Review of Professional Management

Search

Search

Jagdeep Kaur1

1 Guru Nanak Dev University, Amritsar, Punjab, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

This study analyses various factors that affect firms’ dividend payout decisions. It investigates the impact of six firm characteristics: price-earnings ratio, firm age, firm size, growth, firm liquidity and firm leverage on dividend payout. Panel data have been obtained from 151 BSE companies for 2015–2024. A fixed-effect regression model has been used for the study. The results reveal that leverage and growth have a positive significant impact, whereas firm age has a negative significant effect on the dividend payout decisions of the firm. This study is useful for management as well as shareholders in making strategic as well as investment decisions for the firm and also provides financial dynamics regarding the appropriate dividend policy of the firm.

Dividend payout, firm age, fixed effect regression, growth, leverage

Dividend payout, firm age, fixed effect regression, growth, leverage

Introduction

A dividend is a sum of money paid to the business’s owners (Baker & Powell, 2000). Due to the increasing impact of international competition and the part that business plays in supporting the national economy, more companies are now listed on the BSE and conducting initial public offerings (IPOs). As a result, the prior investor would expect a bigger dividend return because they had already committed capital. Therefore, choices for dividend distribution must be carefully considered since they may endanger the company’s ability to develop and survive. Any unfavourable dividend policy decision would have conflicting effects. Therefore, to ensure that the business runs smoothly and that all parties are satisfied, the company needs to set up an appropriate dividend policy. This policy is expected to keep a balance between the current dividend payout and the company’s future growth, which will drive up the stock price. Each company will, therefore, have to make a unique decision regarding dividend policy, such as whether to retain or distribute its profit as dividends, the basis for which has been supported by several competing theories (Al-Kuwari, 2009). Determining the many factors influencing dividend policy is not a difficult process; nevertheless, determining how these components interact is a challenging task. While industrialised economies (such as those in Western Europe, the USA, Canada, the UK, Germany, France and Japan) have been the subject of several studies, developing economies have received relatively little attention on the subject (Musiega et al., 2013). According to Mehta (2012), there are three ways to approach the question of whether dividend policy is significant or not. According to certain authors, a rise in dividend payout will result in a rise in a company’s worth. Subsequent research suggested that dividends have an impact on the value of the company (Al-Malkawi, 2008; Amidu & Abor, 2006). However, other researchers think that raising the dividend payout level may result in a drop in the company’s worth. However, the third method, which was developed by Miller and Modigliani (MM), holds that a dividend policy is meaningless or has no bearing on a company’s worth. Dividend decisions are meaningless in a world without taxes, transaction costs or other market defects, according to MM. The outcome of these theories is not unidirectional and is perplexing. Hence, the researcher tries to find out the significant variables that affect the dividend policy of the firm.

The relationship between dividend payout and various firm characteristics has been discussed in various studies, but the nature of the interaction between them is unclear and differs from the kinds of studies that have already been done in the field. Thus, the purpose of this study is to address the observations derived from the many factors that affect the dividend payout ratio. The current study was motivated by the rapidly expanding capital market in India, the unresolved dividend policy issue and the dearth of research in the field from emerging nations. This study specifically intends to investigate the factors influencing listed firms’ dividend policies in India, a developing nation.

The structure of the article is as follows:

The remaining study has been organised as follows: the following sections consist of literature reviews of various factors of dividend policy and outline six hypotheses; the third section presents the research methodology; the fourth section is the analysis and findings; and the fifth section is the implication, limitations and suggestions for future research.

Literature Review and Hypotheses Development

It is commonly known that there are contentious issues surrounding dividend policy, the best way to maximise shareholder wealth, the proper amount of earnings to distribute as dividends, the selection of profitable projects to invest in and to reduce the agency cost, which decisions need to be made? (Aoki, 2014). Hence it is essential to understand the various essential factors that may influence strategic decisions of the firm. Payment of dividends depends upon the nature of the business. Companies comparatively in developed markets tend to pay less dividend payout. In addition, riskier and more indebted firms prefer to pay lower dividends; larger and more profitable firms and less favourable growth opportunities pay more dividends; companies with more flexible access to debt pay more dividends. Similarly, Bushra and Mirza (2015) exhibit that companies with high profits tend to pay more dividends.

As per the literature, the main factor affecting dividend payout is profitability (Al-Najjar & Kilincarslan, 2018; Bayisa, 2023; Manneh & Naser, 2015; Nasrulloh et al., 2024; Rudy et al., 2023). They study the linear relationship between profitability and dividend payout. To convey a better financial position of the company and a good, credible signal to the market, profitable firms opt to pay high dividends. In contrast, authors like Rudy et al. (2023) and Venkataraman and Venkatesan (2018) exhibit that there is an inverse relationship between them. Despite having high profits, the company wants to invest in projects, in line with Islam and Adnan (2018) and Rudy et al. (2023). On the other hand, Pandey (2001) and Malik et al. (2013) state that profitability has no impact on the dividend payout of the firm.

Now, there have been numerous research studies that considered more variables influencing dividend policy. Leverage is a significant factor of dividend payout (Al-Najjar & Kilincarslan, 2018; Awad, 2015; Kuzucu, 2015; Manneh & Naser, 2015). As per the study of Awad (2015), leverage positively affects the dividend payout of KSE-listed companies. In contrast, Al-Malkawi (2008) and Rudy et al. (2023) state that there is a negative relationship between them. According to Rozeff (1982), a firm’s transaction cost and risk will rise as its leverage increases. The leverage ratio shows how much debt a corporation has. A high leverage ratio necessitates a high fixed payment to the lenders in the form of interest for external funding. This implies that the likelihood of paying out a dividend will decrease as leverage increases. This suggests that leverage and dividend policy have an inverse relationship (Abdullah et al., 2018). Some authors like Chukwuebuka et al. (2020) investigate no significant impact of leverage on the dividend payout of the firm

Furthermore, as per the opinion of Birhanu et al. (2023), firm age has a significant positive impact on dividend payout; more aged and mature firms always prefer high dividends. As the firm had already matured and did not have any further investment opportunities, they decided not to retain the profit (Birhanu et al., 2023). In contrast, studies like Al-Malkawi (2008) and Bushra and Mirza (2015) state that companies that are looking to find new investment possibilities or are facing a shift in the firm’s life cycle (the growth phase) prefer to pay lower or no dividends during the mature period.

The price-earnings (PE) ratio has a significant impact on dividend policy. As per the opinion of Moradi et al. (2010) and Ang and Peterson (1984), it is inversely related to dividend payout. Since these companies typically retain their earnings to fund future growth, a company with a high PE ratio would be thought to be growing faster than one with a low PE ratio. On the other hand, Baker and Powell (2000) and Kuzucu (2015) state a positive relationship. The price-to-book (PB) ratio shows how much the company is worth in the market compared to its book value. A firm’s likelihood of paying out increases with its PB ratio. When investors place a comparatively high stock price on dividend-paying companies, those companies raise their payouts, and vice versa. On the other hand, Malkawi (2008) states that there is no significant association between them.

It is believed that growth plays a major role in determining dividend policy (Barclay et al., 1995; Fama & French, 2001). According to the research, a company’s need for capital for growth prospects usually has a major detrimental effect on dividend payout. As a corporation matures, its growth slows down. This leads to lower capital expenditure and the potential for higher dividend payments because the company will have more free cash flow. Companies need to accumulate reserves to handle rapid expansion and financing requirements, which means they will have to pay fewer dividends and retain more profit. A company with a strong investment potential will be expected to pay a low dividend (Al-Malkawi, 2008). Conversely, a business with little growth opportunity may choose to issue a dividend, which could restrict the overviewing management approach (Jensen et al., 1992). However, according to Lin et al. (2012), despite having the potential to generate large returns, a company may choose to pay a large dividend to foster goodwill and protect minority shareholders, which is in line with Arif and Akbarshah (2013).

Firm size is a significant factor influencing corporate dividend decisions, and numerous studies have shown a positive correlation between firm size and dividend policy (Al-Najjar & Kilincarslan, 2018; Barclay et al., 1995; Fama & French, 2001). The majority of larger companies pay higher dividends to investors to establish their financial stability in the market (Arif & Akbarshah, 2013). Conversely, other writers argue that larger companies are more likely to retain cash flow rather than pay dividends, and smaller companies require less cash flow than larger companies do because they require less money to run their daily operations (Bushra & Mirza, 2015).

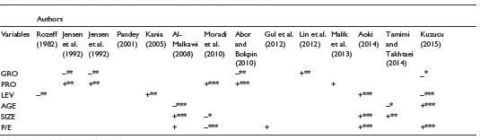

Significant outcomes of various determinants of dividend payout in various studies have been shown in Table 1. While several research studies have looked at the determinants influencing dividend policy in India, the data utilised in these studies were not current, and the published findings were inconsistent (Kumar, 2006; Movalia & Vekariya, 2014). Furthermore, the few previous studies on Indian corporations’ dividend policies had a sector-specific focus. Anil and Kapoor’s (2008) study, for example, focused mostly on consumer product firms. With the use of more recent data and a wider scope that includes all sectors, the current study expands on the body of research on the factors influencing corporate dividend policy from developing economies, such as India.The following null hypotheses were developed to determine the factors influencing the dividend policy of BSE 200 listed companies in India.

Table 1. Evidence of Various Determinants of Dividend Payout.

Source: Author’s compilation.

Notes: *** significant at 1%, ** significant at 5% and *significant at 10%.

Ho1: There is no significant effect of profitability on dividend payout.

Ho2: There is no significant effect of leverage on dividend payout.

Ho3: There is no significant effect of firm age on dividend payout.

Ho4: There is no significant effect of PE ratio on dividend payout.

Ho5: There is no significant effect of growth on dividend payout.

Ho6: There is no significant effect of firm size on dividend payout.

Research Methodology

Universe of the Study

The study’s goal is to present a comprehensive analysis of the factors influencing dividend policy. The companies chosen for this study are those that are included in the top 200 firms listed on BSE based on market capitalisation as of 12 October 2021 (consistent with the study of Yusof & Ismail, 2016 and Abdullah et al., 2018). Because high market capitalised companies are financially sound and have stable earnings and high dividend payout. The study includes all the companies except the following:

Hence, 151 companies were included in this study.

.jpg/10_1177_09728686251339944-table(2)__480x169.jpg)

Data Collection

Data for the period 2015–2024 have been gathered from the software ACE Equity and the annual reports of the companies. The sample size of 10 years has been taken for a balanced, comprehensive and empirically relevant data set for analysing dividend payout. Such a long-framed period can predict the economic fluctuations during the study period of assessing dividend payouts.

Statistical Tool

Software called Gretl has been used to analyse the data. Regression analysis was specifically performed using the pooled least squares model, fixed- and random-effects models. Panel regression has been applied by the researcher. Panel data analysis, as noted by Hsiao (2022), has certain advantages since it takes into account the influence of other measurable factors on the determination of the dependent variable in addition to the function of unobservable firm-specific and time-specific elements. We have utilised panel data analysis because of its benefit over cross-sectional analysis.

Model

The dividend payout is the dependent variable in the model, and the independent variables are firm size, PE ratio, profitability, growth, firm age and leverage of the company.

Model specifications: For testing the hypotheses, the research model is presented as follows:

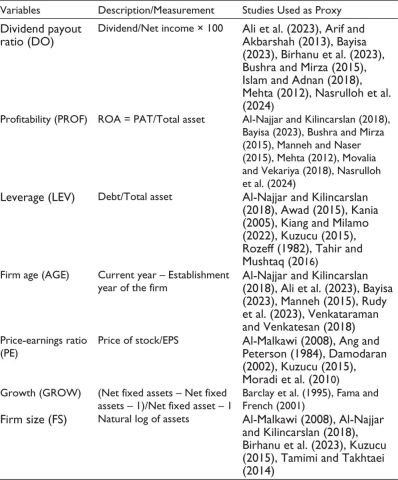

Definition of Variables

where, DO = Dividend payout, PROF = Profitability, LEV = Leverage, AGE = Firm age, PE = Price-earnings ratio, GROW = Growth and FS = Firm Size.

Analysis and Findings

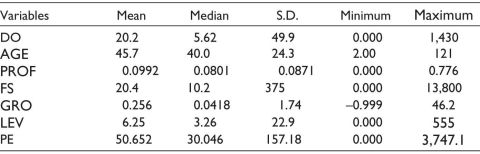

Descriptive Statistics

In this section, Table 2 depicts the mean, median, standard deviation, minimum and maximum value of each variable used in this study.

Table 2. Descriptive Statistics of Determinants of Dividend Payout.

Source: Author’s compilation.

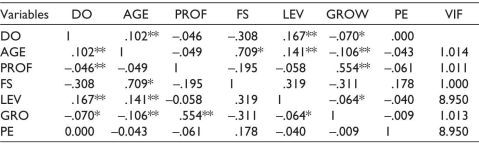

Table 3. Correlation Analysis (Total Observations = 1,347).

Source: Author’s compilation.

Notes: *Correlation is significant at the 0.05 level (two-tailed).

**Correlation is significant at the 0.01 level (two-tailed).

The table illustrates the mean DO (20.02%) indicates that BSE companies in our sample paid dividends in about 20.02% of the total observations Additionally, the means of PROF and LEV show that companies had returns of roughly 0.099% on their total assets invested during the time, and made about 6.25% of their capital structures from debt financing. On average, BSE firms had a good signal of growth of approximately 25.6%. Furthermore, the mean value of firm age and firm size is 45.7 and 20.4, respectively.

Correlation Analysis

The degree of association between two variables can be examined with the use of the statistical method known as correlation analysis; they discovered that the correlation between the variables should not be greater than .80, which may suggest the existence of multicollinearity. Additionally, the variance-inflated factor, or VIF, can be used to test for multicollinearity. If the value of each variable is less than 10, multicollinearity is not present (Gujarati, 2021). However, in our investigation, Table 3 indicates that the correlation coefficient between a dependent variable and independent variables is less than .80, and all variable values are less than 10. Hence, there is no problem of multicollinearity.

Diagnostics Tests

Autocorrelation

The optimal mix of explanatory factors and the existence of autocorrelation in the residuals (prediction errors) are found using Durbin–Watson (DW) statistics (Gujarati, 2021). The data do not exhibit autocorrelation, as indicated by the calculated DW value of 2.080282.

Heteroskedasticity

Heteroskedasticity can be managed during model execution by utilising a robust standard error (Gujarati, 2021).

Hausman Test to Select the Appropriate Model

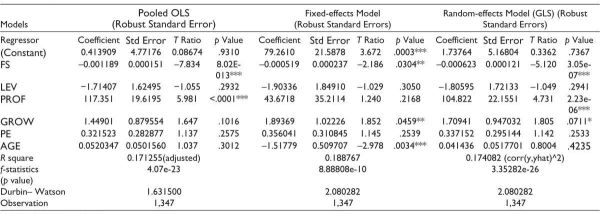

Table 4 displays the findings of the regression analysis of the pooled ordinary least squares, random-effects, and fixed-effects models on the variables influencing dividend policy. According to the Hausman test, the fixed-effects model is more suitable than the random and pooled methods for this investigation.

Similarly, Table 4 demonstrates that the six factors considered in this study explain almost 18.87% of the factors affecting dividend policy. The regression results indicate that there is no statistically significant association between the dividend payout and profitability (p value = .2168). Therefore, our first null hypothesis is not rejected. This demonstrates that dividend policy is not much influenced by profitability. The outcomes here agree with those of Mehta (2012), Pandey (2001) and Malik et al. (2013).

Leverage has a negative but insignificant relationship with dividend payout, in line with Gill et al. (2010) and Al-Kuwari (2009). It is because the p value of .3050 is not less than 5%. Hence, our null hypothesis is not rejected.

Firm age was shown to have a statistically significant negative association with the dividend payout value (p value = .0034). Thus, the hypothesis was disproved. This suggests that in Indian corporations, a firm’s age has a major role in determining its dividend policy. According to this theory, companies prefer to pay fewer or no dividends during the maturity period because they may be facing a shift in the firm’s life cycle (the growth phase) and seeking to identify new investment opportunities (Al-Malkawi, 2008; Bushra & Mirza, 2015).

With a p value of .2539, Table 4 demonstrates that the coefficient of the PE ratio is statistically insignificant. It is not decided to reject the third null hypothesis. This implies that the company’s dividend policy is not significantly influenced by its PE ratio. This discovery aligns with the findings of Gul et al. (2012) and Al-Malkawi (2008).

Table 4. Regression Results for Determinants of Dividend Payout.

Source: Author’s compilation.

Note: ***, **and * represent significance levels at 1%, 5% and 10%, respectively.

With a p value of .0459 and a threshold of significance of 5%, the regression demonstrates a strong positive link between dividend policy and growth. Even if a company has a phase of growth, Lin et al. (2012) state that it may opt to give greater dividends to foster goodwill and help minority shareholders. This finding is consistent with Lin et al. (2012). It is determined that high-growth companies choose to pay large dividends to draw in both current and new investors and to win over shareholders, which helps the companies lower the agency problem (Easterbrook, 1984).

A statistically significant negative link between firm size and value is observed, as demonstrated in Table 4, with a p value of .0304. Firm size is a significant factor; hence, the null hypothesis is rejected. This result is in line with the findings of Moradi et al. (2010).

Implication, Limitations and Suggestions

This study looked at several variables influencing the dividend policy of Indian companies using data from 151 BSE companies between 2015 and 2024. The findings indicate that firm price earning, leverage and profitability were not significant factors, but firm age, size and growth are some of the key determinants of dividend policy. The results led to six hypotheses regarding the determinants influencing dividend policy. From these, we deduced that firm age and size had a negative relationship with the dividend policy. In contrast, growth and the dividend policy of the company are positively correlated. The results of this study also help current and potential shareholders make investment decisions. It also provides the board of directors with valuable input for the formulation and revision of dividend policy. In particular, the consideration of profit, leverage, size, growth and PE ratio should be carefully considered if the board of directors is thinking about raising the dividend payment to shareholders.

By looking at the factors that influence dividend policy for BSE companies, the research contributes to the body of knowledge by illuminating the trends seen in this type of financing decision for businesses in developing markets. The empirical results of this study provide valuable insights into the various factors of dividend payout of listed firms in India, a developing nation, and hence contribute significantly to the body of literature. The success of the company will be affected in the long run by the integration of good determinants into their cultures. It implies that to attract international investment and grow through cross-border commerce and acquisitions, developing economies are required.

While aligning with the financial stability of the company, one can make a structure of dividend policy by understanding the impact of leverage, profitability, growth, size and so on, and for promoting investors’ confidence, regulators and policymakers can also develop strategies for creating balanced dividend policies. Companies, investors and regulators can make properly informed financial decisions owing to the practical implications of these determinants. Variability in dividend policy by sector and nation can be evaluated in further detail.

The determinants of dividend policy have only been examined in this study using six independent variables. To better understand the effects of these variables, future studies should try to include more relevant determinants such as tax, market-to-book ratio, asset tangibility, insider ownership, block ownership and corporate governance features. Additionally, this could be researched through banks or NSE firms. For better outcomes, certain useful behavioural and psychological elements could be taken into account. The study is based on secondary data based on quantitative data, where chances of mistakes may occur; hence, qualitative techniques like an interview and questionnaire could be used for better results. Despite some limitations, the study contributes to the knowledge of existing literature about the significant issues of various determinants of dividend payout.

Acknowledgements

The author wants to sincerely thank Sage Publications for all of their help and assistance during the research process. Additionally, the author appreciates the anonymous referees for the journal for their tremendously valuable comments on how to improve the article’s quality.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Jagdeep Kaur https://orcid.org/0009-0003-3300-2571

Abdullah, M. N., Quader, S. M., & Saha, J. (2018). Impact of payout policy on market value. International Review of Business Research Papers, 14(1), 109–131.

Abor, J., & Bokpin, G. A. (2010). Investment opportunities, corporate finance, and dividend payout policy: Evidence from emerging markets. Studies in Economics and Finance, 27(3), 180–194.

Ali, A., Khan, A., & Khan, S. (2023). Dividend policy attributes and its impact on firm profitability. Sarhad Journal of Management Sciences, 9(1).

Al-Kuwari, D. (2009). Determinants of the dividend policy of companies listed on emerging stock exchanges: The case of the Gulf Cooperation Council (GCC) countries. Global Economy & Finance Journal, 2(2), 38–63.

Al-Malkawi, H. A. N. (2008). Factors influencing corporate dividend decision: Evidence from Jordanian panel data. International Journal of Business, 13(2).

Al-Najjar, B., & Kilincarslan, E. (2018). Revisiting firm-specific determinants of dividend policy: Evidence from Turkey. Economic Issues, 23(1), 3–34.

Amidu, M., & Abor, J. (2006). Determinants of dividend payout ratios in Ghana. The Journal of Risk Finance, 7(2), 136–145.

Ang, J., & Peterson, P. P. (1984). The leasing puzzle. The Journal of Finance, 39(4), 1055–1065.

Anil, K., & Kapoor, S. (2008). Determinants of dividend payout ratios: A study of Indian information technology sector. International Research Journal of Finance and Economics, 15, 63–71.

Aoki, Y. (2014). How does the largest shareholder affect dividends? International Review of Finance, 14(4), 613–645.

Arif, A., & Akbarshah, F. (2013). Determinants of dividend policy: A sectoral analysis from Pakistan. International Journal of Business and Behavioral Sciences, 3(9), 16–33.

Awad, B. (2015). Determinants of dividend policy in Kuwait stock exchange. International Journal of Business and Management Review, 3(7), 72–78.

Baker, H. K., & Powell, G. E. (2000). Determinants of corporate dividend policy: A survey of NYSE firms. Financial Practice and Education, 10, 29–40.

Barclay, M. J., Smith, C. W., & Watts, R. L. (1995). The determinants of corporate leverage and dividend policies. Journal of Applied Corporate Finance, 7(4), 4–19.

Bayisa, Y. (2023). Determinants of dividend payout in private insurance companies of Ethiopia. International Journal of Advanced Research in Science and Technology, 12(8), 1064–1070.

Birhanu, D. C., Gelaye, Z. E., & Gelalcha, W. G. (2023). Determinants of dividend payout ratio of private insurance companies in Ethiopia. Journal of Research in Engineering and Computer Sciences, 2(1), 1–13.

Bushra, A., & Mirza, N. (2015). The determinants of corporate dividend policy in Pakistan. The Lahore Journal of Economics, 20(2), 77.

Chukwuebuka, O., & Okonkwo, O. (2020). Financial leverage and dividend policy: Evidence from oil and gas firms in Nigeria. Asian Journal of Economics, Business and Accounting, 14(2), 51–62.

Damodaran, A. (2002). Tools and techniques for determining the value of any asset. John Wiley & Sons.

Easterbrook, F. H. (1984). Two agency-cost explanations of dividends. The American Economic Review, 74(4), 650–659.

Fama, E. F., & French, K. R. (2001). Disappearing dividends: Changing firm characteristics or lower propensity to pay? Journal of Financial Economics, 60(1), 3–43.

Gill, A., Biger, N., & Tibrewala, R. (2010). Determinants of dividend payout ratios: Evidence from United States. The Open Business Journal, 3(9), 8–14.

Gujarati, D. N. (2021). Essentials of econometrics. Sage Publications.

Gul, S., Sajid, M., Razzaq, N., Iqbal, M. F., & Khan, M. B. (2012). The relationship between dividend policy and shareholder’s wealth. Economics and Finance Review, 2(2), 55–59.

Hsiao, C. (2022). Analysis of panel data (No. 64). Cambridge University Press.

Islam, M. S., & Adnan, A. T. M. (2018). Factors influencing dividend policy in Bangladesh: Survey evidence from listed manufacturing companies in Dhaka stock exchange. European Journal of Business Science and Technology, 4(2), 156–173.

Jensen, G. R., Solberg, D. P., & Zorn, T. S. (1992). Simultaneous determination of insider ownership, debt, and dividend policies. Journal of Financial and Quantitative Analysis, 27(2), 247–263.

Kania, S. L. (2005). What factors motivate the corporate dividend decision? Theses, Dissertations & Honors Papers, 195.

Kiangi, R. F., & Milamo, M. W. R. J. (2022). Dividend policy for commercial banks in Tanzania: Controlling for random and specific effects. Research Journal of Finance and Accounting, 13(4).

Kumar, J. (2006). Corporate governance and dividends payout in India. Journal of Emerging Market Finance, 5(1), 15–58.

Kuzucu, N. (2015). Determinants of dividend policy: A panel data analysis for Turkish listed firms. International Journal of Business and Management, 10(11).

Lin, H., Lin, W. Y., & Liu, Y. C. A. (2012). Dividend catering and the information content of dividend changes. Journal of Interdisciplinary Mathematics, 15(1), 1–21.

Malik, F., Gul, S., Khan, M. T., Rehman, S. U., & Khan, M. (2013). Factors influencing corporate dividend payout decisions of financial and non-financial firms. Research Journal of Finance and Accounting, 4(1), 35–46.

Manneh, M. A., & Naser, K. (2015). Determinants of corporate dividends policy: Evidence from an emerging economy. International Journal of Economics and Finance, 7(7), 229–239.

Mazengo, S. D., & Mwaifyusi, H. A. (2021). The effect of liquidity, profitability, and company size on dividend payout: Evidence from financial institutions listed in Dar es Salaam stock exchange. Business Education Journal, 7(1).

Mehta, A. (2012). An empirical analysis of determinants of dividend policy: Evidence from the UAE companies. Global Review of Accounting and Finance, 3(1), 18–31.

Moradi, M., Salehi, M., & Honarmand, S. (2010). Factors affecting dividend policy: Empirical evidence of Iran. Poslovna izvrsnost, 4(1), 45–61.

Movalia, N., & Vekariya, P. (2014). A study on determinant of dividend policy and its impact on dividend of listed company under S&P BSE Sensex. Journal of Business Management & Social Sciences Research, 3(12), 70–72.

Musiega, M. G., Alala, O. B., Musiega, D., Maokomba, C. O., & Egessa, R. (2013). Determinants of dividend payout policy among non-financial firms on Nairobi Securities Exchange, Kenya. International Journal of Scientific & Technology Research, 2(10), 253–266.

Nasrulloh, N., Supraptiningsih, J. D., & Alvianingsih, V. (2024). The effect of profitability (ROA) and free cash flow on dividend payout ratio in manufacturing companies listed on the IDX in 2019-2022. JISIP (Jurnal Ilmu Sosial dan Pendidikan), 8(2), 1016–1025.

Pandey, I. M. (2001). Corporate dividend policy and behaviour: The Malaysian experience (IIMA Working Papers WP2001-11-01).

Rozeff, M. S. (1982). Growth, beta and agency costs as determinants of dividend payout ratios. Journal of Financial Research, 5(3), 249–259.

Rudy, R. P., Hady, H., & Nalurita, F. (2023). Factors influencing dividend payout in manufacturing industries listed on the Indonesia Stock Exchange, Riwayat. Educational Journal of History and Humanities, 6(4), 3002–3018.

Tahir, M., & Mushtaq, M. (2016). Determinants of dividend payout: Evidence from listed oil and gas companies of Pakistan. The Journal of Asian Finance, Economics and Business, 3(4), 25–37.

Tamimi, M., & Takhtaei, N. (2014). Relationship between firm age and financial leverage with dividend policy. Asian Journal of Finance & Accounting, 6(2), 53.

Venkataraman, R., & Venkatesan, T. (2018). Empirical analysis of the determinants of dividend payouts of Indian banking stocks using panel data econometrics. In Advances in finance & applied economics (pp. 283–297). Springer.

Yusof, Y., & Ismail, S. (2016). Determinants of dividend policy of public listed companies in Malaysia. Review of International Business and Strategy, 26(1), 88–99.