Review of Professional Management

Search

Search

Himanshu Bhusan Mishra1 , Tanvi Chawda2, Shibanee Acharya3 and Omkar Acharya3

, Tanvi Chawda2, Shibanee Acharya3 and Omkar Acharya3

1Institute of Management and Information Technology Cuttack, Odisha, India

2Shailabala Women’s (Autonomous) College, Cuttack, Odisha, India

3Department of Law, Fakir Mohan University, Januganj, Balasore, Odisha, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Micro, small and medium enterprises (MSMEs) are an essential element in Odisha’s economic growth and socio-economic progress, providing jobs, fostering rural entrepreneurship and promoting balanced geographical development. But even with the introduction of government reforms and financial inclusion programmes, MSMEs often face challenges in obtaining credit from public sector banks, especially at the pre-sanction stage of loan disbursement. The first step, which includes documentation, eligibility checks and ground evaluation, is a pivotal factor in determining customer satisfaction and trust in the banking system. The current study examines the levels of satisfaction of MSME borrowers at the pre-sanction stage of loan issuance in public sector banks in Odisha. The research aims to determine the impact of demographic and financial factors, such as age, education and loan amount, on borrowers’ perceptions of fairness, efficiency and transparency in the loan process. Using a descriptive–analytical research design, the study collects primary data through a structured questionnaire and interviews with borrowers across various districts of Odisha. Results show that satisfaction levels are not materially different across age groups, education levels and credit limits, suggesting that most public sector banks share a similar attitude towards lending. This consistency highlights the success of digital banking reforms, process automation and rule-based evaluation systems that have reduced procedural bias and increased transparency. The study also indicates that satisfaction levels are increasingly determined by institutional performance indicators, including timeliness, communication quality and the legibility of documentation, but not by borrower demographics. As a result, the research concludes that the model for achieving procedural parity and consistency in pre-sanction loan processes by public sector banks in Odisha indicates an improvement in inclusive banking. Further improvement in satisfaction should focus on qualitative aspects of service delivery, including staff responsiveness, empathy and the efficiency of active communication. MSMEs, as well as public sector banks, can build long-lasting connections and strong trust by further developing digital infrastructure, feedback systems and strategies to engage borrowers.

MSME satisfaction, pre-sanction loan process, public sector banks (India), borrower perception and trust, banking process transparency

Introduction

Micro, small and medium enterprises (MSMEs) comprise a significant portion of India’s economic infrastructure. They contribute approximately 30% to the country’s gross domestic product, 45% to manufacturing and 48% to exports. They also employ more than 110 million individuals. This is also a leading sector in Odisha, with over 4 lakh registered MSME units operating in various industries, including handloom, handicrafts, food processing and mineral-based manufacturing. Although MSMEs in India make a significant contribution to the economy, they face a substantial credit gap, estimated at 20–25 lakh crore, and only 14% of these businesses utilise formal institutional credit. This financial limitation has a significant negative impact on the growth path and competitiveness of such businesses, especially in states such as Odisha, where financial inclusion remains a persistent issue (Ashiq et al., 2023).

In India, funding for MSMEs predominantly relies on public sector banks (PSBs), which provide over 77% of the loans to this sector. By March 2025, the current MSME loan book with PSBs stood at 13.07 lakh crore, an increase of 11.3 year on year. However, a series of challenges have been encountered in the pre-sanction credit appraisal process, which is a bottleneck between MSMEs’ credit demand and supply. The pre-sanction stage is a part of the process that includes submitting the application, conducting due diligence on the borrower, performing a credit check, verifying documents and obtaining preliminary approval. All these combined details indicate the ease, effectiveness and borrower satisfaction with banking services (GOI, Ministry of Finance, 2025).

Recent studies have found that approximately 64% of stressed assets and non-performing accounts originate from failures during the initial pre-sanction borrower due diligence step. The pre-sanction credit process consists of three basic steps: appraisal and recommendation, assessment and sanction. These functions are subdivided by the functional responsibilities of appraisers, assessors and sanctioning authorities. The difficulties associated with this process include incomplete documentation, subjective risk evaluation, the absence of standard procedures, limited access to accurate information about borrowers and time-consuming manual verifications. For MSMEs, this is exacerbated by poor collateral, a lack of organised credit histories, stringent documentation requirements and a perceived higher risk.

Customer satisfaction in the banking industry has proven crucial to institutional performance and competitive advantage, particularly in the highly regulated and competitive MSME lending environment. The quality dimensions of service, such as tangibles, reliability, responsiveness, assurance and empathy, as conceptualised in the SERVQUAL model, fundamentally define satisfaction. In a particular case of MSME lending, the factors of satisfaction do not relate only to the traditional service parameters such as quality but also the timeliness of the decision, the suitability of the loans, the clarity of the processes, its reliability, the presence of online banking services, the conducive conditions of the loans, the competence of the staff and the protection of personal data. It has been established that the service quality dimensions have a strong linear relationship with customer satisfaction, with all correlation coefficients revealing strong relationships between bank policies and procedures and MSME borrower contentment (Jena, 2025).

The shift to digital credit assessment models represents a paradigm shift in lending to MSMEs. The New Digital Credit Assessment Model for MSMEs (initially launched in March 2025) leveraged digitally verifiable data and automated credit decisioning to complete the turnaround in under one day, compared to the more traditional manual methods, which typically took 7–15 working days. The number of MSME loan applications sanctioned by PSBs within this new framework from 1 April to 15 July 2025 is 98,995. This digital revolution encompasses PAN authentication, integration of GST data API, account aggregation, analysis of bank statements, ITR verification and automated fraud detection. Nevertheless, the conversion and application of these technological innovations differ considerably across regions and institutions, and some traditional challenges persist in most work settings (McKinsey & Company, 2025; RBI, 2024).

The MSME sector in Odisha faces unique regional challenges, including inadequate access to finance, infrastructural bottlenecks, outdated technology, market constraints and regulatory burdens. The state government has introduced specific policy reforms through the MSME Development Policy 2022, a part of the Vikshit Odisha vision, to rejuvenate the ecosystem by easing the business environment, providing financial support schemes, improving market access, developing skills and encouraging innovation. Despite such interventions, Odisha’s credit-to-deposit ratio stands at approximately 66, below the national average, indicating that banking resources are not being fully utilised for productive lending. PSBs still dominate the state’s credit environment. Still, there is a paucity of systematic research studying the level of satisfaction among MSME borrowers with pre-sanction processes.

The pre-sanction loan process serves as the entry point for crucial interactions among institutional efficiency, regulatory conformity, technological competency and customer expectations. For MSMEs borrowers, this step not only defines access to credit but also contributes to perceptions of fairness, transparency, speed and institutional trustworthiness. The studies show that customers focus on four main dimensions throughout the loan process, including reassurance from knowledgeable and readily available personnel, a clear understanding of prices and schedules, ease in the application process and paperwork, and speed in processing and decision-making. Banks that excel at getting things right the first time and providing 24 × 7 status updates also go a long way towards increasing borrower satisfaction and loyalty.

Although the literature on the quality of banking services and the problem of MSME financing has continued to grow over time, empirical studies that specifically focus on the pre-sanction loan process satisfaction of MSMEs borrowers in PSBs in Odisha are scarce. The current literature has been more inclined towards post-sanction monitoring, credit performance measurement and macro-level achievement trends. Still, a major knowledge gap exists regarding the determinants of satisfaction at the most crucial pre-sanction stage. The identified research gap is especially crucial, considering that pre-sanction experiences largely shape borrowers’ perceptions, influence their credit uptake choices and define the long-term banking relationships (Swaminathan, 2024).

The lending regulations for MSMEs have undergone significant changes in recent years. Beginning on 1 October 2024, banks were required to disclose clear and understandable information on the terms and costs of loans in a Key Facts Statement, as mandated by the Reserve Bank of India (2025). The reason behind this is to enhance transparency and empower the borrowers. Additionally, the elimination of prepayment penalties on some MSME loans demonstrates a commitment to promoting desirable borrower practices. This article discusses the pre-sanction loan system in state-sponsored banks in Odisha, examining issues such as the system’s performance, transparency, communication, employee competence and reliability to identify what drives borrower satisfaction.

Review of Literature

MSMEs are critical to the economic development of India, particularly in states such as. Odisha, however, has a long-standing discontent with the pre-sanction loan procedures of PSBs. Studies have highlighted that high collateral requirements and a complex nature are among the biggest challenges that MSMEs face. Documentation and low financial literacy, which lower their access to formal credit, increase satisfaction. and banking operations (Divya & Sharma, 2025, 2023; Dubey, 2023; Tambunan et al., 2022). While government programmes, such as the MUDRA scheme, have increased access to credit and enhanced entrepreneurship, they have also created problems. High repayment pressure, inability to understand the process and the need for financial education remain (Chaturvedi & Mishra, 2024, 2023; Dubey, 2023). At the advent of digitalisation, non-banking financial companies (NBFCs) have further increased access, especially in areas previously poorly served, but they face challenges. They include regulatory compliance, high interest rates and inefficiencies in the process (Akang & Udo, 2024; Divya & Sharma, 2025; Tambunan et al., 2022). The literature emphasises streamlining pre-sanction processes to improve financial literacy and leverage technology to enhance MSME satisfaction, ultimately leading to sustainability. In Odisha and other regions, economic growth is a significant concern (Akang & Udo, 2024; Basha et al., 2021; Chaturvedi & Mishra, 2023, 2024; De Carvalho et al., 2021; Divya & Sharma, 2025; Dubey, 2023; Marchelina, 2021; Tambunan et al., 2022; Umami et al., 2024).

There are severe constraints on MSMEs’ access to formal credit from state banks in Odisha and across India, such as high collateral requirement, difficult documentation and long approval processes (Akang & Udo, 2024; Dubey, 2023; Sharma, 2025, 2023; Tambunan et al., 2022). These difficulties are magnified by limited financial literacy and ignorance of existing schemes (Dubey, 2023; Supriyadi et al., 2024 ; Tambunan et al., 2022).

Plans such as the Pradhan Mantri MUDRA Yojana have ensured ease of access to collateral-free loans, particularly for micro and small businesses, and have contributed to the creation of entrepreneurship and job opportunities (Chaturvedi & Mishra, 2024; Dubey, 2023). There is further improvement in digitalisation activity, participation by NBFCs and availability of credit, especially in rural and semi-urban regions (De Carvalho et al., 2021; Divya & Sharma, 2025; Tambunan et al., 2022; Umami et al., 2024). Nevertheless, interest rates are high, regulations are restrictive and better need is required. Problems with process clarity still exist (Akang & Udo, 2024; Chaturvedi & Mishra, 2024; Divya & Sharma, 2025).

Financial literacy is one of the most important factors influencing MSME satisfaction and loan repayment. Studies show that more financially literate MSMEs are more likely to access credit and repay it successfully and vice versa. Compliance with regulations may raise operational costs and discourage lending (Akang & Udo, 2024; Dubey, 2023; Supriyadi et al., 2024).

Alternative sources of finance, including NBFCs, credit cooperatives and online lending systems, have emerged. Significant lending options to MSMEs, where traditional banking institutions are not in a position or willing to lend (Da Silva et al., 2024; Dubey, 2023; Divya et al., 2018; Mckillop et al., 2020; Sharma, 2025; Tambunan et al., 2022), can be less strict in terms, yet they can be more risky or even more expensive.

The literature continues to identify that satisfaction with pre-sanction loan procedures among MSMEs in the Odisha public sector is low. Procedural complexity, poor transparency and financial literacy hinder banks (Akang & Udo, 2024; Dubey, 2023; Sharma, 2025, 2023; Tambunan et al., 2022). Although government initiatives, such as those based on MUDRA and digitalisation, have helped people access more, they have never fully addressed the causes of these issues, such as discontent, that is, excessive collateralisation and lengthy processing time (Dubey, 2023; Chaturvedi & Mishra, 2024; Tambunan et al., 2022). The contributions of NBFCs and alternative lenders have helped close some gaps, but such solutions tend to be more expensive or carry higher regulatory risks (Da Silva et al., 2024; Divya & Sharma, 2025; McKillop et al., 2020; Tambunan et al., 2022).

The research quality in the field is generally high, and a variety of empirical studies and literature reviews provide the necessary information and robust evidence. Nevertheless, further region-specific and primary research is required to be performed in Odisha. Learn the local peculiarities and adjust interventions accordingly (Dubey, 2023). The importance of financial reforms in literacy and regulation is mostly supported, so the policy should focus on simplification procedures, improving transparency and offering specific financial education to MSMEs (Akang & Udo, 2024; Dubey, 2023; Supriyadi et al., 2024).

In Odisha, MSMEs’ satisfaction with the pre-sanction loan procedures of PSBs is moderate to low. Even with government scheme ameliorations and digitalisation, there are consistent obstacles, such as procedural complexity, collateral requirements and low financial literacy. Overcoming such challenges through regulation, simplifying processes, providing targeted financial education and implementing reforms are necessary to increase MSME satisfaction and support economic growth.

MSMEs are the lifeblood of Odisha’s local economy, creating jobs and supporting rural entrepreneurship. Yet, one of their biggest challenges is getting fair and timely access to finance. PSBs are intended to support these businesses. Still, MSME owners often describe the pre-sanction loan stage as involving lengthy document checks, eligibility assessments and field inspections, which they find confusing, time-consuming or discouraging. This stage can make or break their trust in the banking system. A human-centred analysis reveals that satisfaction is not only about getting the loan approved but also about how MSME owners feel during the process: whether they are respected, informed and treated fairly. While many studies discuss post-loan satisfaction or repayment behaviour, very few explore emotional experiences, trust and satisfaction before loan sanction, particularly in Odisha.

Despite government schemes and banking reforms, MSMEs in Odisha continue to face difficulties in securing credit from PSBs. Many MSMEs report long waiting periods, lack of communication, unclear documentation requirements and procedural rigidity during the pre-sanction stage. These experiences often lead to emotional stress, business delays and even loan rejections. There is a pressing need to understand how MSMEs perceive these interactions and what specific actions can enhance satisfaction and trust.

Research Gap

Most current research in India emphasises credit availability and financial inclusion rather than pre-sanction happiness. Limited research highlights the qualitative, emotional and experiential aspects of interactions between MSMEs and bankers. There is a paucity of region-specific information about Odisha, despite its burgeoning MSME sector and dependence on PSBs. Research on process enhancement and customer empathy in loan evaluation remains underdeveloped. Hence, there is a clear gap in understanding the human experience of MSME clients during the pre-sanction stages in PSBs, and how satisfaction at this stage can influence broader trust and financial inclusion outcomes.

Objective of the Study

This study aims to evaluate the level of satisfaction of MSMEs during the pre-sanction stage of loan approval in PSBs in Odisha.

Hypotheses

To test whether the demographic and financial characteristics of MSME borrowers (age, education and credit limit) significantly influence their satisfaction levels with pre-sanction loan processes in Odisha’s PSBs.

H1: There is a significant difference in MSME borrowers’ satisfaction with the determinants of the pre-sanction loan process in PSBs in Odisha across different age groups.

H2: There is a significant difference in MSME borrowers’ satisfaction with the determinants of the pre-sanction loan process in PSBs in Odisha across different education levels.

H3: There is a significant difference in MSME borrowers’ satisfaction towards determinants of the pre-sanction loan process in PSBs in Odisha across different credit limit categories.

Research Methodology

Significance of the Study

This study aims to explore and understand how MSMEs in Odisha experience the pre-sanction stage of bank loans in PSBs.

By focusing on borrowers’ satisfaction during this crucial phase, the research brings human perspectives into a largely technical process, revealing what truly matters to small entrepreneurs when they seek credit. The insights from this study can help PSBs improve their service delivery, enhance trust and design MSME-friendly loan systems.

Data Sources and Sample Size

The researchers used purposive sampling to ensure that participants had relevant and recent exposure to the process. The team selected respondents based on their recent experience with the loan application and sanction process in PSBs. The study includes primary data collected from 206 MSME borrowers across various districts in Odisha.

Data Collection Method

Data were collected through a structured questionnaire complemented by personal interviews. The questionnaire covered key areas that influence satisfaction, including the timeliness of decision-making, procedural clarity, services, reliability and charges. Primary data came from MSME borrowers. This study’s population comprises MSME borrowers of PSBs in Odisha. Secondary data were obtained from RBI reports, government policy documents and bank annual reports.

Variable Measurements

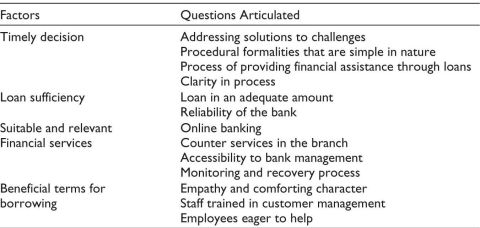

The dependent variables, that is, borrower satisfaction, were measured on a five-point Likert scale, ranging from highly dissatisfied (1) to highly satisfied (5). Independent variables included age (young/middle aged/senior), education (higher secondary/graduation/postgraduate or above) and credit limits (below 20 lakh/20–100 lakh/above 100 lakh). Researchers developed all variables based on prior MSME credit literature and customised them to the context of Odisha’s public sector banking landscape (Table 1 and Table 2).

Table 1. Elements of MSME Borrowers’ Pre-stage of Loan Sanction and the Questions.

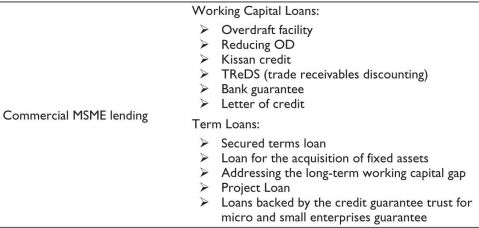

Table 2. MSME Bank Credit Landscape in India.

Research Design

This study employs a descriptive–analytical research design. It aims to describe the level of satisfaction among MSME borrowers and identify the underlying factors influencing their experience during the pre-sanction phase.

Results and Discussion

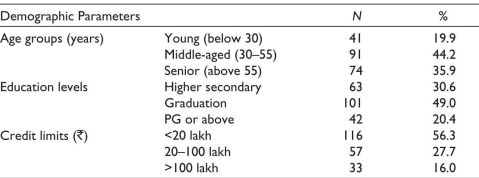

Table 3 and Figure 1 present the demographic profile of MSME borrowers who obtained credit from PSBs in Odisha. A majority of respondents were middle-aged (44.2%), followed by senior entrepreneurs aged 55 or older (35.9%) and young borrowers aged 30 or younger (19.9%). Educationally, 49% were graduates, 30.6% had completed higher secondary education, and 20.4% held postgraduate or higher qualifications. Regarding loan sizes, most MSMEs (56.3%) availed credit below .png) 20 lakh, indicating that micro and small enterprises dominate the credit landscape. This demographic structure aligns with observations by Panda and Dash (2023), who found that micro-enterprises in eastern India are composed mainly of middle-aged entrepreneurs with moderate educational backgrounds. Similarly, Singh and Ghosh (2022) emphasised that MSMEs in semi-urban Odisha rely heavily on small credit segments due to limited collateral and procedural constraints.

20 lakh, indicating that micro and small enterprises dominate the credit landscape. This demographic structure aligns with observations by Panda and Dash (2023), who found that micro-enterprises in eastern India are composed mainly of middle-aged entrepreneurs with moderate educational backgrounds. Similarly, Singh and Ghosh (2022) emphasised that MSMEs in semi-urban Odisha rely heavily on small credit segments due to limited collateral and procedural constraints.

Table 3. Distribution of Sample MSMEs Availing Credit Facilities from PSBs in Odisha.

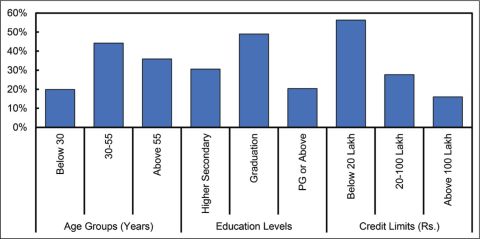

Figure 1. Distribution of Sample MSMEs Availing Credit Facilities from PSBs in Odisha.

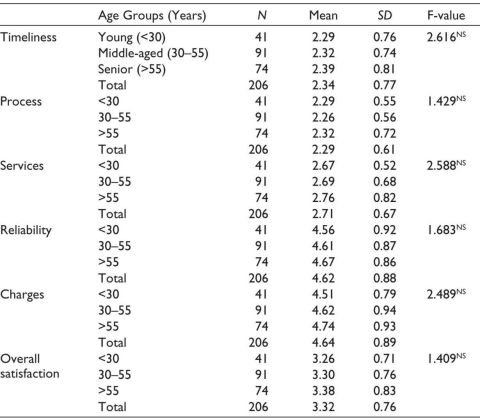

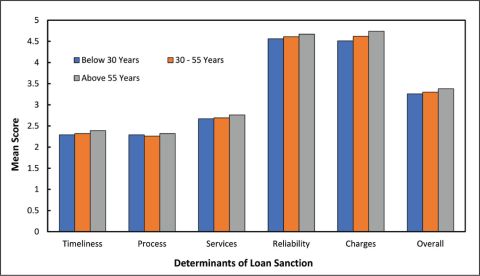

Table 4 and Figure 2 analyses satisfaction differences across age groups using ANOVA. The F-values for all determinants—timeliness, process, services, reliability, charges and overall satisfaction—were statistically non-significant (p > .05). This suggests that age does not significantly impact MSME borrowers’ satisfaction levels with pre-sanction processes in PSBs. Although the mean values show minor variation, senior borrowers report slightly higher satisfaction (overall mean = 3.38); these differences are not large enough to be statistically meaningful. Thus, H1 is not supported. This uniformity suggests that procedural experiences during loan appraisal and sanction are broadly standardised across age categories. The result corroborates the findings of Kumar and Patel (2021), who reported that digitised loan processing in Indian PSBs reduces age-based biases. Similarly, Rout and Sahoo (2022) noted that uniform loan documentation and KYC norms have streamlined the borrower experience, minimising demographic disparities. While age does not significantly affect satisfaction, educational attainment often shapes perceptions and understanding of loan processes. Hence, the next section examines differences across education levels.

Table 4. Mean, SD and F-values of Satisfaction Levels of MSMEs Across Age Groups for Various Determinants at Pre-stage Loan Sanction by PSBs in Odisha.

Note: F-value in ANOVA Between Age Groups. NS: Not significant at the 5% level (p < .05).

Figure 2. Mean Satisfaction Levels of MSMEs Across Age Groups for Various Determinants of Pre-stage Loan Sanction by PSBs in Odisha.

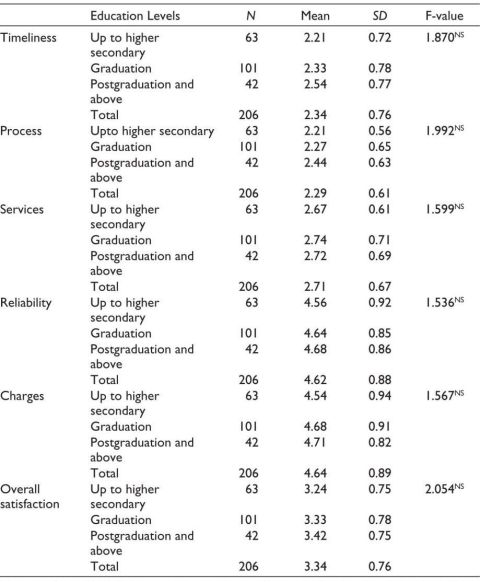

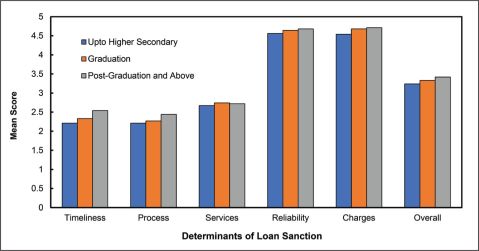

Table 5 and Figure 3 compare the satisfaction levels across borrowers’ educational backgrounds. The mean scores show a gradual increase from those with higher secondary education (mean = 3.24) to those with postgraduate degrees (mean = 3.42). However, the F-values across determinants are all non-significant (p > .05), indicating that educational level does not significantly impact satisfaction with pre-sanction processes. Hence, H2 is also not supported. The pattern implies that the communication and procedural standards of PSBs are generally clear and uniform, irrespective of educational differences. These findings align with those of Das and Behera (2021), who observed that MSME borrowers perceive pre-sanction interactions as highly standardised due to the improved transparency and simplified documentation introduced under the PSB loans in 59 minutes initiative. Likewise, Chakraborty and Roy (2023) reported that even borrowers with limited financial literacy are now better equipped to engage with credit institutions due to digital awareness drives. Although educational and age differences are statistically insignificant, the magnitude of credit availed may influence expectations and perceptions of service quality. Therefore, the analysis proceeds to test H3.

Table 5. Mean, SD and F-values of Satisfaction Levels of MSME Borrowers Across Education Levels for Various Determinants of Pre-stage Loan Sanction by PSBs in Odisha.

Note: F-value in ANOVA between education levels. NS: Not significant at the 5% level (p < .05).

Figure 3. Mean Satisfaction Levels of MSME Borrowers Across Education Levels for Various Determinants of Pre-stage Loan Sanction by PSBs in Odisha.

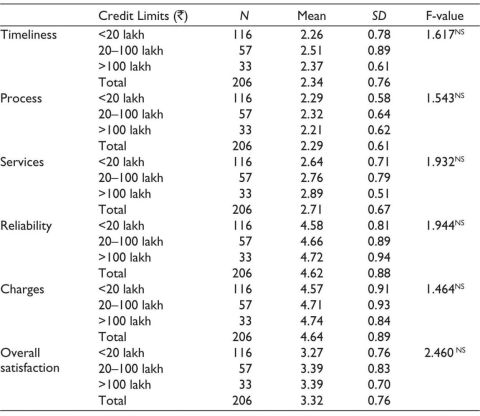

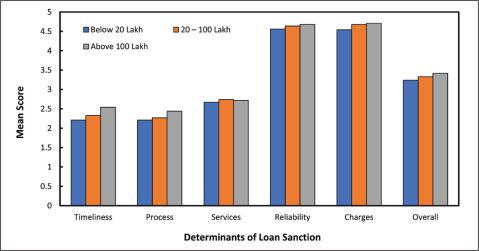

The data in Table 6 and Figure 4 show that MSME borrowers with higher credit limits (> 100 lakh) reported marginally higher satisfaction (mean = 3.39) than those with lower credit limits (< 20 lakh; mean = 3.27). However, as indicated by the non-significant F-values (p > .05) across all determinants, these variations are not statistically significant. Thus, H3 is rejected. This consistency implies that PSBs maintain a relatively standardised approach to MSME clients, irrespective of the size of the sanctioned loan. Larger loan seekers do not necessarily receive superior service quality, as this is often reflected in a uniform credit evaluation system. Narayan and Singh (2024) observed similar results, suggesting that digital underwriting frameworks have reduced preferential treatment based on loan size. Moreover, Mishra et al. (2022) highlighted that the RBI’s standardisation guidelines for MSME lending have reduced procedural asymmetry between small and large credit applicants.

Table 6. Mean, SD and F-values of Satisfaction Levels of MSME Borrowers across Credit Limits for Various Determinants of Pre-stage Loan Sanction by PSBs in Odisha.

Note: F-value in ANOVA Between Credit Limits. NS: Not significant at the 5% level (p < .05).

Figure 4. Mean Satisfaction Levels of MSME Borrowers Across Credit Limits for Various Determinants of Pre-stage Loan Sanction by PSBs in Odisha.

The statistical findings collectively indicate that demographic and financial differences among MSME borrowers, including age, education and credit limit, do not significantly influence satisfaction levels with pre-sanction loan processes in Odisha’s PSBs. This may reflect the banks’ adoption of uniform evaluation systems, online application portals, and rule-based verification frameworks that ensure consistency in service delivery. This result aligns with recent studies that emphasise process uniformity and procedural transparency as key achievements of financial reforms. Kaur and Sharma (2023) and Gupta (2022) noted that digitisation and MSME-focused lending schemes have improved borrowers’ experiences by minimising subjectivity and bureaucratic discretion. Furthermore, Behera and Panda (2023) observed that satisfaction with MSME credit services is now more influenced by institutional performance (e.g., timeliness and communication efficiency) than by borrower demographics. From a policy standpoint, the findings underscore the need for further qualitative exploration of factors beyond demographics, such as staff responsiveness, documentation clarity and post-sanction follow-up, that may influence borrower satisfaction. The non-significance across all hypotheses underscores that procedural equality has largely been achieved in the pre-sanction phase, reflecting commendable progress in public sector banking reforms in Odisha.

Conclusions

The study’s findings indicate that PSBs in Odisha have achieved a high level of procedural uniformity in the pre-sanction phase of MSME loan processing. Borrowers’ satisfaction levels do not differ significantly by age, education or credit size, suggesting that banks follow standardised systems that treat all applicants similarly. This reflects consistent application of policies, digital frameworks and rule-based assessment methods that minimise personal bias and demographic influence. The results further imply that reforms in digital lending, such as online application portals and automated evaluation tools, have enhanced procedural transparency and fairness. Borrowers from diverse backgrounds experience comparable levels of satisfaction, indicating the successful implementation of inclusive and efficient lending practices. Although demographic variables do not have a significant effect on satisfaction, this uniformity highlights the maturity of operational processes in PSBs. It also suggests that borrowers’ satisfaction is now shaped more by the quality of institutional performance, such as timeliness, communication and clarity of documentation, than by personal characteristics. From a policy and managerial perspective, the study underscores that the next stage of improvement should focus on service delivery dimensions rather than demographic targeting. Strengthening staff responsiveness, improving documentation clarity and ensuring proactive communication could further elevate MSME satisfaction. Overall, the research concludes that Odisha’s PSBs have established equitable and standardised pre-sanction loan processes, reflecting meaningful progress in MSME-oriented banking reforms.

Policy Implications

In summary, the statistical uniformity in satisfaction outcomes underscores that Odisha’s PSBs have successfully minimised demographic disparities in loan sanctioning. Future policies should shift from standardisation towards service enhancement, focusing on responsiveness, effective communication and continuous improvement mechanisms.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iDs

Himanshu Bhusan Mishra https://orcid.org/0000-0002-8623-9076

Shibanee Acharya https://orcid.org/0000-0002-5175-6321

Akang, A., & Udo. (2024). Regulatory compliance and access to finance: Implications for business growth in developing economies. Sciental Journal of Education, Humanities and Social Sciences, 1(2), 8–23. https://doi.org/10.62536/sjehss.2023.v1.i2.pp8-23

Ashiq, M., Rubab, N., Hussain, S., & Asad, M. (2023). Customer loyalty in banking: A comprehensive review. Journal of Business Research, 157, 112–125.

Basha, S., Elgammal, M., & Abuzayed, B.(2021). Online peer-to-peer lending: A review of the literature. Electronic Commerce Research and Applications, 48, 101069. https://doi.org/10/1016/je.elerap.2021/101069

Behera, A., & Panda, S. (2023). Digital lending transformation and MSME financing in Eastern India. Indian Journal of Finance and Banking, 12(3), 88–101.

Chakraborty, T., & Roy, P. (2023). Financial literacy and MSME satisfaction: Evidence from eastern India. Asia-Pacific Journal of Business Administration, 15(2), 211–229.

Chaturvedi, A., & Mishra, S. (2024). A comprehensive review of MUDRA loan scheme: Implications for MSME development. Smart Moves Journal Ijoscience, 9(10). https://doi.org/10.24113/ijoscience.v9i10.483

Da Silva, Y., Temu, T., & Lamawitak, P. (2024). Knowledge management-based efforts to improve MSME performance (credit union intervention for MSME actors in Sikka Regency). Dinasti International Journal of Education Management and Social Science. https://doi.org/10.38035/dijemss.v5i4.2454

Das, P., & Behera, R. (2021). Pre-sanction credit assessment in Indian PSBs: A borrower perspective. Journal of Small Business and Enterprise Development, 28(7), 1104–1123.

De Carvalho, G., Resende, L., Pontes, J., De Carvalho, H., & Betim, L. (2021). Innovation and management in MSMEs: A literature review of highly cited papers. SAGE Open, 11. https://doi.org/10.1177/21582440211052555

Divya, & Sharma, S. (2025). Role of NBFCs on MSME financing: A special reference of credit accessibility and economic growth. International Journal of Business Ethics in Developing Economies. https://doi.org/10.21863/ijbede/2025.14.1.001

Dubey, S. (2023). Financing of small-scale industries in India: A survey of literature. International Journal for Research in Applied Science and Engineering Technology. https://doi.org/10.22214/ijraset.2023.53750

Government of India, Ministry of Finance. (2025, July 28). Public sector banks’ MSME bad loans falling. Press Information Bureau. https://pib.gov.in/

Gupta, R. (2022). Evaluating service quality in MSME banking: A comparative study of public and private banks. Journal of Business Studies Quarterly, 13(2), 33–49.

Jena, B. K. (2025). An analytical study of MSME financing in Odisha, India. Journal of Management and Science Research, 8(2), 156–178.

Kaur, J., & Sharma, N. (2023). Impact of digital banking on MSME loan satisfaction in India. International Journal of Management Studies, 10(1), 45–60.

Kumar, V., & Patel, R. (2021). Standardization of MSME credit evaluation in public sector banks. Journal of Banking and Finance Research, 9(4), 122–136.

McKinsey & Company. (2025, August 10). Why the future of MSME banking is digital. https://www.mckinsey.com/

Mckillop, D., French, D., Quinn, B., Sobiech, A., & Wilson, J. (2020). Cooperative financial institutions: A review of the literature. International Review of Financial Analysis, 71, 101520. https://doi.org/10.1016/j.irfa.2020.101520

Mishra, S., Reddy, D., & Mohanty, P. (2022). Regulatory influence on MSME credit process efficiency in India. South Asian Journal of Business and Economics, 11(3), 77–91.

Narayan, M., & Singh, P. (2024). Credit limit and satisfaction asymmetry in MSME banking. Asian Journal of Economics and Business Research, 19(2), 55–70.

Panda, R., & Dash, S. (2023). Age and experience dimensions in MSME entrepreneurship in Odisha. Journal of Rural Management Studies, 7(2), 61–74.

Reserve Bank of India. (2025, February 21). Reserve Bank of India (prepayment charges on loans) directions, 2025.

Reserve Bank of India. (2025, March 24). Master directions: Reserve Bank of India (priority sector lending – targets and classification) directions, 2025.

Rout, S., & Sahoo, B. (2022). Borrower satisfaction in MSME finance: An empirical analysis of public sector banks. Indian Banking Review, 15(1), 39–54.

Supriyadi, A., Saifi, M., & Np, M. (2024). The effect of financial literacy on loan repayment performance of MSMEs: A literature review. KnE Social Sciences. https://doi.org/10.18502/kss.v9i11.15779

Swaminathan, J. (2024, November 16). MSMEs: Bridging the credit gap through improving confidence in lending. Federation of Telangana Chambers of Commerce and Industry CEO Forum, Hyderabad. Bank for International Settlements. https://www.bis.org/

Tambunan, E., Enuh, K., Ubaidullah, U., & Tamba, M. (2022). Capital access for micro small medium enterprises. Jurnal Ekonomi dan Perbankan Syariah. https://doi.org/10.46899/jeps.v10i2.375

Umami, I., Pee, A., Sulaiman, H., & Mar’ati, F. (2024). A literature review of MSME success: Acceptance and use of technology, financial access, and strategic cooperation. Multidisciplinary Reviews, 6, 2023ss086. https://doi.org/10.31893/multirev.2023ss086