Review of Professional Management

Search

Search

Reshma Kurussiveettil1 and K. Kanniammal1

and K. Kanniammal1

1 Department of Commerce, Avinashilingam Institute for Home Science and Higher Education for Women, Coimbatore, Tamil Nadu, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

The financial system has changed due to recent advancements in banking and insurance, but it is only available to some groups of society while excluding others, which is known as ‘financial exclusion’. Every nation strives relentlessly for comprehensive financial inclusion in order to achieve both inclusive growth and overall development. This study aims to analyse the role of the Pradhan Mantri Jan Dhan Yojna (PMJDY) on financial inclusion among tribes of Kerala. A structured schedule was used to collect primary data from 395 tribal respondents of the Attappady tribal area. The data were analysed through the statistical program for the social sciences by using the chi-square test, and the study found evidence that there is a strong association between the perception of tribes about the impact of the PMJDY scheme on financial inclusion. The results support further promoting Scheduled Tribes’ access to and use of the specific scheme in order to ensure the inclusive development of the society.

Pradhan Mantri Jan Dhan Yojna; awareness, financial inclusion, sustainable development, perception, tribes of Kerala

Introduction

India is ranked 62nd out of 74 rising nations in the World Economic Forum’s ‘Inclusive Development Index’ for inclusive development. Despite being well on its way to becoming an economy worth $5 trillion, economic inequality still exists in India (Barik & Sharma, 2019). There are several elements for inclusive economic growth. Among them, the two most important elements are complete financial inclusion and empowerment of the vulnerable. Having equitable access to formal financing results in increased investments in human capital and improved job creation. There is mounting evidence that financial inclusion increases total economic production, lowers poverty and income inequality at the national level and reduces credit risk. A stable, honest and equal financial system promotes growth. Hence, policymakers should pay attention to financial exclusion caused by various barriers, such as physical, sociocultural and psychological ones.

Access to money is a huge barrier for the poor and underprivileged, particularly in rural areas and in emerging nations like India. They are compelled to rely on shady lenders that charge them outrageous interest rates that they frequently fail to repay, increasing their debt and causing a debt cycle. The lack of financial institutions in rural areas and a lack of financial knowledge and awareness make it difficult for people to access finance. A sound financial system will improve the welfare of the populace and make it possible for money to be invested, increasing the quantity of credit available to the economy and, consequently, the creation of capital assets and economic growth. Pradhan Mantri Jan Dhan Yojna (PMJDY) was launched in 2014 by the Indian government as a component of the National Mission for Financial Inclusion. It aspires to make financial services available to all Indian people.

Low levels of poverty and income inequality are correlated with high levels of financial inclusion (Churchill & Marisetty, 2020). Therefore, we can say that PMJDY has an impact on financial inclusion. A review of the present state reveals that the PMJDY, a new inventiveness for financial inclusion, has resulted in the opening of around 12.54 million new bank accounts (as of January 2015) and deposits totalling more than .png) 5,000 crores (as of November 2014). Yet, it has been noted that the majority of the rural market is still untapped and has not been extensively investigated (Joshi & Rajpurohit, 2016). Hence in this study, we are investigating the role of the PMJDY scheme on the financial inclusion of tribes of Kerala, as they constitute one major section of marginalised groups in India.

5,000 crores (as of November 2014). Yet, it has been noted that the majority of the rural market is still untapped and has not been extensively investigated (Joshi & Rajpurohit, 2016). Hence in this study, we are investigating the role of the PMJDY scheme on the financial inclusion of tribes of Kerala, as they constitute one major section of marginalised groups in India.

Review of Literature

Numerous studies have been carried out in relation to the PMJDY scheme since it embarked as the most successful initiative of the Central Government in transforming the ‘excluded’ to as ‘included’. Shibu (2022) examines the level of awareness of the PMJDY scheme among rural women with primary data collected on a 5-point Likert scale. The analysis results reveal that the source of information significantly influences the level of rural women’s familiarity with the PMJDY plan, but schooling had no discernible influence on their level of awareness. Saini and Mittal (2020) analysed the status of the scheme and its role in financial inclusion. This study argues that in order to contribute to the country’s inclusive growth, the government and private sector banks will need to make a lot of effort. The researcher describes the advantages of PMJDY and the status of the bank accounts opened under this programme in this study. Bijoy (2017) discussed the status of financial inclusion in India through various government policies, such as Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA), Direct Benefit Transfer (DBT) and Pradhan Mantri Jan Dhan Yojna (PMJDY). The study unveils that the number of bank accounts opened by PMJDY for marginalised and underprivileged persons has increased, while the volume of transactions in these accounts has decreased. Many accounts are inactive because there is not enough revenue flowing through them or there are not enough funds to deposit. It is advised that policymakers focus on creating jobs so that everyone in India can fully access the financial system. Yadav et al. (2021) assessed how well the PMJDY has contributed to financial inclusion since its establishment. Using a Financial Inclusion Index, which is similar to the Human Development Index, they measured the level of financial inclusion enjoyed by each state of India. The study used secondary data for analysis. The study’s key finding demonstrated that a larger portion of the Indian region falls into the category of low financial inclusion. In terms of financial inclusion, southern regions score better than central, eastern and northeastern regions. Moreover, there is a strong correlation between FII and HDI. Additionally, only a few regions saw an increase in their ranking from low to medium financial inclusion, indicating that the PMJDY framework has not led the economy to a high degree of financial inclusion. By strengthening and expanding monetary organisations while also managing digital literacy, underlying developments were subsequently given institutional legitimacy. Singh et al. (2019) investigated to what extent the financially excluded folks are using the PMJDY programme’s benefits. The study undertakes a systematic review of 60 research publications on PMJDY, which aids in identifying the major problems the programme is dealing with. Several reports on the PMJDY plan and financial inclusion were also taken into consideration for a better analysis. Findings indicated that despite some constraints, such as dormant accounts, financial illiteracy, duplicate accounts, unbanked areas (4.25 lakh) and a lack of ATMs, this programme has significantly contributed to increasing access to financial services. Omar and Inaba (2020) examined how financial inclusion affects the reduction of poverty and income inequality, as well as the causes and confounding effects of each, in 116 developing nations. The findings offer solid proof that financial inclusion significantly lowers income inequality and poverty rates in developing nations. The findings support further improving marginalised populations’ access to and use of formal financial services in order to increase society’s overall well-being. Thus, from the earlier studies, it is evident that there exists a nexus between PMJDY, financial inclusion and sustainable development. Hence, the researcher is attempting to investigate the relationship among scheduled tribes, since they constitute a major portion of the vulnerable section in Kerala.

Research Gap

Researchers have offered a number of arguments for and against financial inclusion over the years. The PMJDY initiative received a major boost when the National Democratic Alliance (NDA) administration introduced it. As a result, those in the financially marginalised sector experienced a significant elevation. But the question still stands: what does PMJDY offer that prior financial inclusion initiatives did not? The government claims amazing success with this programme; hence, the question is pertinent. The accomplishment being claimed is not without controversy. Hence, this study aims to determine whether PMJDY has significantly impacted the financial inclusion aspect of the Attappady tribal region, which is the study area.

Scope of the Study

The study will throw light on the extent to which the PMJDY scheme has a role to play in financial inclusion among tribes of Kerala. The current study’s focus is mostly restricted to the scheduled tribes of Kerala who are aware of the PMJDY programme. Finding out the current level of understanding, perception and utilisation of the PMJDY scheme is the functional scope.

Objectives of the Study

Objectives of the study are as follows:

Hypotheses of the Study

The following hypotheses are derived from the study:

Methodology

Source of Data

The study is based on both primary and secondary data. The former is gathered using an organised schedule, while the latter is gathered from various public documents.

Sampling Design

As per 2011 census data, 32,956 is the total tribal population of the study area. Using the stratified random sampling technique, a total of 395 tribal respondents (as per Slovin’s formulae) were selected for the study.

Statistical Tools and Techniques

The data were examined using Microsoft Excel and the Statistical Package for Social Sciences. Frequencies, percentages and the chi-square test were applied in the statistical analysis to test the hypotheses.

Results and Discussion

Level of Awareness of Tribes on PMJDY Account

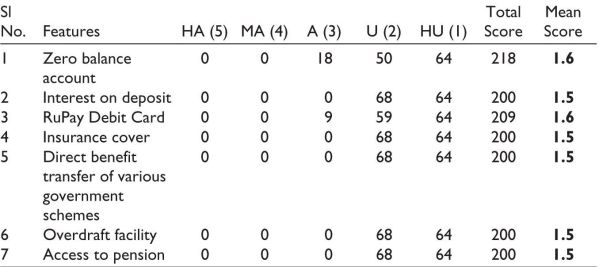

PMJDY is a national initiative for financial inclusion that aims to guarantee that everyone has affordable access to financial services, such as banking, savings and deposit accounts, remittance, credit, insurance and pensions. This programme comes with a number of extra benefits, such as DBT, interest on deposits, insurance coverage and an overdraft facility.

The mean score analysis of the seven variables used for analysis reveals an awareness level that falls between ‘highly unaware’ and ‘unaware’, with a mean score of around 1.5. The severity of the tribal sects’ lack of knowledge about the PMJDY system is indicated by the mean score. This predicament can only be changed by providing appropriate education and training. It is significant to notice that despite having a PMJDY account, they are unaware of the fundamental components of this programme. Hence, the result proves that the tribes possess only a low level of awareness about the PMJDY scheme (Table 1).

Table 1. Mean Score Analysis on Awareness Level of Tribes on Features of PMJDY Scheme.

Note: Figures in ( ) indicate the score. HA: Highly Aware, MA: Moderately Aware, A: Aware, U: Unaware, HU: Highly Unaware. The bold values are the Mean Score of each statement, based on which we interpret the result.

Perception of Tribal People About the Impact of PMJDY Scheme on Financial Inclusion

This study analysed the role of the scheme in financial inclusion from the perception of tribes in three aspects.

Access to PMJDY Accounts

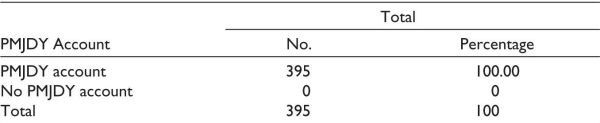

PMJDY is a well-known programme for financial inclusion created by the Indian government at the national level (Table 2). This account has no frills and can be actively maintained even when there is no balance. The programme has numerous extra advantages.

Table 2. Access to PMJDY Account.

Note: PMJDY – Pradhan Mantri Jan Dhan Yojna.

H0: There is no strong association between the perceptions of tribes with regard to the impact of the PMJDY scheme on financial inclusion in the case of the number of PMJDY account holders.

The p-value is .000, which is less than .05 at the 5% level of significance, as shown in Table 3. As a result, H1 is accepted and H0 does not stand accepted. Consequently, it is determined that ‘There is a strong correlation between the perceptions of people of different tribes about the Impact of PMJDY scheme in financial inclusion in the case of number of PMJDY account holders’ (Table 3).

Table 3. Chi-square Test—Result.

Note: *Level of significance: 5%. a3 cells (16.7%) have expected count less than 5. The minimum expected count is 0.33.

Benefits of PMJDY Accounts

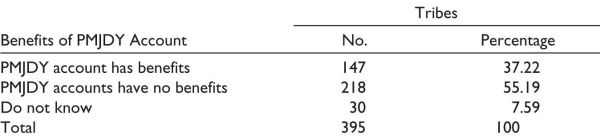

PMJDY account holders can enjoy many added benefits with the scheme. Interest on deposits, RuPay Debit Cards, accident insurance cover, direct benefit transfers and so on are some of them (Table 4).

Table 4. Benefits of PMJDY Accounts.

Source: Primary data.

Note: PMJDY – Pradhan Mantri Jan Dhan Yojna.

H0: There is no strong association between the perception of tribes about the impact of the PMJDY scheme on financial inclusion in the case of benefits of PMJDY accounts.

At the 5% threshold of significance, the p-value given in Table 5 is .000, which is less than .05. Therefore, the null hypothesis is rejected, and hence H1 is accepted. In terms of the advantages of PMJDY accounts, there is a significant correlation between how members of various tribes view the impact of the PMJDY system on financial inclusion. All three categories share a similar understanding of the benefits of the PMJDY account. They knew very little about the advantages of the plan (Table 5).

Table 5. Chi-square Test—Result.

Source: Computed data.

Note: *Level of significance: 5%. a3 cells (20.0%) have expected count less than 5. The minimum expected count is 0.33.

Difficulties Faced with Opening and Operating of PMJDY Accounts

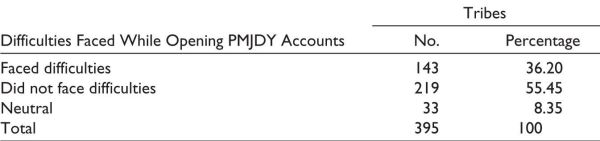

Despite the many appealing characteristics of PMJDY accounts, creating and managing accounts under this system may have presented some difficulties for account users. They might struggle to follow the process, be unable to provide the necessary documentation, experience delays or encounter bank workers who are non-cooperative, among other problems (Table 6).

Table 6. Difficulties Faced While Opening and Operating PMJDY Accounts.

Source: Primary data.

Note: PMJDY – Pradhan Mantri Jan Dhan Yojna.

H0: There is no strong association between the perception of tribes in relation to the impact of the PMJDY scheme on financial inclusion in the case of difficulties in opening and operating PMJDY accounts.

The p-value is .000, which is less than .05 at the 5% level of significance, as shown in Table 7. As a result, the null hypothesis is disproved. Consequently, it can be concluded from Table 7 that there is a significant correlation between how members of various tribes view the impact of the PMJDY scheme on financial inclusion when there are obstacles to opening and operating PMJDY accounts (Table 7).

Table 7. Chi-square Test—Result.

Source: Computed data.

Note: *Level of significance: 5%. a3 cells (20.0%) have expected count less than 5. The minimum expected count is 0.66.

Findings

The findings of this study are as follows:

Conclusion

The PMJDY addressed India’s financial exclusion issue. The primary goal of the PMJDY programme is to give the most vulnerable members of society access to formal financial services. Those living in rural areas need access to these services. This survey has been done to determine the general public’s level of scheme awareness. It also investigates the perception of account holders about the scheme by studying its utilisation and the factors affecting the scheme. The government and Reserve Bank of India can remove financial exclusion by launching this programme since it enables many people to access official financial channels. The study found that there is a correlation between how individuals from various tribes perceive the PMJDY scheme’s effect on financial inclusion. The study suggests conducting awareness programmes to enhance the awareness level of tribes on the benefits of the PMJDY scheme. With the help of Bank Mithras and Business Correspondents, the problems faced by tribes while opening and operating PMJDY accounts can be solved. The sample region was constrained by time and material restrictions, which is one of the study’s drawbacks. As with any survey-based study, there is a chance that recollection and cognitive bias crept into the results. We utilised straightforward questions with short recollection durations to lessen these biases. In order to minimise bias, the researcher personally gathered data using a systematic timetable. Furthermore, this study can be extended to more aspects of this scheme.

The study found that even for the PMJDY account holders, the full benefits of the scheme still need to be discovered. The scheme is really helpful in uplifting financial inclusion among tribes and achieving sustainable development only if the beneficiaries take full advantage of the scheme. It would be better if the government authorities and non-governmental organisations could conduct awareness programmes on the benefits and features offered under the PMJDY scheme. The basic motive behind introducing this scheme is to include the excluded people financially. But their perception has to be changed towards the scheme. The tribes are facing difficulties while opening and operating accounts under the scheme. The problems should be found out, and we should take remedial measures to resolve the hurdles. Bank Mithras and Business Correspondents can help in this regard. To sum up, it is important to prioritise outreach initiatives that are specifically created for Kerala’s scheduled tribes communities in order to raise knowledge and comprehension of the advantages offered by PMJDY. It is imperative to tailor financial literacy programmes such that they are both linguistically and culturally suitable in order to effectively reach and interact with members of scheduled tribes. Building an accessible banking infrastructure—such as mobile banking capabilities and banking correspondents—is essential to removing geographical obstacles and guaranteeing that financial services are available to everyone. Further encouraging more adoption could be the provision of incentives or favourable lending rates for scheduled tribe households that actively participate in the programme. Finally, to track progress and impact, strong monitoring and evaluation systems should be put in place. Additionally, cooperative partnerships between government agencies, financial institutions and local stakeholders should be fostered in order to co-design and implement inclusive policies that are sensitive to the particular needs of Kerala’s scheduled tribes communities.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Reshma Kurussiveettil is a Senior Research fellow under the University Grants Commission NET JRF scheme and currently receiving funds from UGC under grant number 190510464440.

ORCID iD

Reshma Kurussiveettil  https://orcid.org/0000-0002-9113-5714

https://orcid.org/0000-0002-9113-5714

Barik, R., & Sharma, P. (2019). Analyzing the progress and prospects of financial inclusion in India. Journal of Public Affairs, 19(4), e1948.

Bijoy, K. (2017). Financial Inclusion in India and PMJDY: A critical review. ICITKM, 14, 39–46.

Churchill, S. A., & Marisetty, V. B. (2020). Financial inclusion and poverty: A tale of forty-five thousand households. Applied Economics, 52(16), 1777–1788.

Joshi, M., & Rajpurohit, V. P. (2016). Pradhan Mantri Jan Dhan Yojana (the financial inclusion): A study of awareness. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2816493

Omar, M. A., & Inaba, K. (2020). Does financial inclusion reduce poverty and income inequality in developing countries? A panel data analysis. Journal of Economic Structures, 9(1), 37.

Saini, P., & Mittal, I. (2020). Pradhan Mantri Jan-dhan Yojana–A way towards financial inclusion. AGPE The Royal Gondwana Research Journal of History, Science, Economic, Political and Social Science, 2(1), 129–134.

Shibu, N. M. (2022). A study on level of awareness of Pradhan Mantri Jan Dhan Yojana among rural women. Special Education, 1(43).

Singh, A., Kumar, K., McDougal, L., Silverman, J. G., Atmavilas, Y., Gupta, R., & Raj, A. (2019). Does owning a bank account improve reproductive and maternal health services utilization and behavior in India? Evidence from the National Family Health Survey 2015–16. SSM-Population Health, 7, 100396.

Yadav, V., Singh, B. P., & Velan, N. (2021). Multidimensional Financial Inclusion Index for Indian states. Journal of Public Affairs, 21(3), e2238.