Review of Professional Management

Search

Search

Reena Kumari1  and Pranay Parashar1

and Pranay Parashar1

1 Department of Commerce and Financial Studies, Central University of Jharkhand, Ranchi, Jharkhand, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

This article aims to systematically review the literature on cognitive heuristic-driven bias and its impact on investment management, identifying gaps and providing future directions for investors, researchers, and academics. The study critically reviewed 71 relevant articles in the Scopus database published between 1980 and 2023. It synthesised the literature on behavioural finance, particularly focusing on cognitive heuristic-driven biases and their influence on investment decision-making and performance. Investors in the financial market are influenced by cognitive biases such as overconfidence, representativeness, anchoring, availability, and adjustment heuristics. These biases impact investment decision-making and performance, potentially leading to suboptimal decisions and undermining market efficiency. Further research on other cognitive factors like the gambler’s fallacy and framing is needed and also explores the recognition of heuristic-driven bias. Investors, both individual and institutional, must be more aware of these biases. This study highlights that the global investor community is unknowingly affected by these biases. Understanding these biases is increasingly crucial due to the expanding investment market and the rise of individual investors in financial markets. This study is also significant for researchers, academics and professionals in the domain of behavioural finance, providing crucial insights into the influence of cognitive heuristic-driven biases in management activities.

Systematic literature review, behavioural finance, behavioural biases, cognitive heuristic-driven biases, investment decisions, investment performance

Introduction

The traditional theories in economics and finance assert that investors are rational beings in the sense that they consider all relevant information before making an investment decision. Neoclassical or Traditional Finance comprises of various concepts and theories, including Expected Utility Theory (Bernoulli, 1738), Markowitz Portfolio Theory (Markowitz, 1952), Miller and Modigliani Theory (1961), Sharpe’s (1964) Capital Assets Pricing Model Theory, and Fama’s (1965) Efficient Market Theory, etc. It can be noted from the aforesaid theories that traditional finance theories depend heavily upon two basic assumptions—first that human beings are rational and second that the markets are efficient and contain all the relevant information required for financial decision-making.

Behavioural finance is a newly emerging field within finance that challenges the traditional assumptions of perfect rationality and market efficiency (Sharma & Kumar, 2019). It focuses on studying investment decisions as an ongoing process, taking into account the cognitive and emotional biases that can influence these decisions (Kumar & Goyal, 2015). As per the behavioural finance theories, it is common for investors to demonstrate irrational behaviour in the stock market, which contrasts with the traditional finance assumptions that investors are rational beings (Mushinada & Veluri, 2019). This field studies how individuals and groups act in the stock market, as investors, analysts and portfolio managers. It aims to understand the influence of emotions and cognitive biases on investment behaviour (Madaan & Singh, 2019). The field of behavioural finance examines how psychological and social factors influence the decision-making processes of finance professionals and the resulting impact on market behaviour (Ahmad et al., 2023).

This study synthesises the existing literature in behavioural finance, primarily focusing on cognitive heuristic-driven biases and their impact on investment decision-making and investment performance. Tversky and Kahneman (1974) were pioneers in defining heuristics and classified heuristics into three categories: Representativeness, anchoring and availability bias. Subsequently, Waweru et al. (2008) expanded this list by adding overconfidence and gambler’s fallacy as additional heuristics. Tversky and Kahneman (1973) proposed that in order to cope with the limited information processing capability, individuals can rely on heuristics that simplify decision-making but restrict the use of information. This can result in systematic errors in evaluation and sub-optimal investment choices. Investors often employ heuristics and mental shortcuts, which give rise to various behavioural biases, particularly recognition and cognitive heuristic biases can significantly impede the ability to make optimal stock trading decisions (Ahmad & Wu, 2023; Kumari et al., 2025).

Overall, this study focuses on cognitive-based heuristic biases and their impact on investment decisions and performance, while also exploring the foundations of behavioural finance and heuristic theory. There is currently a gap in the literature regarding a systematic review that specifically addresses cognitive heuristic-driven biases, with particular emphasis on four predominant biases: Overconfidence Bias, Representativeness Bias, Availability Bias and Anchoring & Adjustment Bias. By focusing on these cognitive biases, this research aims to provide a deeper understanding of how mental processes influence decision-making outcomes within the investment context. Additionally, existing research by Cascão et al. (2023); Khan et al. (2020); Kumari et al. (2025); Richie and Josephson (2018); Sumantri et al. (2024) highlights critical heuristic biases that significantly affect investors’ decision-making and the performance of individual investors, which include representativeness, overconfidence, anchoring and availability bias.

The following sections provide a structured approach to understanding the research: In the second section, the authors review previous studies that explore the relationship between heuristic-driven biases and investment management activities, such as investment decision-making and performance. The third section outlines the data collection and analysis method. The fourth section explores the findings and identifies research gaps in the fifth section. Finally, the sixth section presents the conclusions and implications derived from this article’s results, as well as proposes potential areas for future research.

Literature Review

Heuristic Theory

Heuristics theory states that decision-makers utilise shortcuts to minimise the risk of losses in uncertain situations (Ritter, 2003). Heuristics are mental shortcuts used to simplify decision-making and problem-solving, especially when dealing with complex problems and incomplete information (Ritter, 1988). The word ‘heuristic’ was initially explained by Tversky and Kahneman (1974) in their influential article ‘Judgment Under Uncertainty: Heuristics and Biases’. In their seminal work of 1974, Tversky and Kahneman (1974) examined heuristics and outlined three key biases: representativeness, availability and adjustment anchoring. Subsequently, Waweru et al. (2008) expanded upon this framework by introducing additional heuristics, namely overconfidence. Investors’ decisions in the financial markets are influenced by several heuristic-driven biases, specifically, recognition-based heuristics like name memorability, name fluency and alphabetical order, as well as other cognitive heuristic biases, such as herding behaviour, disposition effect, overconfidence, anchoring and adjustment, representativeness and availability biases (Ahmad & Wu, 2023).

Cognitive Heuristic-driven Biases

This article examines the four most prominent cognitive heuristics biases: Overconfidence, representativeness, availability and anchoring & adjustment bias.

Overconfidence Bias

Overconfidence bias can lead individuals to inaccurately assess their competence, expertise, and skills, seeing themselves as highly capable participants who are capable of achieving greater financial gains (Asad et al., 2018). Abreu and Mendes (2012) have defined overconfidence as the belief held by investors that their decisions are superior to the average and the actual reality. This overconfidence often leads to a distorted perception of the accuracy of an investor’s knowledge and an inflated sense of their own capabilities in analysing the information at hand (Nofsinger, 2013).

Representativeness Bias

The ‘representativeness heuristic’ was initially explained by psychologists Amos Tversky and Daniel Kahneman during the 1970s. Similar to other heuristics, decision-making based on representation aims to serve as a cognitive shortcut, enabling us to make prompt decisions. Nevertheless, it can also lead to inaccuracies. Representativeness is a cognitive bias that involves making judgments using an analogy-based approach. This means that decisions are more likely to be influenced by small samples due to the inherent uncertainty involved (Busenitz & Barney, 2017). The representativeness heuristic ultimately leads decision-makers to depend on a small sample of a population to update their beliefs rather than relying on complex data when making decisions (Shah et al., 2018).

Availability Bias

Availability bias is a mental shortcut that relies on readily available information that comes to mind or the ease of recalling specific events and frequency of experiences with similar events (Tversky & Kahneman, 1973). It is a cognitive heuristic bias, which occurs when a decision-maker relies on quickly accessible information instead of considering other options and procedures. In the stock market, decision-makers are greatly influenced by the information they receive during the process of selecting and identifying stocks (Khan et al., 2017).

Anchoring and Adjustment Bias

The anchoring bias was initially discovered by Tversky and Kahneman (1974) during their laboratory experiment as an anchoring and adjustment bias. This bias refers to the inclination of individuals to heavily depend on the initial information they receive and inadequately adjust it when making final decisions. Slovic and Lichtenstein (1971), states that anchoring and adjustment bias occur when individuals utilise initial information to form estimates, which are then adapted to arrive at the final answer. These initial values can be modified through problem formulation or suggested through partial computation. In addition to that, Tversky and Kahneman (1974) assert that different starting points produce varying estimates, influenced by the initial value. This phenomenon is referred to as anchoring. Hence, the anchoring and adjustment bias can be traced to investors’ propensity to ‘anchor’ their thoughts to an irrelevant reference point when making decisions (Pompian, 2011).

Research Methodology

This article employs the systematic literature review (SLR) method to critically review the existing literature on cognitive heuristic-driven biases in behavioural finance. The SLR methodology is a comprehensive analysis of existing research on a clearly defined subject, using systematic and clear techniques to identify, select and evaluate relevant studies. It involves the meticulous extraction and critical analysis of data and findings from these chosen studies (Christofi et al., 2017). Typically, systematic reviews aim to generate comprehensive understanding by synthesising research findings, thereby enhancing methodological robustness and establishing a reliable knowledge base to guide future research endeavours (Tranfield et al., 2003).

Considering these factors, the authors assert that the SLR is the most effective way to achieve the research objective, which is to provide a comprehensive and high-quality overview of the literature concerning cognitive heuristic-driven biases and their influence on investment decision-making and investment performance.

There are various frameworks exist for reporting SLRs, but this study employs the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) Model, as outlined by Page et al. (2021). The PRISMA framework is organised into four stages: identification, screening, eligibility and inclusion. It provides a standardised checklist that outlines essential components to be included in a systematic review report. The adoption of the PRISMA framework is intentional, as it offers a robust and transparent methodology, ensuring that the SLR is executed with a high degree of rigour and clarity (Page et al., 2021; Rethlefsen et al., 2021).

Formulation of the Research Questions

This study’s primary goal is to carry out a systematic review of the existing body of knowledge by exploring the heuristic bias. Research questions were defined at this stage. Four research questions were framed for this study, which are as follows:

Identification

The initial phase of conducting the SLR process involves the identification of relevant keywords for accessing the appropriate literature (Moher et al., 2009). The selected keywords serve as the foundation for developing search strings focused on cognitive heuristic bias. The primary search string is intended to be applied to titles, keywords and abstracts of articles related to heuristic bias. To construct the search string, Boolean operators, specifically AND and OR, with the option to utilise various combinations of these operators (Kumari et al., 2024; Moher et al., 2009; Page et al., 2021).

This study predominantly employs the Scopus database for literature reviews, as it is widely recognised as a reliable source for scientific articles (Baas et al., 2020; Mongeon & Paul-Hus, 2016). The choice of Scopus is deliberate, given its distinguished reputation in the academic community for consistently publishing high-quality research. As the most extensive abstract and citation database available, Scopus covers a wide range of literature, including scientific journals, books and conference proceedings (Schotten et al., 2019).

Moreover, the authors implemented stringent inclusion and exclusion criteria to delineate the research sample for the study shown in Table 1. This extensive search, which included all publications up to December 2023, aimed to identify significant articles using key search terms such as ‘heuristic*’ OR ‘heuristic-driven bias’ OR ‘heuristic decision-making’ OR ‘cognitive heuristic*’ OR ‘cognitive heuristic-driven bias*’ OR ‘behavioural heuristic factor*’ AND ‘investment decision*’ OR ‘financial decision*’ OR ‘investment performance’. These approaches were carefully applied to articles’ topics, titles, keywords, and abstracts in the Scopus database.

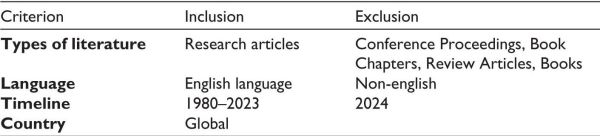

Table 1. Inclusion and Exclusion Criteria.

To maintain quality and rigour in the research, only peer-reviewed articles published in English were included in the selection process. The author’s focus was specifically on the areas of ‘Business, Management, and Accounting’, ‘Social Science’, ‘Economics, Econometrics, and Finance’, and ‘Arts and Humanities, and Psychology’, all of which are critically relevant to the field of behavioural finance. Ultimately, this thorough approach yielded an initial collection of 189 relevant articles, after judiciously excluding 177 studies from a total of 366 references sourced from the Scopus database.

Screening

In the second phase of the study, a comprehensive screening process was conducted on all articles identified from the selected database based on the search string and followed the inclusion and exclusion criteria. To enhance the relevance of the results in relation to the research objective, the authors independently reviewed the titles and abstracts of the articles, leading to the exclusion of 74 articles that did not align with the research objective.

Eligibility

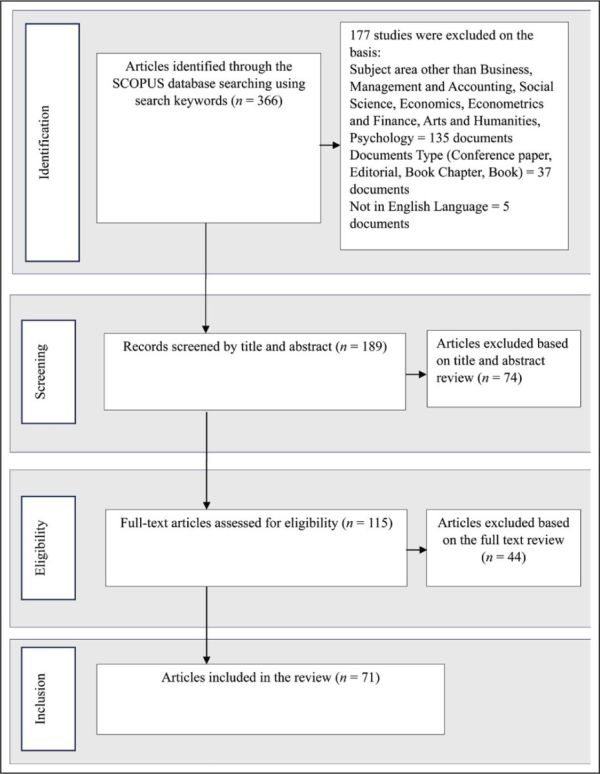

This phase worked collaboratively with the screening phase to ensure that all selected journal articles met the necessary criteria. As shown in Figure 1, a total of 115 articles were identified for further examination. These articles were carefully analysed for their relevance to cognitive heuristic bias, involving a thorough examination of the full texts and their abstracts, which excluded 44 articles.

Figure 1. PRISMA Flow Diagram of the Literature Search and Articles’ Selection for the SLR.

Inclusion

In the last phase, the authors identified 71 main articles that form the foundation of this analysis. The data were systematically summarised and analyse. Subsequently, the authors discuss the findings of this article, and enhance the understanding of the cognitive heuristic bias for further study.

Findings

In this section, the authors discuss the findings with respect to the heuristic biases and their impact on investment decisions and investment performance based on 71 shortlisted studies on cognitive heuristic-driven biases.

Findings on Overconfidence Bias

The findings of this study confirm that investors behave irrationally and make trading mistakes due to heuristic biases. Through the review of the literature, it was found that the overconfidence heuristic has a significant negative influence on the investment decisions of individual investors. Psychologically, this means that, due to overconfidence bias, investors cannot take appropriate investment decisions. Overconfident investors tend to make inappropriate or risky investments and they may trade excessively, which can have a negative effect on their returns (Kafayat, 2014; Waweru et al., 2008). Overconfidence serves as a heuristic that investors depend on, seemingly to mitigate the potential losses in uncertain circumstances. By employing heuristics, individual investors compromise their technical expertise and logical thinking abilities, consequently leading to erroneous judgments (Ahmad & Shah, 2020). Investors frequently make irrational decisions, which then negatively affects their investment performance (Shah et al., 2018). Overconfidence prompts investors to increase their asset purchases when they receive positive signals from the market, and conversely, to sell off more assets when they receive negative signals (Wang, 2001). Kafayat (2014) stated that the overconfidence bias negatively impacts the investment decision. In a similar vein, Park et al. (2010) and Kengatharan and Kengatharan (2014) propose that investment decisions and investment performance are adversely affected by overconfidence.

Findings on Representativeness Bias

The present study also provides evidence regarding the bias—representativeness. Several researchers have carried out studies on the representativeness bias and its impact on investment management activities (Ahmed & Safdar, 2017; Dias et al., 2019; Irshad et al., 2016; Khan & Bashir, 2020). Certain studies have shown a positive connection between representativeness bias and investment decisions, suggesting that this bias can effectively improve the investment decision-making process (Khan et al., 2020; Rehan & Umer, 2017; Toma, 2015). In a study conducted by Irshad et al. (2016), it was revealed that a significant positive correlation exists between representativeness bias and investment decisions. Correspondingly, Ikram (2016) found that individual investors trading on the Islamabad Stock Exchange was notably influenced by representativeness bias when making their decisions. This bias had a positive impact on the returns of those investors, leading to an increase in their overall profitability. Conversely, in some studies, researchers demonstrate a negative correlation (Parveen et al., 2020; Tin & Wee-Siong Hii, 2020) between the representativeness bias and investment decision-making. Researchers argue that this bias reduces the quality of investment decision-making as individuals struggle to make rational decisions, leading to irrational behaviour in the market. As a result, they tend to make trading errors as a consequence of relying on the representativeness heuristic.

Barber and Odean (1999) findings further support this, highlighting a significant correlation between representativeness bias and investment performance. They elucidated that investors are drawn toward stocks that capture public attention or have witnessed unexpectedly high trading volumes. Additionally, Abdin et al. (2017) posit that representativeness impacts both investment decisions as well as performance.

Findings on Availability Bias

Similarly, this study also highlights the significance of availability bias in the financial market. The significance of availability bias in the stock market has been highlighted by Chiodo et al. (2003). Their research indicates that availability can lead to either under-reaction or overreaction in expectations, consequently impacting asset prices. Similarly, Salman et al. (2021) assert that a substantial number of individual investors were affected by the availability heuristic at the Stock Exchange. The availability heuristic significantly influences investors’ decisions, leading them to view a stock with favourable earnings as less risky and a stock with poor earnings as highly risky (Richie & Josephson, 2018; Shantha Gowri & Ram, 2019). Consequently, this cognitive bias leads to suboptimal investment decisions (Ganzach, 2000). Investor preferences are based on available information, which leads to a specific trend in decision-making. Occasionally, even insignificant information can impact investment decisions (Van den Steen, 2002).

Findings on Anchoring and Adjustment Bias

Additionally, many studies have shown that anchoring and adjustment bias influence the different types of financial investment decisions, such as real estate (Pandey & Jessica, 2018); debt securities (Tin & Wee-Siong Hii, 2020); housing investment (Cascão et al., 2023). According to Ahmad et al. (2020), the anchoring heuristic impacts investment decision-making, often negatively affecting entrepreneurs in emerging markets. In a study conducted by Lowies et al. (2016), it was found that anchoring and adjustment bias significantly influence the investment decisions of listed South African property fund managers. This bias has the potential to result in judgment errors and the possibility of missed gains (Abraham et al., 2014). Similarly, Obara (2015) highlighted the positive and considerable impact of anchoring bias on investment performance. Contrarily, Shah et al. (2018) found that anchoring bias has a detrimental effect on investment decisions and investment performance. Anchoring heuristic is a prevalent bias that affects various aspects of finance and business decision-making. As a result, it’s crucial for investors and wealth management practitioners to fully understand this behaviour and its impact (Khan et al., 2017).

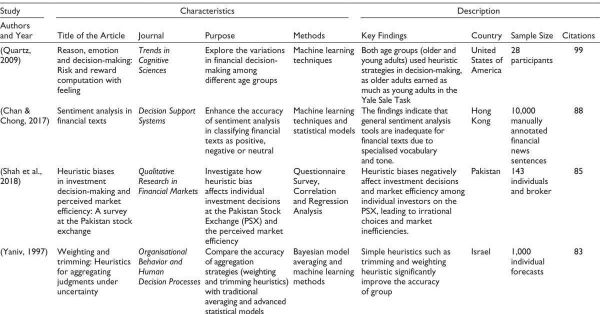

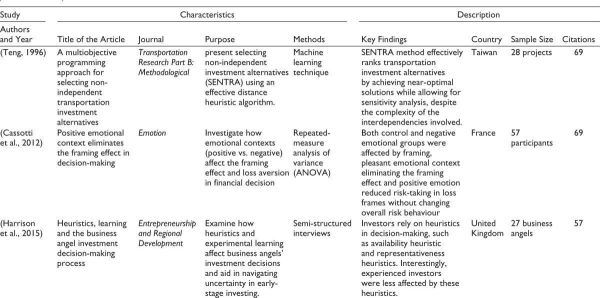

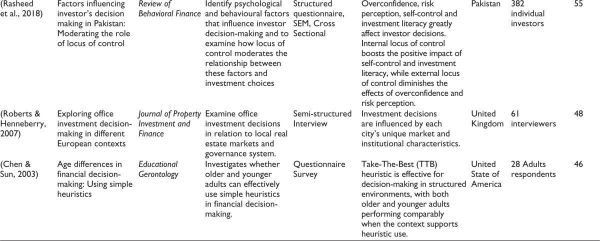

Additionally, Table 2 presenting the most cited articles, along with key study characteristics and insights descriptions, is essential for identifying influential research and understating trends of the cognitive heuristic-driven bias research.

Table 2. Top 10 Cited Articles, Including the Study, Its Characteristics and Its Detailed Description.

Research Gaps

After reviewing the available literature on cognitive heuristic biases, it has been found that there are some gaps which need to be addressed and future studies can be conducted on these gaps. For instance:

Future studies may be conducted to examine the impact of the cognitive heuristic-driven biases on investment decisions as well as investment performance, with a focus on moderating and mediating factors. It is essential to investigate how financial literacy, long-term orientation, and locus of control can moderate these effects, while also considering other variables like risk perceptions and market anomalies can mediate the relationships.

This study also asserts that further study should incorporate other heuristic factors like gambler fallacy; disposition effect, herding, underconfidence, anchoring and representativeness bias. It recommends examining these factors separately will enable a thorough evaluation of their distinct effects on investment decisions, investment performance, and market efficiency.

Furthermore, there is potential for additional research to concentrate on contrasting the diverse categories of investors, including individual investors (retail investors) and institutional investors (financial advisor, pension fund, mutual fund) to find out which investors are less influenced by heuristic biases.

Conclusions and Limitations

This study has presented a detailed analysis of cognitive heuristic-driven biases and their influence on investment decision-making and performance. To achieve rigorous studies on this topic, an SLR approach was conducted of the existing literature in the Scopus database published between 1980 and 2023, resulting in a detailed analysis of 71 articles. The primary goal of this study is to investigate the impact of the various cognitive heuristic biases and their influence on investment decisions and investment performance.

Currently, this particular area of study is experiencing a surge in popularity, and provides invaluable insights into the decision-making processes of investors in the financial markets. The findings of the study propose that most of the investors in the financial market rely on cognitive heuristic biases such as overconfidence, representativeness, anchoring, availability and adjustment heuristic. These biases often lead to suboptimal decision-making. The study highlights the use of heuristics as a means for investors to mitigate risks in uncertain scenarios. However, it also emphasises that this approach can result in errors, leading to irrational decisions that may adversely affect investment performance and also the market efficiency is compromised.

This study is limited in its scope as it solely examines cognitive heuristic-driven bias, further research may be carried out to explore the impact of recognition-based heuristic-driven bias, namely alphabetical ordering, name memorability, and name fluency, which are also heuristic factors, resulting in irrational decisions. Furthermore, there are many heuristic factors like gambler fallacy and framing whose impact can be investigated in investment management activities.

Moreover, this research carries significant practical implications for both individual and institutional investors. Investors, individual as well as institutional, need to be more aware of these biases and this study shall reinforce the fact that globally the investor community is unknowingly plagued with these biases. Although these biases were recorded and reported several years ago, the significance of being aware of these biases has increased multifold, given the expanse of the investment market and the rise in individual (retail) investors’ participation in the financial markets.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Reena Kumari https://orcid.org/0009-0000-9985-4513

Abdin, S. Z. ul, Farooq, O., Sultana, N., & Farooq, M. (2017). The impact of heuristics on investment decision and performance: Exploring multiple mediation mechanisms. Research in International Business and Finance, 42, 674–688. https://doi.org/10.1016/ j.ribaf.2017.07.010

Abraham, G., Hall, J. H., & Cloete, C. E. (2014). Anchoring and adjustment and herding behaviour as heuristic-driven bias in property investment decision-making in South Africa (No. eres2014_217). European Real Estate Society (ERES). Retrieved July 28, 2025, from https://eres.architexturez.net/doc/oai-eres-id-eres2014-217

Abreu, M., & Mendes, V. (2012). Information, overconfidence and trading: Do the sources of information matter? Journal of Economic Psychology, 33(4), 868–881. https://doi.org/10.1016/J.JOEP.2012.04.003

Ahmad, M., & Shah, S. Z. A. (2020). Overconfidence heuristic-driven bias in investment decision-making and performance: Mediating effects of risk perception and moderating effects of financial literacy. Journal of Economic and Administrative Sciences, 38(1), 60–90. https://doi.org/10.1108/JEAS-07-2020-0116

Ahmad, M., Shah, S. Z. A., & Abbass, Y. (2020). The role of heuristic-driven biases in entrepreneurial strategic decision-making: Evidence from an emerging economy. Management Decision, 59(3), 669–691. https://doi.org/10.1108/MD-09-2019-1231

Ahmad, M., & Wu, Q. (2023). Heuristic-driven biases as mental shortcuts in investment management activities: A qualitative study. Qualitative Research in Financial Markets. https://doi.org/10.1108/QRFM-10-2022-0167/FULL/HTML

Ahmad, M., Wu, Q., & Abbass, Y. (2023). Probing the impact of recognition-based heuristic biases on investment decision-making and performance. Kybernetes, 52(10), 4229–4256. https://doi.org/10.1108/K-01-2022-0112

Ahmed, A. S., & Safdar, I. (2017). Evidence on the presence of representativeness bias in investor interpretation of consistency in sales growth. Management Science, 63(1), 97–113. https://doi.org/10.1287/mnsc.2015.2326

Asad, H., Khan, A., & Faiz, R. (2018). Behavioral biases across the stock market investors. Pakistan Economic and Social Review, 56(1), 185–209. https://www.jstor.org/stable/26616737

Baas, J., Schotten, M., Plume, A., Côté, G., & Karimi, R. (2020). Scopus as a curated, high-quality bibliometric data source for academic research in quantitative science studies. Quantitative Science Studies, 1(1), 377–386. https://doi.org/10.1162/QSS_A_00019

Barber, B. M., & Odean, T. (1999). The courage of misguided convictions. Financial Analysts Journal, 55(6), 41–55. https://www.jstor.org/stable/4480208

Bernoulli, D. (1738). Specimen theoriae novae de mensura sortis. Commentarii Academiae Scientiarum Imperialis Petropolitanae, 5, 175–192. https://archive.org/details/ SpecimenTheoriaeNovaeDeMensuraSortis/page/n15/mode/2up

Busenitz, L. W., & Barney, J. B. (2017). Biases and heuristics in strategic decision making: Differences between entrepreneurs and managers in large organizations. Academy of Management, 1994(1), 85–89. https://doi.org/10.5465/AMBPP.1994.10341736

Cascão, A., Quelhas, A. P., & Cunha, A. M. (2023). Heuristics and cognitive biases in the housing investment market. International Journal of Housing Markets and Analysis, 16(5), 991–1006. https://doi.org/10.1108/IJHMA-05-2022-0073

Cassotti, M., Habib, M., Poirel, N., Aïte, A., Houdé, O., & Moutier, S. (2012). Positive emotional context eliminates the framing effect in decision-making. Emotion, 12(5), 926–931. https://doi.org/10.1037/a0026788

Chan, S. W. K., & Chong, M. W. C. (2017). Sentiment analysis in financial texts. Decision Support Systems, 94, 53–64. https://doi.org/10.1016/j.dss.2016.10.006

Chen, Y., & Sun, Y. (2003). Age differences in financial decision-making: Using simple heuristics. Educational Gerontology, 29(7), 627–635. https://doi.org/10.1080/713844418

Chiodo, A. J., Guidolin, M., Owyang, M. T., & Shimoji, M. (2003). Subjective probabilities: Psychological evidence and economic applications. http://research.stlouisfed.org/wp/2003/2003-009.pdf

Christofi, M., Leonidou, E., & Vrontis, D. (2017). Marketing research on mergers and acquisitions: A systematic review and future directions. International Marketing Review, 34(5), 629–651. https://doi.org/10.1108/IMR-03-2015-0100/FULL/XML

Dias, N., Avila, M., Campani, C. H., & Maranho, F. (2019). The heuristic of representativeness and overconfidence bias in entrepreneurs. Latin American Business Review, 20(4), 317–340. https://doi.org/10.1080/10978526.2019.1656536

Fama, E. F. (1965). The behavior of stock-market prices. The Journal of Business, 38(1), 35–105. https://www.jstor.org/stable/2350752

Ganzach, Y. (2000). Judging risk and return of financial assets. Organizational Behavior and Human Decision Processes, 83(2), 353–370. https://doi.org/10.1006/OBHD. 2000.2914

Harrison, R. T., Mason, C., & Smith, D. (2015). Heuristics, learning and the business angel investment decision-making process. Entrepreneurship and Regional Development, 27(9–10), 527–554. https://doi.org/10.1080/08985626.2015.1066875

Ikram, Z. (2016). An empirical investigation on behavioral determinants on impact on investment decision making, moderating role of locus of control. Journal of Poverty, Investment and Development, 26. https://iiste.org/Journals/index.php/JPID/article/view/31771

Irshad, S., Badshah, W., & Hakam, U. (2016). Effect of representativeness bias on investment decision making. Management and Administrative Science Review, 5(1), 26–30.

Kafayat, A. (2014). Interrelationship of biases: Effect investment decisions ultimately. Theoretical and Applied Economics, XXI(6), 85–110.

Kengatharan, L., & Kengatharan, N. (2014). The influence of behavioral factors in making investment decisions and performance: Study on investors of Colombo Stock Exchange, Sri Lanka. Asian Journal of Finance & Accounting, 6(1). https://doi.org/10.5296/ajfa.v6i1.4893

Khan, A., & Bashir, T. (2020). Scale development and exploration in representativeness bias intervening investment and financial decisions. Pakistan Social Sciences Review, 4(1), 403–417.

Khan, H. H., Naz, I., Qureshi, F., & Ghafoor, A. (2017). Heuristics and stock buying decision: Evidence from Malaysian and Pakistani stock markets. Borsa Istanbul Review, 17(2), 97–110. https://doi.org/10.1016/j.bir.2016.12.002

Khan, I., Afeef, M., Jan, S., & Ihsan, A. (2020). The impact of heuristic biases on investors’ investment decision in Pakistan stock market: Moderating role of long-term orientation. Qualitative Research in Financial Markets, 13(2), 252–274. https://doi.org/10.1108/QRFM-03-2020-0028

Kumar, S., & Goyal, N. (2015). Behavioural biases in investment decision making: A systematic literature review. Qualitative Research in Financial Markets, 7(1), 88–108. https://doi.org/10.1108/QRFM-07-2014-0022

Kumari, R., Parashar, P., & Sangma, A. (2024). A bibliometric overview of fund managers’ bias: Research contributions and influence. Journal of Operations and Strategic Planning. https://doi.org/10.1177/2516600X241245776

Kumari, R., Parashar, P., Sangma, A., & Das, J. (2025). Research patterns and intellectual structure of heuristic bias: A bibliometric overview using SPAR-4-SLR approach. In Global Knowledge, Memory and Communication. Emerald Publishing. https://doi.org/10.1108/GKMC-06-2024-0392

Lowies, G. A., Hall, J. H., & Cloete, C. E. (2016). Heuristic-driven bias in property investment decision-making in South Africa. Journal of Property Investment and Finance, 34(1), 51–67. https://doi.org/10.1108/JPIF-08-2014-0055

Madaan, G., & Singh, S. (2019). An analysis of behavioral biases in investment decision-making. International Journal of Financial Research, 10(4). http://dx.doi.org/10.5430/ijfr.v10n4p55

Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77–91. https://doi.org/10.2307/2975974

Miller, M. H., & Modigliani, F. (1961). Dividend policy, growth, and the valuation of shares. The Journal of Business, 34(4), 411–433. https://doi.org/10.1086/294442

Moher, D., Liberati, A., Tetzlaff, J., Altman, D. G., Antes, G., Atkins, D., Barbour, V., Barrowman, N., Berlin, J. A., Clark, J., Clarke, M., Cook, D., D’Amico, R., Deeks, J. J., Devereaux, P. J., Dickersin, K., Egger, M., Ernst, E., Gøtzsche, P. C., … Tugwell, P. (2009). Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. PLoS Medicine, 6(7). https://doi.org/10.1371/ journal.pmed.1000097

Mongeon, P., & Paul-Hus, A. (2016). The journal coverage of Web of Science and Scopus: A comparative analysis. Scientometrics, 106(1), 213–228. https://doi.org/10.1007/S11192-015-1765-5/METRICS

Mushinada, V. N. C., & Veluri, V. S. S. (2019). Elucidating investors’ rationality and behavioural biases in Indian stock market. Review of Behavioral Finance, 11(2), 201–219. http://dx.doi.org/10.1108/RBF-04-2018-0034

Nofsinger, J. R. (2013). The psychology of investing (Vol. 5). Routledge. https://doi.org/10.4324/9781315230856

Obara, C. A. (2015). The effect of heuristic biases on investment returns by unit trusts in Kenya. School of Business University of Nairobi. http://erepository.uonbi.ac.ke/handle/11295/94049

Page, M. J., Moher, D., Bossuyt, P. M., Boutron, I., Hoffmann, T. C., Mulrow, C. D., Shamseer, L., Tetzlaff, J. M., Akl, E. A., Brennan, S. E., Chou, R., Glanville, J., Grimshaw, J. M., Hróbjartsson, A., Lalu, M. M., Li, T., Loder, E. W., Mayo-Wilson, E., Mcdonald, S., … Mckenzie, J. E. (2021). PRISMA 2020 explanation and elaboration: Updated guidance and exemplars for reporting systematic reviews. In The BMJ (Vol. 372). BMJ Publishing Group. https://doi.org/10.1136/bmj.n160

Pandey, R., & Jessica, V. M. (2018). Measuring behavioural biases affecting real estate investment decisions in India: Using IRT. International Journal of Housing Markets and Analysis, 11(4), 648–668. https://doi.org/10.1108/IJHMA-12-2017-0103

Park, J., Konana, P., Gu, B., Kumar, A., & Raghunathan, R. (2010). Confirmation bias, overconfidence, and investment performance: Evidence from stock message boards. SSRN Electronic Journal. https://doi.org/10.2139/SSRN.1639470

Parveen, S., Satti, Z. W., Subhan, Q. A., & Jamil, S. (2020). Exploring market overreaction, investors’ sentiments and investment decisions in an emerging stock market. Borsa Istanbul Review, 20(3), 224–235. https://doi.org/10.1016/j.bir.2020.02.002

Pompian, M. M. (2011). Behavioral finance and wealth management: How to build optimal portfolios that account for investor biases. Wiley. https://www.wiley.com/en-us/Behavioral+Finance+and+Wealth+Management%3A+How+to+Build+Optimal+ Portfolios+That+Account+for+Investor+Biases-p-9781118046319

Quartz, S. R. (2009). Reason, emotion and decision-making: Risk and reward computation with feeling. Trends in Cognitive Sciences, 13(5), 209–215. https://doi.org/10.1016/j.tics.2009.02.003

Rasheed, M. H., Rafique, A., Zahid, T., & Akhtar, M. W. (2018). Factors influencing investor’s decision making in Pakistan: Moderating the role of locus of control. Review of Behavioral Finance, 10(1), 70–87. https://doi.org/10.1108/RBF-05-2016-0028

Rehan, R., & Umer, I. (2017). Behavioural biases and investor decisions. Market Forces, 12(2). Retrieved July 28, 2025, from https://kiet.edu.pk/marketforces/index.php/marketforces/article/view/341

Rethlefsen, M. L., Kirtley, S., Waffenschmidt, S., Ayala, A. P., Moher, D., Page, M. J., Koffel, J. B., Blunt, H., Brigham, T., Chang, S., Clark, J., Conway, A., Couban, R., de Kock, S., Farrah, K., Fehrmann, P., Foster, M., Fowler, S. A., Glanville, J., … Young, S. (2021). PRISMA-S: An extension to the PRISMA statement for reporting literature searches in systematic reviews. Systematic Reviews, 10(1), 1–19. https://doi.org/10.1186/S13643-020-01542-Z/TABLES/1

Richie, M., & Josephson, S. A. (2018). Quantifying heuristic bias: Anchoring, availability, and representativeness. Teaching and Learning in Medicine, 30(1), 67–75. https://doi.org/10.1080/10401334.2017.1332631

Ritter, J. (1988). The buying and selling behavior of individual investors at the turn of the year. The Journal of Finance, 43(3), 701–717. https://doi.org/10.1111/J.1540-6261.1988.TB04601.X

Ritter, J. (2003). Behavioral finance. Pacific Basin Finance Journal, 11(4), 429–437. https://doi.org/10.1016/S0927-538X(03)00048-9

Roberts, C., & Henneberry, J. (2007). Exploring office investment decision-making in different European contexts. Journal of Property Investment and Finance, 25(3), 289–305. https://doi.org/10.1108/14635780710746939

Salman, M., Khan, B., Khan, S. Z., & Khan, R. U. (2021). The impact of heuristic availability bias on investment decision-making: Moderated mediation model. Business Strategy and Development, 4(3), 246–257. https://doi.org/10.1002/bsd2.148

Schotten, M., el Aisati, M., Meester, W. J. N., Steiginga, S., & Ross, C. A. (2019). A brief history of Scopus: The world’s largest abstract and citation database of scientific literature. Research Analytics, 31–58. https://doi.org/10.1201/9781315155890-3

Shah, S. Z. A., Ahmad, M., & Mahmood, F. (2018). Heuristic biases in investment decision-making and perceived market efficiency: A survey at the Pakistan stock exchange. Qualitative Research in Financial Markets, 10(1), 85–110. https://doi.org/10.1108/QRFM-04-2017-0033

Shantha Gowri, B., & Ram, V. S. (2019). Does availability bias have influence on FMCG investors? An empirical study on cognitive dissonance, rational behaviour and mental accounting bias. International Journal of Financial Research, 10(4), 68–83. https://doi.org/10.5430/IJFR.V10N4P68

Sharma, A., & Kumar, A. (2019). A review paper on behavioral finance: Study of emerging trends. Qualitative Research in Financial Markets, 12(2), 137–157. https://doi.org/10.1108/QRFM-06-2017-0050

Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425–442. https://doi.org/10.1111/J.1540-6261. 1964.TB02865.X

Slovic, P., & Lichtenstein, S. (1971). Comparison of Bayesian and regression approaches to the study of information processing in judgment. Organizational Behavior and Human Performance, 6(6), 649–744. https://doi.org/10.1016/0030-5073(71)90033-X

Sumantri, M. B. A., Susanti, N., & Yanida, P. (2024). Effect of representativeness bias, availability bias and anchoring bias on investment decisions. Economics and Business Quarterly Reviews, 7(2).

Teng, J. Y., & Tzeng, G. H. (1996). A multiobjective programming approach for selecting non-independent transportation investment alternatives. Transportation Research Part B: Methodological, 30(4), 291–307. https://doi.org/10.1016/0191-2615(95)00032-1

Tin, O. S., & Wee-Siong Hii, J. (2020). The relationship between heuristics behaviour and investment performance on debt securities in Johor. Journal of Arts & Social Sciences, 3(2), 57–74.

Toma, F.-M. (2015). Behavioral biases of the investment decisions of Romanian investors on the Bucharest stock exchange. Procedia Economics and Finance, 32, 200–207. https://doi.org/10.1016/S2212-5671(15)01383-0

Tranfield, D., Denyer, D., & Smart, P. (2003). Towards a methodology for developing evidence-informed management knowledge by means of systematic review. British Journal of Management, 14(3), 207–222. https://doi.org/10.1111/1467-8551.00375

Tversky, A., & Kahneman, D. (1973). Availability: A heuristic for judging frequency and probability. Cognitive Psychology, 5(2), 207–232. https://doi.org/10.1016/0010-0285(73)90033-9

Tversky, A., & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185(4157), 1124–1131.

Van den Steen, E. (2002). Skill or luck? Biases of rational agents. MIT Sloan School of Management. https://dspace.mit.edu/handle/1721.1/1684

Wang, F. A. (2001). Overconfidence, investor sentiment, and evolution. Journal of Financial Intermediation, 10(2), 138–170. https://doi.org/10.1006/JFIN.2001.0311

Waweru, N. M., Munyoki, E., & Uliana, E. (2008). The effects of behavioural factors in investment decision-making: A survey of institutional investors operating at the Nairobi Stock Exchange. International Journal of Business and Emerging Markets, 1(1), 24–41. https://doi.org/10.1504/IJBEM.2008.019243

Yaniv, I. (1997). Weighting and trimming: Heuristics for aggregating judgments under uncertainity. Organizational Behavior and Human Decision Processes, 69(3), 237–249. https://doi.org/10.1006/OBHD.1997.268