment and stock market volatility: Evidence from India. Financial Innovation, 6(1), 34.

Pillada, N., & Rangasamy, S. (2023). An empirical investigation of investor sentiment and volatility of realty sector market in India: An application of the DCC–GARCH model. SN Business & Economics, 3(2), 55.

Prasad, S., Mohapatra, S., Rahman, M. R., & Puniyani, A. (2023). Investor sentiment index: A systematic review. International Journal of Financial Studies, 11(1), 6.

Sahoo, M., Gupta, M., & Srivastava, P. (2021). Does information and communication technology and financial development lead to environmental sustainability in India? An empirical insight. Telematics and Informatics, 60, 101598.

Seth, N., & Kumar, Y. (2023). Market mood index and stock market. Evidence from National Stock Exchange. Theoretical & Applied Economics, 30(1), 263–272.

Singh, S. (2012). Investor irrationality and self-defeating behavior: Insights from behavioral finance. Journal of Global Business Management, 8(1), 116.

Verma, R., Baklaci, H., & Soydemir, G. (2008). The impact of rational and irrational sentiments of individual and institutional investors on DJIA and S&P500 index returns. Applied Financial Economics, 18(16), 1303–1317.

Wang, W., Su, C., & Duxbury, D. (2022). The conditional impact of investor sentiment in global stock markets: A two-channel examination. Journal of Banking & Finance, 138, 106458.