Review of Professional Management

Search

Search

Shivani Nischal1

1 University School of Financial Studies, Guru Nanak Dev University, Amritsar, Punjab, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

In today’s context, digital transformation is essential for the survival of an economy. The digital transformation mechanism involves the understanding of the potential of technology and creating a new road map that details the solutions and resources needed to deliver change. Digitalisation happens when organisations embed digital technologies across all their operations. The purpose of this study involves the verification of whether the digital transformation mechanism could improve organisational performance. Under current research analysis, the effect of digitalisation strategies such as various structural changes, use of digital technologies and value creation upon the short- and long-run financial performance of Indian banks has been examined. For the same, employees of 20 public and private sector banks have been selected through a stratified random sampling technique. First, the effect of digital transformation on the banking industry’s financial performance has been analysed, and then, the role of cognitive conflict, that is, employees’ mental health or cognitive dissonance as a moderator, has been investigated. The findings revealed that the adoption of digital technologies can significantly affect the financial performance of a business enterprise. In the banking industry, the adoption of digitalisation has a positive relationship with the short-run and long-run financial performance, which is moderated by the psychological state of human personnel, that is, cognitive conflicting state.

Cognitive dissonance, digital transformation mechanism, financial performance indicators, structural changes, value creation

Introduction

The survival of an economy without digital transformation is absolutely impossible. The digital transformation mechanism involves the process of implementation of new advanced techniques of information technologies that lead towards the adoption of new and unique business models in today’s competitive world. On the one hand, digital transformations of companies include the understanding of the potential of technology and creating a new road map that details the solutions and resources needed to deliver change. On the other hand, digitalisation happens when the organisations embed digital technologies across all their operations (Fichman et al., 2014; Hess et al., 2016; Lucas et al., 2013). Digital transformation is not an easy process, because its implementation passes through complex procedures (Hess et al. 2016). Business organisations are completely upgrading themselves through product improvements, research and developments, innovations, cost reductions and high sales strategies to capture the main market share (Sebastian et al., 2017). Faro et al. (2019) also highlighted the challenge for public sector organisations to preserve their validity by digitally transforming their products and processes so as to remain viable business units. Historically, they are reluctant to bring about new changes to adopt. Complex and core issues have emerged in the preparation and execution of digital transformation mechanisms in that business concerns. Digital transformation has been regarded as a continuous seed which generates roots of further developments in today’s modern world with no foreseeable end (Chanias et al., 2019). Strategic management decisions of the business enterprises are now to be majorly focused on digital transformation mechanisms instead of any other technical issue. Digital transformations and innovations are now to be treated as hard-core intensive elements of public and private sector entities (Henriette et al., 2015; Reis et al., 2018).

A SAP 2019 survey revealed that only 3% of business entities have adopted the complete mechanism of a digital transformation system, and 84% entities found this mechanism very important for their survival in the next five years (Besson & Rowe, 2012; Crowston et al., 2005). Kane et al. (2015) suggested that the scope of the digital transformation mechanism incorporates the process of adopting advanced information technologies that incorporate new and unique business models in today’s competitive world. The fusion view with regard to digital transformation (Bharadwaj et al., 2013; Mithas et al., 2013) revealed that the strategic impact of information technology was very imperative because a corporate IT mechanism has been found identical to a business mechanism. In fact the current scenarios indicate that the practical knowledge of new information technology and digital transformation fails the implementation of innovative digital transformation in business concerns (Hess et al., 2016; Matt et al., 2015). On the other hand, cognitive conflict is a psychological state which occurs when there is a discrepancy between a person’s cognitive structures and their experiences. Cognitive conflict also refers to how people interpret or prioritise information, which can make it difficult to make decisions. In strategy of practice theory (Jarzabkowski, 2005; Jarzabkowski & Spee, 2009; Whittington, 1996, 2006), digital transformation has been related to the emotional stagnancy of human personnel inside the business world. Without achieving the stability of cognitive dissonance and conflict resolution and establishment of full coordination and support system, the implementation of the digital transformation mechanism is neither effective nor productive (Jarzabkowski, 2005; Jarzabkowski & Spee, 2009; Whittington, 1996, 2006). Aspara also highlighted that the decision for implementing digital transformation strategy is very complex and incorporates the involvement of cautious strategic judgements. To simplify the process of decision-making, the concept of psychology should be taken into consideration, that is, elements associated with emotions and cognitive dissonance (Luce et al., 1999; Nguyen et al., 2018). While focusing on factors generating dissonance or disagreements, this study analyses the effect of the adoption of digital transformation on the performance of study units. The moderated effect of cognitive conflict has been undertaken in the proposed theoretical model. Amason (1996) outlined the conflict as the crux of this paradox and provided strong evidence from two different samples of conflict’s constant yet contradictory impacts upon decision quality, consensus as well as upon affective acceptance. The collection of the first sample included 94 CEOs from 48 top management teams from the small food processing firms of America. The second sample included 15 managers from five furniture manufacturing firms in the Southeastern United States. The study builds the relationship between digital transformation mechanism and cognitive conflict theory. Cognitive conflict has been found positively related to decision quality, understanding, commitment and affective acceptance, and the cognitive conflict leads to achievement of business productivity (Amason, 1996; Festinger, 1957; Warner & Wäger, 2019). Parayitam and Dooley (2011) examined the relationship between cognitive conflict, decision quality and decision commitment. The data were collected from the top management teams of 109 hospitals of the United States. The findings of the study revealed that a curvilinear or inverted U-shaped relationship exists between cognitive conflict and decision-making quality variables. The study emphasised that top management team members need not over emphasise cognitive conflict beyond a limit because it may have destructive effects. The findings of the study revealed the presence of a moderated level of cognitive conflict which is desirable always instead of too much conflict, causing destruction in the business units (Bercovitch, 1982; Parayitam & Dooley, 2011). Various longitudinal studies have examined the relationship between task, process and relationship conflict, inter-personal conflict and inter-group conflict and work performance (Greer et al., 2008), but the impact of digitally transformed strategies on the financial performance of banking industry has been least explored while mediating the role of cognitive conflict. This study focuses on this research gap.

This study expands the literature by indicating the effect of digital transformation mechanisms on banks’ operational efficiency and the industry and society as a whole. The study focuses on the effect of digital transformation on short- and long-term performance, widening and deepening the current research. Further, the research confirmed the moderating effect of cognitive conflict on the relationship between digital transformation and the overall performance of the banking sector. Moreover, the bank unit’s age, unit size, sector and past performance have been taken as control variables to improve the reliability of the conclusion.

Theoretical Framework and Hypothesis Development

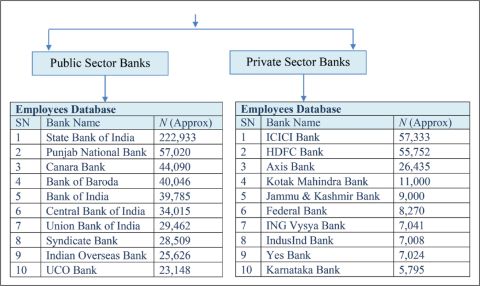

The primary objective of this research is to explore the connection between digital transformation mechanisms and the financial performance of the banking industry units of India. Further, the mediated role of conflicts has been explored to stimulate the low financial performance that turns into the high financial performance of the banking business in India. For this purpose, a single cross-sectional research design has been undertaken, that is, only one sample of respondents is drawn from the target population, and data is obtained from this sample only once. The population of Punjab has been divided geographically into three major belts, that is, Majha, Doaba and Malwa. One city has been selected from each belt on the basis of the highest area population criterion to make the sample representative based on this geographical cut-off criteria. Area population has been considered a major determinant and a significant positive contributor towards the set up of the number and size of bank branches (Avery et al., 1999; Cristina, 2014; Damar, 2007; Hannan & Hanweck, 2007). Therefore, the selected areas have been found enriched with the highest number of offices of all scheduled commercial banks, that is, Amritsar (478), Jalandhar (669) and Ludhiana (783) within each belt of Punjab, that is, Majha, Doaba and Malwa. Thereafter, the sample database was selected from various published annual reports of banks that have been specified as the highest employee-bearing units (Avery et al., 1999; Cristina, 2014; Damar, 2007; Hannan & Hanweck, 2007). Twenty banks have been selected (mentioned in Table 1). The stratified random sampling mechanism involved a survey of 90 branches of public sector banks and 79 branches of private sector banks to get a response of 676 bank employees. Table 1 indicates the number of respondents and branches surveyed of every public and private sector bank. Sixty-six respondents did not return the questionnaire due to their busy schedule, and 69 questionnaires had been discarded due to data redundancy error. Finally, 541 responses have been recorded for data analysis (Krejcie & Morgan, 1970).

The formula for calculating sample size (the Krejcie–Morgan criterion) is

The stratification process started with the selection of these commercial banks situated in Amritsar, Jalandhar and Ludhiana cities of Punjab. Ten banks from the public sector and ten banks from the private sector have been selected based on the highest employee database extracted from annual reports out of Prowess software. The population of Punjab has been divided geographically into three major belts, that is, Majha, Doaba and Malwa. One city has been selected based on the highest area population criterion from each belt to make the sample representative based on this geographical cut-off criteria. Therefore, the selected areas have been found enriched with the highest number of offices of all scheduled commercial banks, that is, Amritsar (478), Jalandhar (669) and Ludhiana (783) within each belt of Punjab, that is, Majha, Doaba and Malwa.

Table 1. Sample Database: Details of Banking Units.

Source: Data have been captured from the official websites of these units and representing figures under parenthesis depicts the number of branches surveyed under the geographical area of each city.

Note: ASR: Amritsar, JLD: Jalandhar, LUD: Ludhiana (famous green belt-cities of Punjab).

Figure 1. Public and Private Sector Banks under Study.

Source: Annual reports of public and private sector banks extracted from Prowess software.

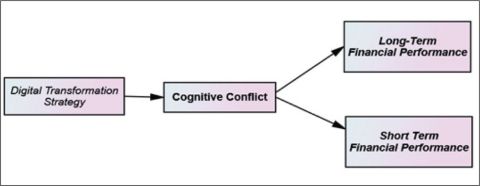

Further, having specific control over cognitive conflict dissonance will automatically lead to better work performance and productivity because of for-sure improved decision quality and the digital transformed strategy mechanism. As per strategy-as-practice theory, this research framework conjuncts the various theories of digital transformation and conflict management mechanisms. The proposed research question under the present analysis focused on whether the organisational financial performance can be improved by the implementation of digital transformation in banking units or not. After that, the research further stressed the moderation by the cognitive conflict between digital transformation and the financial performance of banking units.

The proposed theoretical model of the study has been depicted in Figure 2. No economy in the present era can really prevent the occurrence of competitive mutilation that is brought about by upgrading digitalisation processes and business models (Al-Debei & Avison 2010). The impact of the digital transformation mechanism on the units’ financial performance should be examined (Vial, 2019). The role of cognitive or task-related conflict cannot be ignored. In strategy- as-practice model theory, strategic decisions have been linked with humans’ involvement or their mental cognitive ability to reach targeted goals. Moderated cognitive conflict with greater adoption of digital transformation mechanism will assuredly lead to better work productivity and the firm will reach its heights (Amason, 1996; Chanias et al., 2019).

Figure 2. Theoretical Model of the Study.

On the basis of research questions and the proposed model, the following hypotheses have been formulated:

Ha: Digital transformation mechanism has been positively influencing the short-term financial performance of banking units under study.

Hb: Digital transformation mechanism has been positively influencing the long-term financial performance of banking units under study.

Hc: Digital transformation mechanism is positively influencing the cognitive conflict prevailing within banking units under study.

Hd: Cognitive conflict has been positively influencing the short-term financial performance of banking units under study.

He: Cognitive conflict has been positively influencing the long-term financial performance of banking units under study.

Hf: There is an inverted U-shaped relationship curve of cognitive conflict between the digital transformation mechanism and the short-term banking units’ financial performance.

Hg: There is an inverted U-shaped relationship curve of cognitive conflict between the digital transformation mechanism and the long-term banking units’ financial performance.

Application of Standardised Measures

Data have been collected with the help of a set standard questionnaire. The digital transformation mechanism has been examined with the help of a standardised scale which is developed by Hess et al. (2016), which incorporates 11 items of strategic decision questions. For example, ‘The firm actively looks for opportunities for implementation of new technologies’. Three dimensions have been bifurcated, that is, strategic questions about technology, changes in value creation activities (what will the future business scope be?) and structural changes (e.g., ‘Do you plan to integrate new operations into existing business structures?’).

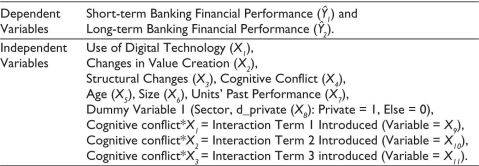

Digital transformation indicators revealed appropriate information extraction extent (communality rate > 0.50 level), variance explained rate (76.44%) with a Cronbach alpha reliability of 0.887. Digital transformation has been taken as a predictor variable. The dependent variable or outcome variable has been taken as the bank’s financial performance. The financial performance has been measured with the help of four subjective indicators where the comparison has been done for at least three financial years to its competitors: (a) returns on sales (ROS), (b) return on assets (ROA), (c) return on equity (ROE) and (d) returns on investments. A 7-point scale has been taken, where 1 indicates much lower performance and 7 indicates much higher performance (Newbert, 2008). The extracted factor analysis indicated that all the variables have communality values > 0.77 (Field, 2019), variance explained rate (69.74%) with Cronbach alpha reliability = 0.811. The moderated role of cognitive conflict has been analysed with the help of a 4-item scale developed by Jehn. Cronbach alpha for a single-factor model was 0.851. The role of cognitive conflict has been found associated with the work environment of the business units which brings the upshot of disagreements of ideas, opinions and crucial judgements about strategic decisions to achieve a shared unit target. This mediator has been introduced in the research framework to have an eye on better performance indicators and analyse the changed impact of digital transformation mechanism on banking financial performance. For example, ‘How much disagreement arise between the members in your unit about the ideas about strategic decision implementation?’ or ‘Did your group discussion find a solution?’ The Cronbach alpha was 0.802. Control variables have also been introduced to govern their impacts, such as age, size, sector type and unit’s past performance. Age includes the number of years of the creation of a particular unit, size represents the average figure of employees for the last three years and sector means public or private that has been taken as a dummy variable, and past performance has been computed for three years with average revenue of particular unit (Bedford et al., 2019; Jehn, 1995). Bharadwaj et al. (2013), Sebastian et al. (2017) and Tumbas et al. (2017) also highlighted that the age, type or size of an organisation preceding the advent of digitalisation need to reform their business products, processes and technology fully to make its survival possible for the upcoming competitive business environment. Control variables have been undertaken from existing literature, which may have a significant impact on the financial performance of banks. Age, sector, size and past performance have been taken to remove confounding effects upon the dependent variable. The effect of digitalisation on financial performance has been accurately predicted while controlling these control variables and achieves a more realistic apple-to-apple comparison between banks (Bedford et al., 2019; Jehn, 1995).

Results

Confirmatory factor analysis has been performed to confirm the measured variables in our study after EFA. The outcome analysis indicated the four-factor model is a good fit with Chi-square value = 21,887.21 (p = .000) (Kaiser, 1960); (TLI = 0.944, CFI = 0.948; RMEEA < 0.10 exactly = 0.041). All the variables have been loaded with their factors significantly in the model fitted and passed through reliability and validity analysis (Field, 2019). Further correlation coefficients have been found statistically significant (p < .05) between the variables under study. The extracted variance has been divided into two parts: explained variance, which is described by independent variables, and unexplained variance, which is not described by independent variables, that is, residuals. No problem of multicollinearity occurred in the present analysis as the data represent a good fit (VIF .png) 3; all the values are under permissible limit) (Dale,, 2003; Field 2019).

3; all the values are under permissible limit) (Dale,, 2003; Field 2019).

Table 2. Dependent and Independent Variables Taken for Study.

Source: Authors’ Elaborations and Data variables entered into Analysis

Model Development

Testing of Hypothesis

The higher value of F-statistics (Table 3) denotes its significance and rejection of the theoretical basis null hypothesis, which states that one or more partial regression coefficients have a beta value .png) 0. Thus, the model signifies a good fit. Both Ha and Hb have been tested with the help of multiple regression analysis under structural equation modelling. The effect of the digital transformation mechanism has been analysed, and resultant positive indications have been stimulated (Amason, 1996; Chanias et al., 2019). The effect of variables, such as the use of digital technologies, changes in value creation and the effect of structural changes, has been found to positively influence short-term and long-term financial performance of the banking sector units along with an insignificant effect of the type of unit whether public or private. It reflects that the type of unit affects insignificantly the financial performance of banks. Thus, the results supported the hypothesis, that is, Ha and Hb (Table 3). The effect of control variables, such as age, units’ size and sector type, has been found insignificant towards the outcome variable, that is, banks’ financial performance (both short-term and long-term). Only the effect of units’ past performance has been found significant. The standardised beta coefficients of regression indicated the positive relationship of the three major drivers of the digital mechanism such as the use of digital technologies (β = 0.335, SE = 0.037, p < .01), changes in value creation (β = 0.441, SE = 0.044, p < .01), and the effect of structural changes (β = 0.553, SE = 0.045, p < .01) has been found positive towards the long- and short-term performance of banking sector units under study. This indicates the acceptance of both Ha and Hb in our current research. The extracted values of R2 and

0. Thus, the model signifies a good fit. Both Ha and Hb have been tested with the help of multiple regression analysis under structural equation modelling. The effect of the digital transformation mechanism has been analysed, and resultant positive indications have been stimulated (Amason, 1996; Chanias et al., 2019). The effect of variables, such as the use of digital technologies, changes in value creation and the effect of structural changes, has been found to positively influence short-term and long-term financial performance of the banking sector units along with an insignificant effect of the type of unit whether public or private. It reflects that the type of unit affects insignificantly the financial performance of banks. Thus, the results supported the hypothesis, that is, Ha and Hb (Table 3). The effect of control variables, such as age, units’ size and sector type, has been found insignificant towards the outcome variable, that is, banks’ financial performance (both short-term and long-term). Only the effect of units’ past performance has been found significant. The standardised beta coefficients of regression indicated the positive relationship of the three major drivers of the digital mechanism such as the use of digital technologies (β = 0.335, SE = 0.037, p < .01), changes in value creation (β = 0.441, SE = 0.044, p < .01), and the effect of structural changes (β = 0.553, SE = 0.045, p < .01) has been found positive towards the long- and short-term performance of banking sector units under study. This indicates the acceptance of both Ha and Hb in our current research. The extracted values of R2 and .png) R2 were 0.487 and 0.231 for long-term performance (

R2 were 0.487 and 0.231 for long-term performance (.png) 2) and 0.334 and 0.087 for short-term financial performance (1). The analysis further highlights the context that the independent variables of digital transformation mechanism and cognitive conflict together explain the variance of long-term (23.10%) and short-term (0.087%) financial performance of banks. The analysis identified the major significant impact of digital transformation mechanism on long-term financial performance as compared to the short-term position. Amason (1996) strongly built the relationship between digital transformation variables and cognitive conflict towards the positive and better achievement of financial performance. The results are also in agreement with those of Bercovitch (1982) and Parayitam and Dooley (2011).

2) and 0.334 and 0.087 for short-term financial performance (1). The analysis further highlights the context that the independent variables of digital transformation mechanism and cognitive conflict together explain the variance of long-term (23.10%) and short-term (0.087%) financial performance of banks. The analysis identified the major significant impact of digital transformation mechanism on long-term financial performance as compared to the short-term position. Amason (1996) strongly built the relationship between digital transformation variables and cognitive conflict towards the positive and better achievement of financial performance. The results are also in agreement with those of Bercovitch (1982) and Parayitam and Dooley (2011).

Table 3. Regression Coefficients with Standard Errors Results.

Notes: * p < .05; ** p < .01; *** p < .001; .png) , insignificant. The four-factor model is a good fit with

, insignificant. The four-factor model is a good fit with .png) 2 = 21,887.21, p < .001; TLI = 0.944; CFI = 0.948; RMEEA = 0.041. All measurement items loaded significantly.

2 = 21,887.21, p < .001; TLI = 0.944; CFI = 0.948; RMEEA = 0.041. All measurement items loaded significantly.

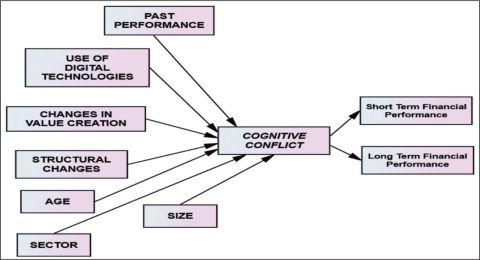

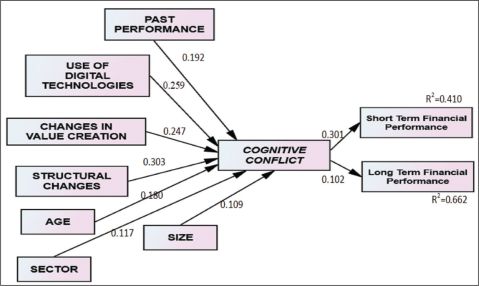

Figure 3. Diagrammatical Representation of Theoretical Model: With Mediator Cognitive Conflict.

Figure 4. Structure of Path Model: With Cognitive Conflict as Mediator (Structured Equation Modelling).

Source: Model results; path coefficients—model signifies the impact of digital transformation mechanism upon the financial performance as a predicted variable.

The Study of Interactions-moderated Role of Cognitive Conflict

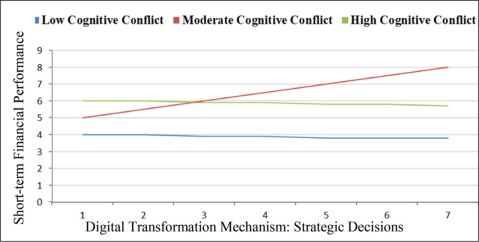

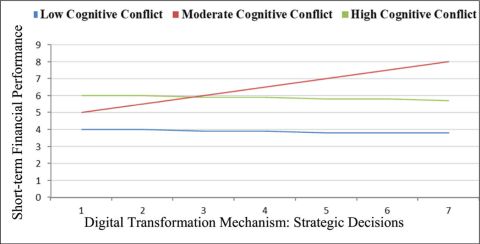

The moderating effect of cognitive conflict has been taken under the present analysis in between the strategies of digital transformation and banking unit financial (short- and long-term) performance. The interaction, as indicated in model STR-M3 and LTR-M3 for variable X9 (cognitive conflict*X1), indicates the positive significant relationship between long-term financial performance (β = 0.267, SE = 0.051, p < .01) and short-term financial performance (β = 0.176, SE = 0.071, p < .01) of the banking sector units. In the same models, the interactions for variable X10 (cognitive conflict*X2) also indicate a positive significant relationship between long-term financial performance (β = 0.283, SE = 0.053, p < .01) and short-term financial performance (β = 0.193, SE = 0.061, p < .01). Further, the interactions for variable X11 (cognitive conflict*X3) indicate a positive significant relationship between long-term financial performance (β = 0.342, SE = 0.032, p < .01) and short-term financial performance (β = 0.245, SE = 0.045, p < .01). Afterwards, the effect of interactions between cognitive conflict square (CC2*DTS) and digital transformation mechanism has been found negative in relation to short-term financial performance (β = 0.209**, SE = 0.053, p < .01), but positive towards long-term financial performance. Hence, the results support hypothesis Hg, that is, negative relationship in case of short-term performance, and reject Hf, that is, positive relation in case of long-term performance. The extracted values of R2 and R2 were 0.662 and 0.175 for long-term performance (2) and 0.410 and 0.076 for short-term financial performance (1). The analysis highlights the context that interactions between cognitive conflict and digital transformation together explain 17% variance in the case of long-term financial performance but 7% variance in the case of short-term performance. Line graphs have been further computed in support of the results (Figure 5 and Figure 6). Dooley conducted a study on 109 hospitals in Florida, California, Texas and Colorado and highlighted the curvilinear or inverted U-shaped relationship that exists between cognitive conflict and performance variables. The study emphasised that top management team members need not over-emphasise cognitive conflict beyond a limit because it may have destructive effects too.

Figure 5. Relationship Structure Between Digital Transformation Strategic Decisions and L-T Financial Performance.

Figure 6. Relationship Structure Between Digital Transformation Strategic Decisions and S-T Financial Performance.

Interaction Graphs: Digital Transformation Mechanism with Short-term and Long-term Banking Performance.

As per the theory of Aiken and West (1991) and Cohen and Cohen (1983), the graphs indicating the association between digital transformation mechanism and long-term as well as short-term financial performance have been computed on the basis of standard deviations (the criterion of Aiken and West, 1991, about interactions). Low cognitive conflict lies < +1 SD, moderate cognitive conflict lies between -1 SD.< X < +1 SD, and high level of cognitive conflict lies above > +1 SD (Pedhazur, 1997). Thus, the findings do not indicate a U-shaped relationship, thereby Hf and Hg are not supported. Although the results are indicative of arousing upward linear relationship among low, moderate and high conflicts in long- run financial performance.

Concluding Observations

Digital economy has become significant because of quality improvements in products, processes, technology, structures, value creation and strategic corporate decisions. The adoption of digital transformation is hard and complex, but it affects various business segments due to competition in the worldwide economy. This study focuses on the effective implementation of digital transformation that significantly affects the financial performance of a business enterprise. It will enhance the short- and long-term financial position of a particular unit. The results revealed the significant impact of the digital transformation mechanism upon long-term financial performance as compared to the short-term position. The effect of variables, such as the use of digital technologies, changes in value creation and the effect of structural changes, has been found to positively influence short-term as well as the long-term financial performance of banking sector units. Amason (1996) too strongly builds the relationship between digital transformation variables and long-run financial performance while moderating the effect of cognitive conflict. The effect of age, size and sector has been found insignificant except for the past performance, which significantly affects financial performance (both short-term and long-term) of a business unit. The effect of interactions between cognitive conflict and various dimensions of digital transformation has been found statistically significant, indicating the moderating role of cognitive conflict is very effective. The research has been in consonance with the study by Pelled et al. (1999), indicating that the moderation of cognitive conflict has positive and significant effects on financial performance. The moderated role of cognitive conflict indicated the positive appreciative relationship towards the long-term financial performance of banks under study. Dooley studied 109 hospitals in Florida, California, Texas and Colorado and found a curvilinear or inverted U-shaped relationship between cognitive conflict and performance variables. The study emphasised that top management team members need not over-emphasise cognitive conflict beyond a limit because it may have destructive effects. Studies indicate the detrimental effect of conflict on work and financial performance if it is over the limit. The constructive impact of the digital transformation mechanism while moderating the role of cognition conflict has been studied under the current research framework. The investigation of dysfunctional impact can be studied in the future research.

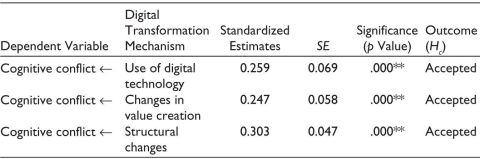

Table 4. Significance of Standardised Estimates for the Relationship Between Digital Transformation Mechanism and Cognitive Conflict.

Source: Calculation under primary data analysis by the author.

Note: Significance levels: * p < .05; ** p < .01.

Table 5. Significance of Standardised Estimates for Relationship Between Digital Transformation and Financial Performance with Mediator: Cognitive Conflict.

Theoretical and Managerial Implications

The managerial implications of the study involve the considerations of numerous factors detailed below:

The Future Directions

Like all research, this study also has its limitations, particularly in terms of time and resources. A more extensive investigation could have been undertaken if not for the geographical constraints. The study too can suffer due to subjective responses. Longitudinal studies can be conducted because attitude tends to change after some time. Only cognitive conflict as a mediated variable has been under study, and other factors, such as mutual understanding, the type of conflict, sources of conflict generation, and task and relationship conflict, should be taken into consideration for future studies. Further, studies can be conducted to explore the wider effect of cognitive conflict upon the other facets of digital transformation variables, such as CEO innovation and IT intensity; moreover, studies can be conducted in other areas rather than in the banking industry, so that its wider scope can be captured in the future (Anderson, 2003; Luce et al., 1999; Nadeem et al., 2018; Nambisan, 2017).

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Shivani Nischal https://orcid.org/0000-0002-3966-1784

Aiken, L. S., & West, S. G. (1991). Multiple regression: Testing and interpreting interactions. Sage Publications.

Al-Debei, M. M., & Avison, D. (2010). Developing a unified framework of the business model concept. European Journal of Information Systems, 19(3), 359–376.

Amason, A. C. (1996). Distinguishing the effects of functional and dysfunctional conflicts on strategic decision making: Resolving a paradox for top management teams. Academy of Management Journal, 39(1), 123–148.

Anderson, C. (2003). The psychology of doing nothing: Forms of decision avoidance result from reason and emotion. Psychological Bulletin, 129(1), 139–167.

Avery, R. B., Raphael, W. B., Paul, S. C., & Glenn, B. C. (1999). Consolidation and bank branching patterns. Journal of Banking and Finance, 23, 2–4.

Bedford, D. S., Bisbe, J., & Sweeney, B. (2019). Performance measurement systems as generators of cognitive conflict in ambidextrous firms. Accounting, Organizations and Society, 72, 21–37.

Bercovitch, J. (1982). Conflict and conflict management in organisations: A framework for analysis (Working Paper). aspheramedia.com/v2/wp-content/uploads/2011/02/5000214.pdf

Besson, P., & Rowe, F. (2012). Strategizing information systems-enabled organizational transformation: A transdisciplinary review and new directions. The Journal of Strategic Information Systems, 21(2), 103–124.

Bharadwaj, A., El Sawy, O. A., Pavlou, P. A., & Venkatraman, N. (2013). Digital business strategy: Toward a next generation of insights. MIS Quarterly, 37(2), 471–482.

Chanias, S., Myers, M. D., & Hess, T. (2019). Digital transformation strategy making in pre-digital organizations: The case of a financial services provider. The Journal of Strategic Information Systems, 28(1), 17–33.

Chia, R. (2004). Strategy-as-practice: Reflections on the research agenda. European Management Review, 1(1), 29–34.

Cohen, J., & Cohen, P. (1983). Applied multiple regression/correlation analysis for the behavioral sciences (2nd ed.). Erlbaum.

Cristina, I. I. (2014). Study on the influence of the number of the ATMs and population upon bank branch evolution. Ovidius University Annals, Economic Sciences Series, 14(1), 136–140. http://stec.univ-ovidius.ro/html/anale/RO/cuprins%20rezumate/volum 2014 p1.pdf

Dale, E. B. (2003). Introduction to multiple regression. wise.cgu.edu/downloads/ regression.doc

Damar, H. E. (2007). Does post-crisis restructuring decrease the availability of banking services: The case of Turkey. Journal of Banking and Finance, 31(9), 2886–2905.

Faro, B., Abedin, B., & Kozanoglu, D. C. (2019). Continuous transformation of public–sector organisations in the digital era. Emergent Research Forum (ERF), Conference: American Conference on Information Systems. https://www.researchgate.net/publication/335096310_Continuous_Transformation_of_Public-sector_Organisations_in_the_Digital_Era

Field, A. (2019). Discovering statistics using IBM SPSS statistics (9th ed.). Sage Publications.

Festinger, L. (1957). A theory of cognitive dissonance. Standard University Press.

Greer, L. L., Jehn, K. A., & Mannix, E. A. (2008). Conflict transformation a longitudinal investigation of the relationships between different types of intragroup conflict and the moderating role of conflict resolution. Small Group Research, 39(3), 278–302.

Hannan, T. H., & Hanweck, G. A. (2007). Recent trends in the number and size of bank branches: An examination of likely determinants. Working Paper, 1–34, http://www.federalreserve.gov/pubs/feds/2012/201202/201202pap.pdf

Henriette, E., Feki, M., & Boughzala, I. (2015). The shape of digital transformation: A systematic literature review. Paper read at Ninth Mediterranean Conference on Information Systems (MCIS), Samos, Greece.

Hess, T., Matt, C., Benlian, A., & Wiesböck, F. (2016). Options for formulating a digital transformation strategy. MIS Quarterly Executive, 15(2), 123–139.

Jarzabkowski, P. (2004). Strategy as practice: Recursiveness, adaptation, and practices- in-use. Organization Studies, 25(4), 529–560.

Jarzabkowski, P. (2005). Strategy as practice: An activity-based approach. Sage Publications.

Jarzabkowski, P., & Spee, A. P. (2009). Strategy-as-practice: A review and future directions for the field. International Journal of Management Reviews, 11(1), 69–95.

Kaiser, H. F. (1960). The application of electronic computers to factor analysis. Educational and Psychological Measurement, 20, 141–151.

Kane, G. C., Palmar, D., Phillips, A. N., Kiron, D., & Buckley, N. (2015). Strategy, not technology, drives digital transformation. MIT Sloan Management Review, 1, 1–25.

Krejcie, R. V., & Morgan, D. W. (1970). Determining sample size for research activities. Educational and Psychological Measurement, 30, 607–610.

Lucas, H. C., Jr, Agarwal, R., Clemons, E. K., El Sawy, O. A., & Weber, B. (2013). Impactful research on transformational information technology: An opportunity to inform new audiences. MIS Quarterly, 37(2), 371–382.

Luce, M. F., Payne, J. W., & Bettman, J. R. (1999). Emotional trade-off difficulty and choice. Journal of Marketing Research, 36(2), 143–159.

Matt, C., Hess, T., & Benlian, A. (2015). Digital transformation strategies. Business and Information Systems Engineering, 57(5), 339–343.

Mithas, S., Tafti, A., & Mitchell, W. (2013). How a firm’s competitive environment and digital strategic posture influence digital business strategy. MIS Quarterly, 37(2), 511–536.

Nadeem, A., Abedin, B., Cerpa, N., & Chew, E. (2018). Digital transformation and digital business strategy in electronic commerce: The role of organizational capabilities. Journal of Theoretical and Applied Electronic Commerce Research, 13(2), 1–8.

Nambisan, S. (2017). Digital entrepreneurship: Toward a digital technology perspective of entrepreneurship. Entrepreneurship Theory and Practice, 41(6), 1029–1055.

Newbert, S. L. (2008). Value, rareness, competitive advantage, and performance: A conceptual-level empirical investigation of the resource-based view of the firm. Strategic Management Journal, 29(7), 745–768.

Nguyen, C., Courtney, M. G. R., & Gillis, S. (2018). Factors affecting primary school achievement in Botswana: A multilevel model for general student performance. International Journal of Quantitative Research in Education, 4(3), 218–239.

Parayitam, S., & Dooley, R. S. (2011). The interplay between cognitive and affective conflict and cognition- and affect-based trust in influencing decision outcomes. Journal of Business Research, 62(8), 789–796.

Pedhazur, E. J. (1997). Multiple regression in behavioral research (3rd ed.). Harcourt Brace.

Pelled, L. H., Eisenhardt, K. M., & Xin, K. R. (1999). Exploring the black box: An analysis of work group diversity, conflict, and performance. Administrative Science Quarterly, 44(1), 1–28.

Reis, J., Amorim, M., Melão, N., & Matos, P. (2018). Digital transformation: A literature review and guidelines for future research. World Conference on Information Systems and Technologies (WorldCIST’18), Naples, 411–421.

Sebastian, I. M., Ross, J. W., Beath, C., Mocker, M., Moloney, K.G., & Fonstad, N. O. (2017). How big old companies navigate digital transformation. MIS Quarterly Executive, 1(1), 197–213.

Tumbas, S., Berente, N., & Vom Brocke, J. (2017). Born digital: Growth trajectories of entrepreneurial organizations spanning institutional fields. Thirty-Eighth International Conference on Information Systems (ICIS), South Korea, Seoul.

Vial, G. (2019). Understanding digital transformation: A review and a research agenda. The Journal of Strategic Information Systems, 28(2), 118–144.

Warner, K. S. R., & Wäger, M. (2019). Building dynamic capabilities for digital transformation: An ongoing process of strategic renewal. Long Range Planning, 52(3), 326–349.

Whittington, R. (1996). Strategy as practice. Long Range Planning, 292(5), 731–735.

Whittington, R. (2006). Completing the practice turn in strategy research. Organization Studies, 27(5), 613–634.

Yang, J., & Mossholder, K. (2004). Decoupling task and relationship conflict: The role of intragroup emotional processing. Journal of Organizational Behavior, 25(5), 589–605.