Review of Professional Management

Search

Search

1 Department of Commerce, Christ College, Irinjalakuda, Kerala, India

2 Christ College, Irinjalakuda, Kerala, India

3 Sri Ramakrishna Engineering College, Coimbatore, Tamil Nadu, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Stocks are often considered a decent hedge against inflation since they tend to move together. This research article examines the long-term relationship between inflation and stock returns in Chinese markets from 2000 to 2021. The stock price is impacted by the consequences of inflation, and this link between the two has long been a source of worry. Investors must understand how the stock market performs in connection to inflation because they anticipate equity markets to provide protection against inflationary consequences. On the relationship between inflation and stock market performance, many theoretical frameworks provide contradictory results. This research aims to pinpoint the precise impact of inflation on stock market performance. The consumer price index (CPI), which measures inflation in this research, is the independent variable, and the stock index, which measures stock market returns, is the dependent variable. The Auto Regressive Distributed Lag (ARDL) model and its accompanying Error Correction Models are used to calculate the long- and short-run correlations between Chinese stock market returns and inflation. The empirical findings indicate that there is a considerable positive long-run link between market returns and inflation. This means the price of the stock should rise along with the general prices of inflation. The relationship between inflation rate and stock market return has been examined by several financial economists around the world. However, this relationship has not been investigated widely in China.

Inflation, stock return, ARDL, ECT

Introduction

The stock markets exhibit turbulent behaviour over time. Volatility occurs when share prices rise and fall quickly. As has been observed in the past, excessive volatility hinders the efficient operation of financial markets and has a negative impact on economies. Instead of investing in riskier assets, this volatility may force investors to switch to risk-free assets. Therefore, knowledge of the stock market’s dynamic behaviour is essential for macroeconomists, financial analysts, and policymakers. Since these patterns of volatility influence their investment spending, all investors are curious about the nature of stock market behaviour. All investors are interested in understanding the nature of stock market behaviour since their investing decisions are influenced by these volatility patterns. A country’s economic activities influence stock market performance. Different variables may be more relevant in explaining variances in stock returns than a single market element.

Numerous research has been conducted on the connection between stock returns and inflation, but no conclusion has been reached. According to the Fisher model, as they reflect claims on real assets, excepted nominal asset returns should rise in lockstep with excepted inflation (1983). Adams et al. (2004) point out that the majority of empirical data indicates a negative correlation between stock returns and inflation. A negative correlation suggests that stock market returns will be below average, which will aggravate the impact of investors’ actual wealth being reduced by inflation. This negative connection is unexpected for equities since they should offset changes in inflation, according to Jacob and Mathew (1993).

Consumer spending, company investment, unemployment rate, and interest rates are all impacted by the economic phenomenon known as inflation. It might be claimed that although low inflation is associated with economic expansion, excessive inflation is risky and not only indicates an overheated economy but also can halt progress and even raise the possibility of a recession in the larger economy. The two main elements that might affect the performance of the stock market are macro and micro influences. However, owing to globalisation, national and international events, as well as, Government Policies may also affect stock market performance. The most significant macroeconomic element that may affect the performance of the stock market is inflation. The effect of inflation on the performance of the stock market may be either beneficial or negative. Every area of the economy is affected by inflation, both directly and indirectly (Geetha et al., 2011). The cost of borrowing will rise if both inflation and the nominal interest rate rise. Due to the high cost of borrowing, net profit and stock prices would decline.

Depending on monetary policy choices and the capacity of investors to hedge, inflation may have either a beneficial or negative effect on the stock markets. A rising rate of inflation lowers the future cash flow’s current value. People are able to buy fewer goods with the same amount of money when it becomes less valuable. Because investors will purchase fewer stocks with the same amount of money due to this decline in buying power, stock markets often suffer as a result. Interest rates often increase as inflation increases because the central bank will raise interest rates on loans and deposits to manage liquidity and hence control inflation. The predicted cash flows of businesses decline when loans or the cost of capital increase, which lowers stock prices. Bond prices will drop as interest rates rise, which will result in investor capital losses. Higher inflation might lead to speculative scenarios on future stock values, which increases market volatility.

In this research, we look at the connection between Chinese stock returns and price levels. The Shanghai Stock Exchange was established in 1990. Since then, China’s economy has expanded significantly, but the country’s stock market does not seem to be mirroring the expansion of its economy. In comparison to the macroeconomic fundamentals throughout the same time period, it has a tendency to swing far more drastically. China’s GDP growth rate, for instance, consistently grew from 8.3% in 2001 to 10.0% in 2004. The national economy’s gauge, the stock market, however, showed a reversal and mild decline throughout the same time period. China’s economy has grown more slowly since the global financial crisis of 2008–2009. In 2017, its GDP growth rate dropped from 14.2% in 2007 to 6.9%. The Shanghai Stock Exchange Composite Index saw a dramatic decline during this time, dropping precipitously from its historical high of about 6000 points in 2007 to around 2000 points by the end of 2008. The index later recovered to reach 3000 points in 2009 before experiencing a protracted downturn that lasted for the next five years, dropping to around 2000 points. The index began to rapidly rise in the second half of 2014. In the middle of 2015, it peaked at over 5000 points, and by the end of the year, it had dropped by 40%. The index stayed mostly within a range of 3000 to 3500 points from 2016 and 2017. In summary, the Shanghai Stock Exchange’s performance seems to depart from China’s general macroeconomic fundamentals.

Inflation has a significant effect on stock market performance. Before investing in the stock market, investors need to have a basic understanding of the relationship between stock returns and inflation. How does inflation effect stock prices, and are Chinese stocks good inflation hedges? When investors are fully educated about the connection between inflation and stock market performance, it also helps them to lower their risk. The majority of research has been done in industrialised nations, whereas emerging nations, particularly China, have found less evidence. As a result, the study’s goal is to ascertain how inflation has affected stock market performance in China during the period of 2000 to 2021. The Chinese stock markets are performing very well, and they may serve as an example of developing markets. Its emergence and growth are an unavoidable by-product of the expansion of the financial markets and market-oriented industries.

Research Problem

When the inflation rate rises, practically all product prices in the market rise simultaneously. Stock prices, however, are inversely related to inflation. In order to lessen or perhaps completely eradicate the negative impacts brought on by excessive inflation, central banks often undertake strict monetary policies, such as raising interest rates and reducing the amount of money in circulation. Stock prices will shift as a result of the policies’ effects on the demand and supply of capital in the stock market. There are now primarily two opposing perspectives on how inflation impacts the stock market. Some individuals believe that there is a positive correlation between inflation and stock returns, which implies that when inflation happens, the stock market will be bullish.

Over time, there have been several notable shifts in inflation that have affected the Chinese economy. The consumer price index (CPI) rose by 0.69% from 133.33 points in November to December 2012, but the stock market return decreased to 3.20% from 3.25% (Osoro & Ogeto, 2014). Additionally, in April 2013, the CPI rose by 0.95%, from 137.96 to 139.28, and at the same time, stock returns were impacted by changes in inflation rates and increased to 3% (Kirui et al., 2014). Additionally, owing to inflationary tendencies, the Shanghai Composite Index has been consistently increasing and dropping throughout the years. As a result, it is necessary to examine how inflation affects the stock market returns of companies listed on the Shanghai Securities Exchange. However, the bulk of Chinese studies that investigate the impact of various macroeconomic conditions on stock market performance also consider inflation. As a result, further research is needed to assess how inflation alone influences stock market returns in China.

Review of Literature

Since inflation is unavoidable, the link between stock returns and stock values is crucial for every economy. If we can develop a strong positive relationship between these two variables, we may utilise stocks as an effective hedge against inflation and maintain our real returns in the economy. Numerous scholars have looked at the connection between inflation and stock market returns, but it has remained challenging to explain the link in broad terms.

Several studies have claimed that there is a positive association between inflation and stock market gains and some of them have demonstrated using cross-sectional and time-series data and this relationship differs from country to country, particularly in light of their unique structural changes over the course of obtaining time-series data. Cross-sectional statistics make it pretty clear that market-available equities are effective inflation hedges. By ignoring the stock market as a viable inflation hedge and taking into account the different ups and downs in the economies, some academics have also shown a negative association between stock market returns and inflation. Many of them discovered both positive and negative relationships between these two factors, but they were neutral since their investigations did not provide any conclusive evidence. The goal of the current research is to fully comprehend how the two key variables—inflation and stock market returns—relate to one another.

In-depth research has been done in the literature on the connection between stock returns and inflation rates. The results of this empirical research were contradictory, nevertheless. Fisher (1930) advised that equity shares be used as a hedge against inflation after discovering a positive association between stock returns and inflation in his empirical study. For Greece from 1985 to 2000, Ioannides et al. (2002) looked at the correlation between stock market performance and inflation rates. They made the case that the stock market can protect against inflation in accordance with Fisher’s theory. Expected and unanticipated inflation has an adverse connection with stock returns, according to empirical research by Fama and Schwert (1977). They believed that an increase in development activities causes inflation to decline. Equity prices rose as a consequence of this. Omran and Pointon (2001) use co-integration analysis and ECM to assess the impact of inflation on the Egyptian stock market. The findings indicate that the inflation rate has a significant impact on the stock market.

In his empirical research carried out in China, Zhao (1999) found a substantial inverse association between inflation and the stock market. On a sample of 20 listed stocks, Bethlehem (1972) looked at the connection between inflation and stock market performance on the JSE. He came to the conclusion that equities provide excellent inflation hedges. Research by Bakshi and Chen (1996) found a link between inflation and stock prices that was negative. The association between these two factors in Greece was determined to be negative and statistically insignificant in an empirical investigation by Spyrou (2001). In 1990, Rao and Bhole looked at how inflation affected stock market performance in India. They computed nominal returns to investigate this and discovered a link between inflation and stock returns that was negative, but positive over the long term. Munyaka (2007) conducted research and discovered a clear correlation between real inflation and stock prices as well as an inverse association between predicted and actual inflation.

Alimi (2014) also looked at the long- and short-term links between inflation and the growth of the banking industry in Nigeria between 1970 and 2012. According to the research’s results, inflation had a negative impact on financial development over the studied period. Taofik and Omosola (2013) found evidence of a negative long-term connection between inflation and stock market return in Nigeria. Using monthly data on inflation and stock returns, Ahmad and Naseem (2011) investigated the effects of high inflation on stock market returns in Pakistan and discovered that there is a negative and substantial influence of inflation on stock returns.

Madsen (2004) estimated the association between share returns and inflation using Fisher’s hypothesis. The Fisher hypothesis has been refuted by the discovery in several articles that share returns are not hedged against predicted inflation. For the US markets, Gallagher and Taylor (2002) examined the relationship between stock prices and macroeconomic factors and found that inflation had a detrimental effect on stock returns. Geske and Roll (1983) examined the US stock market and discovered a negative relationship between stock price and inflation. Asprem (1989) looked at many European nations and found that stock prices were inversely correlated with inflation. Khan and Yousuf (2013) examined how several macroeconomic factors affected Bangladesh’s stock market pricing. Inflation has little long-term effect on stock values, according to research using co-integration analysis and the Vector Error Correction Model (VECM).

The literature investigation on the proposed subject has revealed a link between inflation and stock returns. There is no consensus on whether the correlation between inflation and stock returns is positive, negative, or neutral. Empirical evidence for this association in the Chinese stock market and other emerging stock markets is rare in the literature. In light of this, the relationship between stock market returns and inflation is being investigated. This is why researchers are looking into the relationship between inflation and Chinese stock market performance.

Objectives of the Study

To investigate the correlation between stock returns and inflation.

To investigate the effect of inflation on stock market returns.

Hypothesis of the Study

There is a significant link between inflation (independent variable) and stock returns (dependent variable).

Research Methodology

Data Source

Data required for the study is collected from secondary sources and the macroeconomic indicators like inflation and stock market return in China are collected from the World Economy Database 2021. The data collected for the study covers from 1991 to 2021.

Data Analysis

The current study analyses and evaluates the data using both descriptive and inferential statistics. Descriptive statistics were employed to determine the structural aspects of data. Auto Regressive Distributed Lag (ARDL) Model is used to determine the impact of inflation on stock market return in the Chinese Capital Market. The Augmented Dicky Fuller (ADF) is used to determine the stationary qualities of data. Akaike Information Criteria (AIC) were utilised for the ARDL specification with Eviews 9.

Specification of the Model

The following linear regression model has been developed to examine the putative relationship between stock return and inflation rate.

a = Constant Intercept Term of the Model

SMR = Stock Market Return (Dependent Variable)

b1 = Coefficients of the Estimated Model.

CPI = Consumer Price Index (Independent Variable)

.png) = Error Component.

= Error Component.

Descriptive Statistics

The purpose of descriptive statistics is to identify patterns, trends, and provide a relevant summary of the supplied data set. The patterns and broad trends of the dataset have been statistically summarised using descriptive statistics including mean, median, maximum and minimum values, standard deviation, and probability. According to descriptive data, the average CPI is 8.9%, although the mean value of stock market returns is 2.1%.

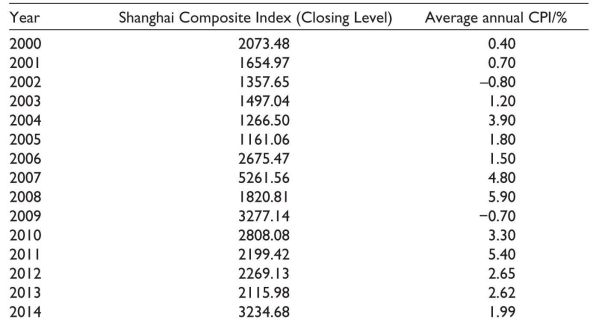

According to Table 1, both the Shanghai Composite Index and the CPI in China are increasing trend from 2000 to 2007. This indicates that there was a positive correlation between the two. The price of stocks rises when there is an increase in money supply due to enough liquidity. Companies may increase earnings thanks to lower financing costs, which also causes the price of shares to increase. Additionally, favourable financial conditions increase investor confidence, which boosts the stock market. This means that during the early stages of inflation, a rise in the money supply drives demand for shares, which raises stock prices and benefits the stock market. The expenses of living for residents and producers will, however, rise sharply in lockstep with persistently rising inflation, which will immediately lower corporate earnings and living standards.

Table 1. Descriptive Statistics Inflation and Stock Market Index of China.

Source: Globaleconomy.com.

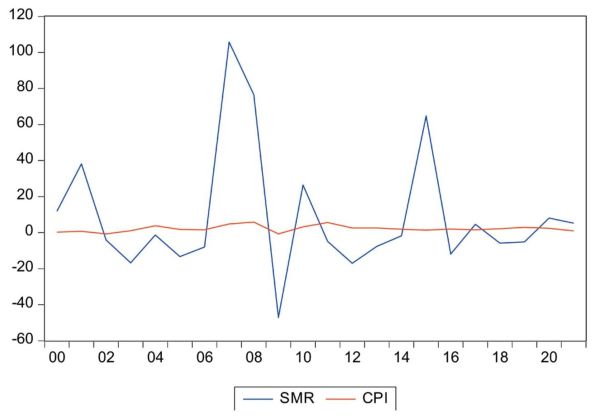

Figure 1 depicts the link between the Shanghai Composite Return of the Chinese stock market from 2000 to 2021 and the inflation rate. The CPI fluctuates somewhat between 2000 and 2002, but overall, it declines. The Shanghai index is declining rather steadily, although there has been some volatility recently. Between 2003 and 2006, the CPI increased significantly. However, the stock index remained mostly constant from 2007 to 2009; however, when the CPI increased dramatically, the Shanghai Composite Index also rose strongly, before declining. The Shanghai Composite Index then saw significant volatility.

Figure 1. Stock Market Return and Inflation in China.

Correlation Coefficient Between Inflation and Stock Market Return

A correlation matrix has been created in order to evaluate the relationship between inflation and stock index return. In China, there is a statistically significant positive (+0.47) link between the stock index and inflation (Refer Table 2).

Table 2. Correlation Coefficient of Stock Index and Inflation of China.

Unit Root Test

The stationarity characteristics of the data are typically assessed using the unit root test. The vast majority of economic data has a unit root, which leads to incorrect regression. The research checks for stationarity in time-series data using the Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) test statistics to get around this problem. As indicated in Table 3, the stock market return (SMR) is integrated at level whereas the CPI is integrated at level 1.

Table 3. ADF Unit Root Tests Results.

Impact of Inflation on Capital Market Return of China

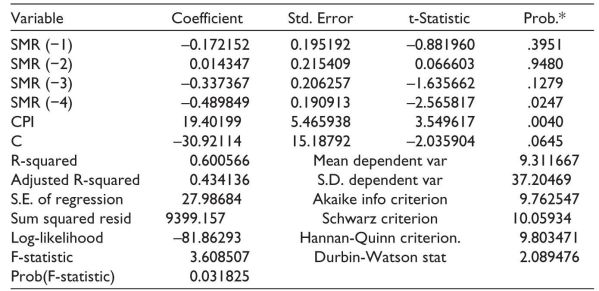

A method for concurrently assessing the short- and long-term effects of inflation on the capital market return of the Chinese market is the ARDL model. The market return is the dependent variable, while inflation is its independent variable. I (1) should be the independent variable and I (0) should be the dependent variable, or a mixed order of integration. According to Table 4, the R-square value is 60%. Accordingly, 60% of the volatility in the performance of the Chinese stock market may be attributed to inflation.

Table 4. ARDL Model for Inflation and Stock Market Return.

Note: P values and any subsequent tests do not account for model selection.

Accordingly, a linear equation model is developed in the following way:

Where t-1 represents the lagged value of the variables by one period and t-2 represents the delayed value etc. The AIC automatically calculates the optimum lag length of the model.

Optimum Lag Length Criteria

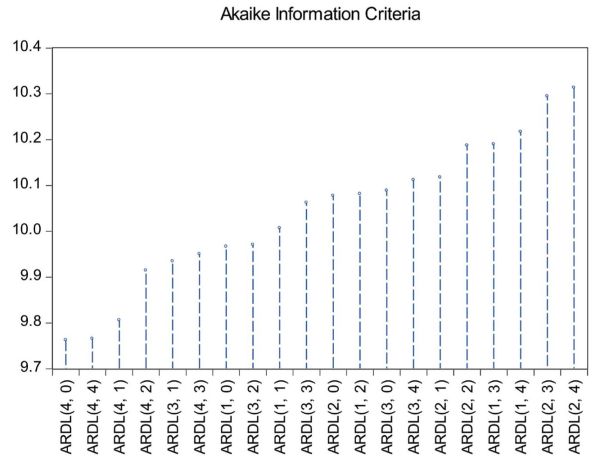

The best lag length for the model, or the number of lags employed in the model, is determined using the Akaike Information Criterion (AIC). According to this test, the model is better the lower the AIC value. The top 20 models are those with the lowest AIC values, as shown in Figure 2. The lowest AIC score indicates that ARDL is the ideal lag length (4, 0). With an AIC value of 9.75, the independent variable had a lag value of 0, whereas the dependent variable had a lag value of 4.

Figure 2. Optimum Lag Length Criteria.

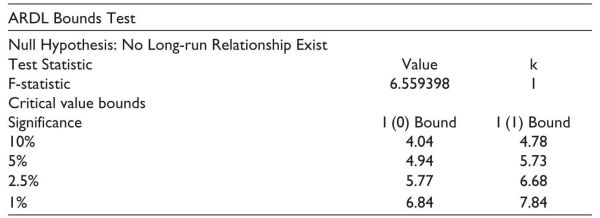

Co-integration Using the ARDL Bound Test Approach

After choosing the order of integration of each variable and the lag length, the next step is to analyse the co-integration or long-term connection among the model’s variables. The model’s variables have a cointegrating relationship if the estimated F-statistics are greater than the upper-bound critical value at the 5% level. The ARDL Bounds Test’s null hypothesis holds that there is no long-term link between the variables.

Table 5 provides a description of the bound test’s resolutions. The calculated F-statistic was 6.55, exceeding the maximum limit at the 5% level. It suggests that the variables in this model have a long-term connection. Then this research points out that the stock market return and inflation in China have a long-term link or co-integration.

Table 5. ARDL Bound Test.

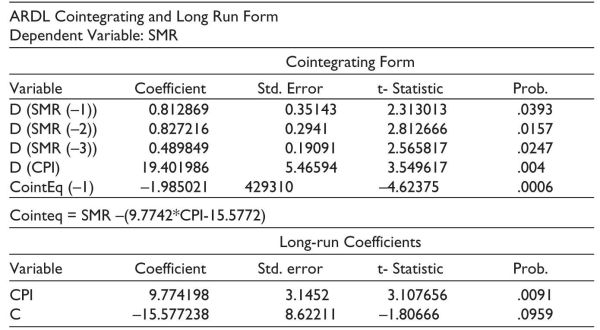

The ARDL model analyses the influence of inflation on stock market performance and examines both short- and long-term positive effects of inflation on China’s capital market performance. In order to more precisely identify and evaluate the effect of inflation on stock prices, this research introduces the Shanghai Composite Index of stock prices in place of the CPI index. The data shown in Table 6 show that stock returns and inflation have a long-term positive connection, and the Error Correction Term (ECT) is substantial and negatively signed (see Table 6). A statistically significant coefficient with a negative sign is required for the ECT coefficient, which measures how rapidly variables return to equilibrium. The yearly correction in disequilibrium is 198%, according to the ECT value of 1.98. The bound test for co-integration is supported by the exceptionally substantial ECT coefficient with anticipated signs. The study’s findings indicate a substantial positive association between inflation and stock market performance. This indicates that investors must balance risk and reward while owning equities, and it also acts as a general risk management strategy.

Table 6. ARDL Cointegrating and Long-run Form of Stock Market Return and Inflation.

Conclusion

This study gives a comprehensive understanding of the relationship between China’s stock market and inflation. The current study makes it clear how inflation affects stock market returns; as a result, it can assist market participants like traders, fund managers, financial market regulators, and investors in making wise portfolio decisions based on information about anticipated inflation and performance of stock returns in China. The main goals are to investigate the connection between inflation and stock market returns in China and to evaluate how inflation affects stock market returns. The analysis found a substantial long-term and short-term positive association between market returns and inflation, suggesting that stocks are an effective inflation hedge. These findings are comparable with those of Olufisayo (2013) and Ibrahim and Agbaje (2013), both of whom found a strong positive co-integration relationship between inflation and stock prices. These findings also suggest that China’s stock market has a long memory for inflation shocks, implying that equities constitute a reasonable long-term inflation hedge.

Recommendations for Policy and Practice

The current analysis demonstrates a significant association between inflation and stock returns; when investors anticipate that inflation will rise, equities are a better vehicle for keeping or protecting assets. At the same time, the results show that monetary policy is not neutral in the financial market. So, the government can utilise monetary policy to control the inflation rate, which will affect the actual returns on investment and real economic activity in China. Even though inflation is at a moderate level, still there is a chance to rise in the rate, which can increase the cost of living of the common people, thereby affecting the stock market, so through continuous checks on maintaining prudent monetary and fiscal policies of the country, will help to maintain the existing rate of inflation thereby does not affect adversely on the stock market and also thereby helps to increase investor confidence both locally and internationally. Since this research clearly demonstrates that changes in inflation cause movements in the stock market, economic regulators should put in place macroeconomic variable laws that are helpful for the growth of the stock market. To guarantee the success and productivity of the stock market, the regulator should ensure that market participants are abiding by the laws and regulations. During moments of rising inflation, investors should avoid panic and emotion-driven decisions in favour of fundamentally robust shares capable of weathering any economic storm.

Suggestions for Further Research

In order to determine if inflation contributes to share price volatility, the research suggests conducting a second investigation into the impact of inflation on share price volatility. However, the study was also restricted to stock market returns. The impact of inflation on the stock market returns of companies listed on Asian Securities Exchanges is another research that is recommended.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Adams, G., McQueen, G. R., & Wood, R. A. (2004). The effects of inflation news on high-frequency stock returns. The Journal of Business, 77(3), 547–574.

Ahmad, M. I., & Naseem, M. A. (2011). Does inflation hurt the stock market returns? Retrieved June 27, 2016, from https://www.researchgate.net/publication/228311038.

Alimi, R. S. (2014). Inflation and financial sector performance: The case of Nigeria. Timisoara Journal of Economics and Business, 7(1), 55–69.

Asprem, M. (1989). Stock prices, asset portfolios, and macroeconomic variables in ten European countries. Journal of Banking and Finance, 13(4–5), 589–612.

Bakshi, G. S., & Chen, Z. (1996). Inflation, asset prices, and the term structure of interest rates in monetary economies. Review of Financial Studies, 9(2), 241–275.

Bethlehem, G. (1972). An investigation of the return on ordinary shares quoted on the Johannesburg Stock Exchange with reference to hedging against inflation. South African Journal of Economics, 40(3), 254–257.

Fama, F., & Schwert, G. (1977). Asset returns and inflation. Journal of Financial Economics, 5, 115–146.

Fisher, I. (1930). The theory of interest. MacMillan.

Gallagher, L. A., & Taylor, M. P. (2002). The stock return–inflation puzzle. Google Scholar, 75, 147–156.

Geetha, C., Mohidin, R., Chandran, V. V., & Chong, V. (2011). The relationship between inflation and stock market: Evidence from Malaysia, United States, and China. International Journal of Economics, 1–16.

Geske, R., & Roll, R. (1983). The monetary and fiscal linkage between stock returns and inflation. Journal of Finance, 38(1), 1–33.

Ibrahim, T. M., & Agbaje, O. M. (2013). The relationship between stock return and inflation in Nigeria. European Scientific Journal, 9(4).

Jacob, B., & Mathew, R. (1993). Stock returns and inflation: A long-horizon perspective. The American Economic Review, 83(5), 1346–1355.

Khan, M., & Yousuf, A. (2013). Macroeconomic forces and stock prices: Evidence from the Bangladesh stock market. hdl.handle.net/10419/72453.

Kirui, E., Wawire, N. H. W., & Onono, P. O. (2014). Macroeconomic variables, volatility and stock market returns: A case of Nairobi Securities Exchange, Kenya. International Journal of Economics and Finance, 6(8), 1–17.

Ioannides, D., Katrakilides, C., & Lake, A. (2002). The relationship between stock market returns and inflation: An econometric investigation using Greek data [Paper presentation]. International Symposium on Applied Stochastic Models and Data Analysis, Brest-France, pp. 17–20.

Munyaka, P. M. (2007). The relationship between inflation and stock prices: A case study of the Nairobi Stock Exchange (Master’s thesis). University of Nairobi.

Olufisayo, A. O. (2013). Stock prices and inflation: Evidence from Nigeria. American Journal of Economics, 3(6), 260–267.

Rao, K. V. S. S., & Bhole, L. M. (1990). Inflation and equity returns. Economic & Political Weekly, 25(1), 91–96.

Spyrou, S. (2001). Stock returns and inflation: Evidence from an emerging market. Applied Economics Letters, 8(7), 447–450

Taofik, M. I., & Omosola, M. A. (2013). The relationship between stock return and inflation in Nigeria. European Scientific Journal, 9(4), 146–157.

Zhao, X.-Q. (1999). Stock prices, inflation and output: Evidence from China. Applied Economics Letters, 6(1), 509–511.