Review of Professional Management

Search

Search

Jayshree Roongta1  and Jaivardhan Roongta2

and Jaivardhan Roongta2

1 The Heritage College, Kolkata, West Bengal, India

2 St. Xavier’s College (Autonomous), Kolkata, West Bengal, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Sustainability consciousness has grown incrementally on a global front. Organisations are striving to include all aspects of sustainability in their business contexts. This research investigates Indian banks’ environmental sustainability strategies, with an emphasis on environmental reporting. Using a sample of 30 public and private sector banks in a longitudinal study, descriptive and exploratory research approaches, and statistical techniques such as descriptive statistics and inferential statistics, the research evaluated their environmental initiatives across 42 key indicators divided into five major categories. According to the analysis, private banks perform better in terms of reporting and are more proactive in environmental management. None of the banks covered every indicator. The recommendations include regulatory assistance, capacity building activities and a tracking mechanism to promote accountability and transparency. This study emphasises the relevance of environmental reporting in establishing sustainable banking practices and provides insights for policymakers, regulators and financial institutions to move forward.

Environmental reporting, environmental sustainability, financial sector, Indian banking sector, sustainable development

Introduction

The word ‘sustainability’ is used everywhere around the world as it is all around us. Protecting the environment has become the top priority for individuals, organisations and society as a whole to prevent human destruction of our planet (Appiah et al., 2019). The concept of sustainable development has been evolving over the years. This moving target has gone across societies, organisations and industries. It has even reached the banking sector and taken the form of ‘sustainable banking’. As banks are the backbone of an economy, they guide the economic players towards sustainable development (Nizam et al., 2019).

Sustainable development aims to meet the needs of both present and future generations by integrating sustainability into decision-making (Fischer et al., 2023). Increasing individual benefits and national economic growth are the goals of the economic component of sustainable development. Giving everyone in society equal access to resources that will improve their well-being is the goal of the social dimension. Preserving natural resources for the current generation without compromising the demands of future generations is the focus of the environmental dimension. It is based on the idea of balancing ecosystem capacity and human needs. But achieving progress in all areas while balancing complexity is the ultimate goal of sustainable development.

The concept of sustainable development has been evolving over the years. It has spread across societies, organisations and industries. It has even reached the banking sector and is now known as ‘sustainable banking’. As banks are the backbone of an economy, they play a key role in guiding the economic players towards sustainable development (Nizam et al., 2019).

To achieve sustainability in the financial sector, banking institutions have gone through four stages. Sustainable banking has evolved from defensive to offensive banking, excluding the first layer of preventive banking. Primarily, banking institutions have moved from the inner layer to the outermost layer. The first layer is defensive banking. As banking institutions are profit-making organisations, they are reluctant to follow environmental laws for fear of incurring losses. In this stage, they consider environmental management as an additional cost to the institution (Deegan & Gordon, 1996) and irrelevant to performance. The second layer is preventive banking. At this stage, banking institutions will work on their internal processes and actively integrate environmental management and risk assessment into their core business activities. The shift in objective is due to externalities that include government institutions, NGOs and potential investors who pressure banking institutions to address environmental issues. The next layer is offensive banking. This stage considers activities that promote environmental sustainability in the financial sector. Here, banks fund environmentally friendly projects, develop green products and services and report on their environmental initiatives to get social licence (Chakroun et al., 2017; Day & Woodward, 2009). Finally, the outermost layer is green banking. At this point, the bank does not look for higher returns; it looks for steady returns. A green bank will fund projects with higher risks, lower returns and longer payback periods. But lately the concept of green banking has emerged on the back of the environmental, social and governance (ESG) framework that promotes sustainable development in the banking sector.

With sustainability growing in all organisations, it adds incremental liability and responsibility on the backbone of the economy—the banking sector to get on the sustainability bandwagon. Thus, a study on banks’ practices on environmental sustainability and reporting becomes essential as it will give an insight into the current state and provide actionable recommendations to create a greater impact.

Literature Review

Corporate environmental reporting has been in the spotlight for almost three decades now. Since the early 1990s, Indian corporates were facing competition from global corporates who were setting up shop in India. These global corporates were reporting their corporate social responsibility (CSR) activities, including environmental initiatives. This led to stakeholders’ expectations from Indian corporates to report their information to be accountable to society. So, to be accountable to stakeholders and society at large, Indian corporates started reporting their environmental activities in their annual reports, websites, newsletters, etc.

In India, corporate environmental reporting procedures are still in their infancy (Sahay, 2004). It was discovered that reporting procedures were insufficient, disorganised and fragmented. Indian chartered accountants believed that in order to increase the credibility of their reports, Indian corporations should create environmental reports that are validated by an outside group of certified environmental auditors (Pahuja, 2007). Furthermore, the majority of Indian corporations were simply posting mandatory environmental documentation, according to an examination of an environmental information audit. According to Chatterjee and Mir (2008), Indian businesses were revealing more environmental information on their websites than in their yearly reports. Furthermore, the study discovered that none of the sample firms reported negative information on environmental issues; instead, they solely reported neutral and positive information. Nonetheless, it was discovered that the disclosure was descriptive and narrative in character (Prasad et al., 2016; Sen et al., 2011). Previous empirical research has revealed variations in environmental reporting within Indian sectors, underscoring the fact that procedures differed both within and between Indian industries (Kumar et al., 2015; Prasad et al., 2016). Additionally, it was shown that there are variations among sectors regarding the more general aspect of sustainability reporting. However, the kind of business tasks carried out by these corporates can be a critical factor in explaining the significant differences in reporting across corporates of different sectors. Indian companies are just starting to adopt global reporting indicators (GRI) (Goel & Misra, 2017). Companies that use GRI indicators disclose more on sustainability than those that don’t (Kumar, 2020). Since GRI reporting companies are doing better, Indian companies should adopt sustainable codes of conduct such as SDGs, UNGC principles and GRI to improve their sustainability reporting (Hossain & Reaz, 2007). The reporting guidelines of Companies Act 2013 and SEBI guidelines are responsible for the growing trend of environmental reporting (Prasad et al., 2016; Kumar et al., 2022; Yadav & Sinha, 2021). After the Companies Act 2013 was amended, which made it mandatory for the companies listed on BSE and NSE to publish, the quality and quantity of corporate environmental reporting by Indian entities has increased.

Earlier research has shown that public sector companies reported on environmental issues more than private sector companies (Pahuja, 2009). Compared to private sector companies in India, government companies disclose more sustainability information in their annual reports. Also, it was found that bigger polluting companies disclosed more environmental information than smaller ones (Pahuja, 2007). Several studies have looked into the variables affecting Indian companies’ socio-environmental reporting practices as per the literature (Chandok & Singh, 2017; Nurhayati et al., 2016). According to Sandhu et al. (2012), corporate environmental responsiveness in Indian organisations is a two-order construct. Pressure from the company’s internationalisation efforts and supply chain clients drives level one responsiveness, while the institution’s cultural foundation and value system, which has its roots in the history of social responsiveness, is responsible for level 2 responsiveness. In India, the size of the audit committee, brand development and company size affect social and environmental reporting (Nurhayati et al., 2016). Also, it was found that age and company size had a positive impact on Indian companies’ environmental reporting (Chandok & Singh, 2017). But this study found that a company’s success and leverage had a negative impact on its environmental reporting. In India, the degree of sustainability reporting is positively affected by board size, board meetings and government ownership (Kumar et al., 2022). But there is a negative correlation between sustainability reporting and the percentage of independent directors.

Environmental reporting is limited in India, especially in the banking sector. As per Kumar et al. (2017), Indian financial institutions are gradually moving towards sustainability reporting, which includes social, environmental and economic factors. As per GRI guidelines, the sustainability reporting of top Indian banks was studied. The findings show that sustainability disclosure is not fully adopted by Indian banks. Though they report on environmental measures, they do not address many important aspects such as GHG emissions, climate change policies, etc. Indian banks are still in the early stages of sustainability, as per earlier studies. The Indian banking sector has been slower to respond to sustainability challenges (Kumar & Prakash, 2019). As per research, Indian banks are just starting to disclose their environmental activities, which are heavily dependent on their green technology. A study on 42 Indian commercial banks’ sustainability reporting policy supported the above conclusions by showing that Indian banks are still in early stages of disclosing their environmental activities. Though most Indian banks have adopted green banking initiatives such as green products, green funding and green innovation processes, they are still in early stages of these programmes. Public and private sector banks in India report on the environment differently (Sharma & Choubey, 2021).

Research Gap

Environmental reporting has gained critical significance across the globe (K.png) lç & Kuzey, 2019). Institutions globally have been reporting in great detail in their annual reports about their environmental activities. Meanwhile, these reporting organisations get a lot out of telling their stakeholders about their financial and non-financial data. As per research, reporting improves an institution’s long-term financial performance (Agostini et al., 2021; Chouaibi et al., 2021; Radhouane et al., 2018). Additionally, these strategies have been shown to improve institutions’ reputations over time (Agyei & Yankey, 2019). They assist them in creating distinctive assets that are essential for obtaining a competitive advantage in the marketplace (Banker et al., 2014). Furthermore, by significantly reducing the input–output costs related to company operations, these methods increase an institution’s operational efficiency (Biswas & O’Grady, 2016). Furthermore, institutional investors protect business institutions from unfavourable market conditions since they take into account both the financial and non-financial performance of institutions when making investment decisions (Godfrey, 2005; Ye & Zhang, 2011). Nevertheless, even if reporting procedures incur additional expenses, a number of organisations use them to align their operations with social norms, values and beliefs (Tilt, 2006) and to justify their activities to the public. More significantly, it gives its stakeholders confidence and fosters a feeling of trust in the organisation. Given this, it is essential to address this area of study, which has significant advantages for a variety of stakeholder groups, including consumers, workers, government agencies, corporate organisations and the general public. However, following SEBI’s rules on required disclosure requirements for listed financial institutions, Indian banks have also been aggressively disclosing their environmental projects and practices. It is essential to assess Indian financial organisations’ contributions to the environment and society in light of the growing significance of environmental reporting.

lç & Kuzey, 2019). Institutions globally have been reporting in great detail in their annual reports about their environmental activities. Meanwhile, these reporting organisations get a lot out of telling their stakeholders about their financial and non-financial data. As per research, reporting improves an institution’s long-term financial performance (Agostini et al., 2021; Chouaibi et al., 2021; Radhouane et al., 2018). Additionally, these strategies have been shown to improve institutions’ reputations over time (Agyei & Yankey, 2019). They assist them in creating distinctive assets that are essential for obtaining a competitive advantage in the marketplace (Banker et al., 2014). Furthermore, by significantly reducing the input–output costs related to company operations, these methods increase an institution’s operational efficiency (Biswas & O’Grady, 2016). Furthermore, institutional investors protect business institutions from unfavourable market conditions since they take into account both the financial and non-financial performance of institutions when making investment decisions (Godfrey, 2005; Ye & Zhang, 2011). Nevertheless, even if reporting procedures incur additional expenses, a number of organisations use them to align their operations with social norms, values and beliefs (Tilt, 2006) and to justify their activities to the public. More significantly, it gives its stakeholders confidence and fosters a feeling of trust in the organisation. Given this, it is essential to address this area of study, which has significant advantages for a variety of stakeholder groups, including consumers, workers, government agencies, corporate organisations and the general public. However, following SEBI’s rules on required disclosure requirements for listed financial institutions, Indian banks have also been aggressively disclosing their environmental projects and practices. It is essential to assess Indian financial organisations’ contributions to the environment and society in light of the growing significance of environmental reporting.

Theoretical Background of the Study

Legitimacy Theory

According to legitimacy theory, institutions have to be in line with societal norms, values and beliefs to be socially accepted. It says organisations and society have a social contract that requires them to uphold moral principles and promote the well-being of society. Institutions use environmental reporting to uphold their legitimacy and address social attitudes and legal requirements. Legitimacy can be achieved through institutional practices (e.g., following industry standards and laws) or strategic activities (e.g., responding to public awareness or legal pressure). Some organisations use symbolic measures to influence stakeholder views, while others take concrete steps to close the legitimacy gap. Environmental reporting has become a way for banks to show their legitimacy and commitment to sustainability. According to the theory, organisations highlight positive information to support their reputation and use environmental disclosure to keep good relations with society.

Stakeholder Theory

Freeman proposed the stakeholder theory in 1984. It states that businesses should consider the interests of all the groups that influence or are affected by their choices, not only those that maximise profits but also non-stockholder organisations such as the environment and local communities. With stakeholders pressuring institutions to address environmental challenges, this has gradually come into line with sustainability. In order to improve a company’s reputation, increase its worth and draw in investors and clients that respect CSR, stakeholder engagement includes accountability, transparency and environmental performance reporting. Institutions are also under pressure from governments and regulatory agencies to practice environmental responsibility. Meeting stakeholder needs is the focus of stakeholder theory.

Objectives of the Study

The study has the following two objectives:

Research Methods

The present research is a longitudinal study for a 10-year consecutive time period of 2014–2024. It is a quantitative study. The sample consists of 30 Indian banks: 12 public sector banks and 18 private sector banks. The study is based on secondary data. The required data were obtained through various sources, inclusive of annual reports, sustainability reports and business responsibility reports of the concerned banks. Tools and techniques for the analysis include extensive content analysis, descriptive statistics and inferential statistics as Levene’s test for equality of variance and t-test for equality of means.

For the 30 selected banks, public sector banks include State Bank of India, Punjab National Bank, Bank of Baroda, Canara Bank, Union Bank, Bank of India, Indian Bank, Central Bank of India, Indian Overseas Bank, UCO Bank, Bank of Maharashtra, Punjab and Sind Bank. Private sector banks include HDFC Bank, ICICI Bank, Kotak Mahindra Bank, Axis Bank, IndusInd Bank, Yes Bank, IDFC First Bank, Federal Bank, South Indian Bank, RBL Bank, Bandhan Bank, CSB Bank, IDBI Bank, Karur Vysya Bank, City Union Bank, Dhanlaxmi Bank, Karnataka Bank and Tamilnad Mercantile Bank.

Extensive literature review yielded the following 42 environmental parameters upon which the banks were extensively evaluated and compared: Evaluation of GHG emission, Initiatives to save fuel consumption, Adoption of tools to reduce air pollution/carbon footprint, Targets to reduce emissions and control air pollution, Initiatives to reduce and recycle material/paper usage, Waste disposal mechanism, Installation of waste recycling units, Targets to reduce waste generation, Installation of water recycling units, Adoption of water conservation tools, Information on units of water saved, Targets to reduce water consumption, Use of alternative/renewable sources of energy, Installation of energy-efficient systems/tools/equipment, Information on units of energy saved, Targets to reduce energy consumption, Tree plantation/afforestation activities initiatives, Initiatives/programmes to restore the ecology, Environmental policy, Environmental risk management system, Adoption of environmental risk management strategies/tool, Identification/evaluation of climate-related risk, Financing renewable energy projects, Financing green projects, Investments in environmental-related research and developmental activities, Investments in green technology, Maintenance of an exclusion list, Inclusion of environmental aspect in the bank’s lending policy, Information on the amount saved from environmental initiatives, Adoption of digital communication channels, Adoption of green technology, Provision of internet and mobile banking apps, Certification for environmental management system, Environmental compliance agreements, Signatory to environmental principles/standards, Awards for environmental practices and initiatives, Presence of environmental departments, councils and committees, Environmental awareness programmes, Environmental training programmes for bank employees, Environmental promotional activities, Presence of an internal/external environmental audit and Delivery of green products and services.

Environmental risk management, environmental finance, environmental compliance, environment management initiatives and practices and environment-related policies are the five domains into which the parameters were logically divided.

Analysis and Discussion

Environmental Reporting Score of Selected Banks: Aggregate/Average-wise

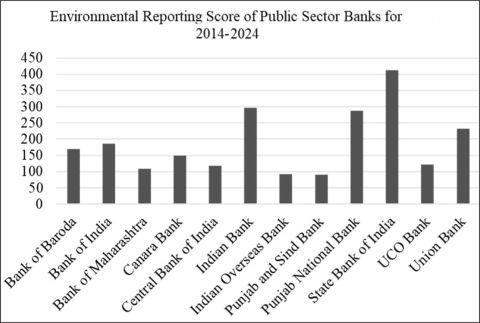

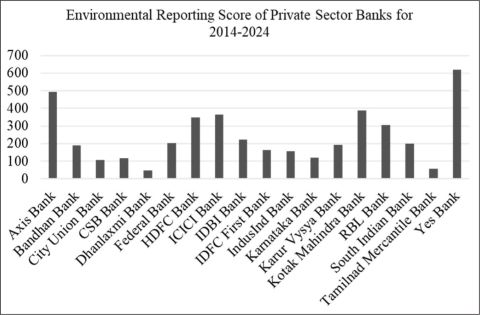

Over the course of 10 consecutive years, the environmental reporting scores of these 30 Indian banks were assessed using aggregate/average-wise criteria. Public sector banks’ individual environmental reporting scores are displayed in Figure 1. For the relevant 10-year period, the State Bank of India obtains the highest environmental reporting score. Next are Punjab National Bank and Indian Bank. The banks with the lowest environmental reporting scores are Indian Overseas Bank and Punjab & Sind Bank. The private sector banks’ individual environmental reporting scores are displayed in Figure 2. In terms of the relevant 10-year timeframe, Yes Bank has the greatest score. Next are Kotak Mahindra Bank and Axis Bank. The banks with the lowest scores include Dhanlaxmi Bank and Tamilnad Mercantile Bank. IndusInd Bank has the most indicators out of 42 indicators, according to a further study done in the context of the indicator-wise criterion. Next in line for a tie-up are Axis Bank, HDFC Bank and ICICI Bank. The second-ranked banks are closely followed by the State Bank of India and Yes Bank. Furthermore, the results make it evident that Tamilnad Mercantile Bank and Indian Overseas Bank meet on the fewest number of metrics. The same is true for Bank of Maharashtra and Dhanlaxmi Bank. Therefore, it is abundantly evident that none of the sample banks are fulfilling their environmental obligations and disclosing them in accordance with all 42 indicators.

Figure 1. Environmental Score of Public Sector Banks.

Figure 2. Environmental Score of Private Sector Banks.

Environmental Reporting Score of Selected Banks: Category-wise

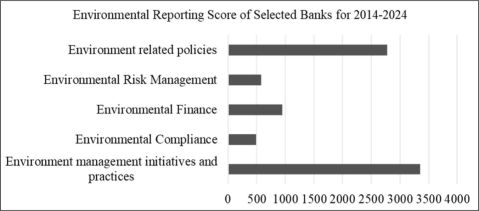

A category-wise analysis of 30 chosen banks was conducted after the 42 indicators were divided into five main categories: environment-related policies, environment risk management, environmental finance, environmental compliance and environment management initiatives and practices. The banks in the sample are reporting under environmental management initiatives and practices, which have the highest score, as shown in Figure 3. Next are environmental policies. Third is environmental finance. The sample banks are reporting the least amount of environmental compliance during the research period, with environmental risk management coming in at number four (Table 1 and Table 2).

Figure 3. Total Environmental Reporting Score Category-wise.

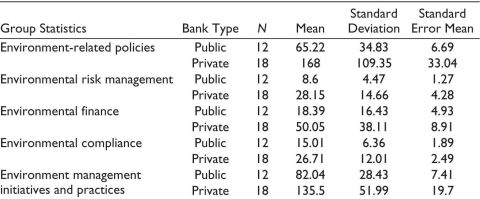

Table 1. Descriptive Statistics for Selected Banks for the Different Dimensions.

Table 2. Inferential Statistics for Selected Banks for Environment-related Policies.

.jpg/10_1177_09728686251411693-table2(1)__480x255.jpg)

Quantitative Analysis

There exist notable distinctions between public and private banks’ environmental measures. The much higher mean ratings of private banks show a far higher level of commitment than those of state banks. A substantial difference in variances is indicated by Levene’s test, indicating that private banks are more aggressive in putting environmental rules into place. Private banks perform better than public banks, as seen by higher mean scores and Levene’s test showing considerable variance inequality. This is because private banks have greater integration of risk management methods connected to environmental challenges. The findings suggest that private banks could place more emphasis on environmental responsibility and sustainability, either as a result of regulatory requirements or competitive pressures.

Significant distinctions between public and private banks in the context of environmental finance are highlighted by the analysis. The much higher mean ratings of private banks show a far higher level of commitment than those of state banks. The results of Levene’s test show a negligible difference in variances, indicating that public and private banks are roughly equally aggressive in providing funding for projects that address environmental issues. Greater environmental compliance is reflected in higher mean scores, which show that private banks perform better than public banks. Private and public banks appear to be about equally aggressive in extending compliances and regulatory concerns from an environmental standpoint, according to Levene’s test, which shows a minor difference in variances. Private banks perform better than public banks, as seen by higher mean scores and Levene’s test showing considerable variance inequality. This is because private banks have superior environmental management programmes and policies. The findings suggest that environmental responsibility and sustainability may be given more attention by private banks.

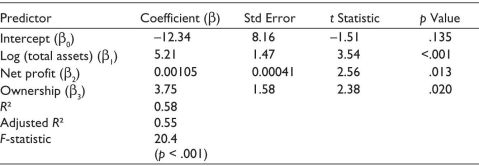

To determine whether differences in environmental disclosure persist beyond structural and financial capacity, a multiple regression was estimated across 30 major Indian banks (Table 3). The model, with R2 of 0.58 ((adjusted R2 = 0.55, F = 20.4, p < .001), reveals that logarithm of total assets is a strong and significant predictor (β = 5.21, p < .001), indicating that larger banks disclose more on environmental practices. Net profit also has a positive and significant effect (β = 0.00105, p = .013), indicating that more profitable banks engage in deeper environmental reporting. Ownership remains a significant factor (β = 3.75, p = .020), confirming that private banks score on average 3.75 points higher than public sector banks, even after accounting for size and profit.

Table 3. Regression of Environmental Score on Bank-level Controls.

Model: EnvScorei = b0 + b1·log (TotalAssetsi) + b2·NetProfiti + b3·Ownershipi + fi.

Illustrative Qualitative Insights from Bank Reports

While this research is quantitative, some quotes from public disclosures provide a qualitative context to banks’ environmental commitments. These quotes are from publicly available sustainability and annual reports and show how banks frame their environmental strategy beyond checklists.

SBI’s commitment to sustainable development is reflected in our ESG framework, which prioritizes responsible lending, adoption of renewable energy, and afforestation drives. In FY24, SBI financed 5,213 MW of renewable energy capacity and initiated 1.1 million tree plantations under its Green India initiative. (SBI Sustainability Report 2024, p. 12)

We are integrating ESG factors across our lending and investment portfolios. Our ‘Parivartan’ platform focuses on green product innovation, low-carbon lending, and supporting communities vulnerable to climate change. (HDFC Bank ESG Report 2024, p. 8)

As the first Indian bank to sign the UNEP-FI Principles for Responsible Banking, we aim to become a catalyst for India’s green transition. Our commitment to responsible banking is operationalized through internal green bond frameworks and sector-specific environmental risk assessments. (Yes Bank BRSR 2024, p. 10)

These narrative disclosures support the numbers which state that banks with higher scores tend to integrate sustainability more into their core strategy. Private banks in particular use environmental reporting not only for compliance but also for stakeholder engagement and market positioning.

Findings

Banks have definitely been boosting their environmental reporting during this time, even if they are still in the early stages of implementing full environmental reporting processes. Since none of the sample banks reported on all 42 environmental indicators, there are gaps in the complete reporting of environmental commitments. The greater increase rate in environmental reporting indicates that private sector banks have taken a more active approach to environmental initiatives. The independent sample t-test reveals notable distinctions between public and private sector banks in each area of environmental reporting, with private banks outperforming public ones across the board. Controlling for size and profitability, private banks report significantly more on environmental issues than public banks, while larger banks and higher profitability are also positively associated with stronger reporting. Qualitative excerpts from the bank reports support that private sector banks articulate a clearer and more integrated sustainability story, as do their higher scores. Finally, there is still a tremendous need for improvement, particularly in public sector banks’ environmental reporting and operations, even though both private and public sector banks are making progress.

Recommendation

Based on the results of the thorough analysis and the lengthy investigation that was carried out, the following practical recommendations or proposals have been made. Banks must think about meeting all environmental indicators in order to achieve complete and transparent environmental reporting success. Both public and private banks are required to submit more thorough and transparent reports on their environmental initiatives, along with particular goals and outcomes. Banks must have continuous procedures to track and evaluate the effectiveness of their environmental initiatives in order to be held accountable. Banks must spend money on educating those in charge of environmental reporting if they want to obtain better and more accurate data. To encourage banks to enhance their environmental disclosures and practices, government and regulatory agencies must provide clear guidelines and incentives.

Implications of the Study

Important new information about the relationship between corporate reporting in the banking industry and environmental sustainability is provided by this study. By improving CSR and environmental reporting, banks will make a stronger case for environmental responsibility. The study shows that customers, investors and regulators prefer banks that are more environmentally committed and stronger environmental reporting is associated with better financial performance and competitive advantage. This is in line with stakeholder theory, which states that for organisations to succeed they must meet the expectations of multiple stakeholders, including environmental ones.

The study provides policymakers and regulators with insights to promote better environmental reporting in India’s banking sector. According to the study, regulatory frameworks should encourage public and private banks to have more extensive and clear environmental reporting requirements. The government can play a big role by having regulations that ensure uniformity across the industry. The study shows how banks can not only comply with regulations but also become leaders in sustainability by integrating sustainability into their core operations, using green financing, improving internal processes and being transparent about environmental data.

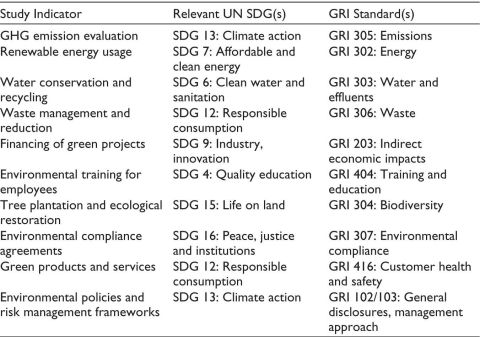

To enhance the policy relevance and generalisability of the findings, the study’s indicators were thoroughly examined in light of global sustainability benchmarks, specifically the United Nations Sustainable Development Goals (UN SDGs) and the GRI Standards. Table 4 maps the selected environmental indicators used in the study to relevant SDG targets and GRI disclosure standards.

Table 4. Mapping of Selected Environmental Indicators to UN SDGs and GRI Standards.

The mapping in Table 4 highlights that the indicators analysed in the study are relevant not merely for local and institutional improvements but also tend to contribute to the broader international sustainability agenda. As Indian banks progress in environmental reporting, alignment with these global frameworks will enhance transparency, comparability and stakeholder trust, whilst enabling a better tracking of progress towards global climate and sustainability goals.

The report highlights how environmental sustainability can be a business advantage for the banking sector. Strong environmental reporting will attract partners, investors and customers who value sustainability. Their market positioning can improve with this trend, especially with customers who care for the environment. Private banks can increase customer loyalty and reputation by showcasing their commitment to sustainability. But if they do not invest in sustainable practices, public sector banks will lag behind and miss out on green financing, new revenue streams and alignment with national and international sustainability goals.

Conclusion

This study demonstrates how reporting practices have advanced, particularly among banks in the private sector. There are still shortcomings in public sector banks’ use of comprehensive environmental indicators, notwithstanding the advancements. Through transparent reporting and thorough environmental policies, Indian banks may foster stakeholder trust and align with global sustainability standards. According to the report, coordinated tracking systems, capacity building initiatives and regulatory backing are required to increase the sector’s environmental responsibility. By bolstering banks’ finances and accomplishing the larger objective of sustainable development, better environmental regulations will eventually help both the economy and the environment.

Future Scope of the Study

The study’s stated limitations may serve as a springboard for more investigation in the targeted field. A longer time range and the utilisation of primary data over and above secondary data might be tried, improved generalisation by more rational classification and analysis using other pertinent statistical methods. Further, the inclusion of foreign banks might provide greater comparison insights.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Jayshree Roongta https://orcid.org/0009-0005-9938-0465

Agostini, M., Costa, E., & Korca, B. (2021). Non-financial disclosure and corporate financial performance under Directive 2014/95/EU: Evidence from Italian listed companies. Accounting in Europe, 19(1), 78–109. https://doi.org/10.1080/17449480.2021.1979610

Agyei, S. K., & Yankey, B. (2019). Environmental reporting practices and performance of timber firms in Ghana. Journal of Accounting in Emerging Economies, 9(2), 268–286. https://doi.org/10.1108/jaee-12-2017-0127

Appiah, B. K., Donghui, Z., Majumder, S. C., & Monaheng, M. P. (2019). Effects of environmental strategy, uncertainty and top management commitment on the environmental performance: Role of environmental management accounting and environmental management control system. International Journal of Energy Economics and Policy, 10(1), 360–370. https://doi.org/10.32479/ijeep.8697

Banker, R. D., Mashruwala, R., & Tripathy, A. (2014). Does a differentiation strategy lead to more sustainable financial performance than a cost leadership strategy? Management Decision, 52(5), 872–896. https://doi.org/10.1108/md-05-2013-0282

Biswas, S., & O’Grady, W. (2016). Using external environmental reporting to embed sustainability into organisational practices. Accounting Research Journal, 29(2), 218–235. https://doi.org/10.1108/arj-04-2015-0063

Chakroun, R., Matoussi, H., & Mbirki, S. (2017). Determinants of CSR disclosure of Tunisian listed banks: A multi-support analysis. Social Responsibility Journal, 13(3), 552–584. https://doi.org/10.1108/srj-04-2016-0055

Chandok, R. I. S., & Singh, S. (2017). Empirical study on determinants of environmental disclosure. Managerial Auditing Journal, 32(4/5), 332–355. https://doi.org/10.1108/maj-03-2016-1344

Chatterjee, B., & Mir, M. Z. (2008). The current status of environmental reporting by Indian companies. Managerial Auditing Journal, 23(6), 609–629. https://doi.org/10.1108/02686900810882138

Chouaibi, S., Rossi, M., Siggia, D., & Chouaibi, J. (2021). Exploring the moderating role of social and ethical practices in the relationship between environmental disclosure and financial performance: Evidence from ESG companies. Sustainability, 14(1), 209. https://doi.org/10.3390/su14010209

Day, R., & Woodward, T. (2009). CSR reporting and the UK financial services sector. Journal of Applied Accounting Research, 10(3), 159–175. https://doi.org/10.1108/09675420911006398

Deegan, C., & Gordon, B. (1996). A study of the environmental disclosure practices of Australian corporations. Accounting and Business Research, 26(3), 187–199. https://doi.org/10.1080/00014788.1996.9729510

Fischer, M., Foord, D., Frecè, J., Hillebrand, K., Kissling-Näf, I., Meili, R., Peskova, M., Risi, D., Schmidpeter, R., & Stucki, T. (2023). Sustainable business. In SpringerBriefs in business. Springer. https://doi.org/10.1007/978-3-031-25397-3

Godfrey, P. C. (2005). The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Academy of Management Review, 30(4), 777–798. https://doi.org/10.5465/amr.2005.18378878

Goel, P., & Misra, R. (2017). Sustainability reporting in India: Exploring sectoral differences and linkages with financial performance. Vision the Journal of Business Perspective, 21(2), 214–224. https://doi.org/10.1177/0972262917700996

Hossain, M., & Reaz, M. (2007). The determinants and characteristics of voluntary disclosure by Indian banking companies. Corporate Social Responsibility and Environmental Management, 14(5), 274–288. https://doi.org/10.1002/csr.154

Kılıç, M., & Kuzey, C. (2019). Determinants of climate change disclosures in the Turkish banking industry. International Journal of Bank Marketing, 37(3), 901–926. https://doi.org/10.1108/ijbm-08-2018-0206

Kumar, K. (2020). Emerging phenomenon of corporate sustainability reporting: Evidence from top 100 NSE-listed companies in India. Journal of Public Affairs, 22(1). https://doi.org/10.1002/pa.2368

Kumar, K., Kumari, R., Nandy, M., Sarim, M., & Kumar, R. (2022). Do ownership structures and governance attributes matter for corporate sustainability reporting? An examination in the Indian context. Management of Environmental Quality, 33(5), 1077–1096. https://doi.org/10.1108/meq-08-2021-0196

Kumar, K., & Prakash, A. (2019). Managing sustainability in banking: Extent of sustainable banking adaptations of banking sector in India. Environment Development and Sustainability, 22(6), 5199–5217. https://doi.org/10.1007/s10668-019-00421-5

Kumar, R., Pande, N., & Afreen, S. (2017). Developing a GRI-G4-based persuasive communication framework for sustainability reporting (SR). International Journal of Emerging Markets, 13(1), 136–161. https://doi.org/10.1108/ijoem-01-2017-0015

Kumar, V., Gunasekaran, A., Singh, K., Papadopoulos, T., & Dubey, R. (2015). Cross sector comparison of sustainability reports of Indian companies: A stakeholder perspective. Sustainable Production and Consumption, 4, 62–71. https://doi.org/10.1016/j.spc.2015.08.005

Nizam, E., Ng, A., Dewandaru, G., Nagayev, R., & Nkoba, M. A. (2019). The impact of social and environmental sustainability on financial performance: A global analysis of the banking sector. Journal of Multinational Financial Management, 49, 35–53. https://doi.org/10.1016/j.mulfin.2019.01.002

Nurhayati, R., Taylor, G., Rusmin, R., Tower, G., & Chatterjee, B. (2016). Factors determining social and environmental reporting by Indian textile and apparel firms: A test of legitimacy theory. Social Responsibility Journal, 12(1), 167–189. https://doi.org/10.1108/srj-06-2013-0074

Pahuja, S. (2007). Environmental reporting verification: A critical evaluation of accountants’ views and corporate practices in India. Social Responsibility Journal, 3(2), 22–31. https://doi.org/10.1108/17471110710829696

Pahuja, S. (2009). Relationship between environmental disclosures and corporate characteristics: A study of large manufacturing companies in India. Social Responsibility Journal, 5(2), 227–244. https://doi.org/10.1108/17471110910964504

Prasad, M., Mishra, T., & Kalro, A. D. (2016). Environmental disclosure by Indian companies: An empirical study. Environment Development and Sustainability, 19(5), 1999–2022. https://doi.org/10.1007/s10668-016-9840-5

Radhouane, I., Nekhili, M., Nagati, H., & Paché, G. (2018). The impact of corporate environmental reporting on customer-related performance and market value. Management Decision, 56(7), 1630–1659. https://doi.org/10.1108/md-03-2017-0272

Sahay, A. (2004). Environmental reporting by Indian corporations. Corporate Social Responsibility and Environmental Management, 11(1), 12–22. https://doi.org/10.1002/csr.51

Sandhu, S., Smallman, C., Ozanne, L. K., & Cullen, R. (2012). Corporate environmental responsiveness in India: Lessons from a developing country. Journal of Cleaner Production, 35, 203–213. https://doi.org/10.1016/j.jclepro.2012.05.040

Sen, M., Mukherjee, K., & Pattanayak, J. (2011). Corporate environmental disclosure practices in India. Journal of Applied Accounting Research, 12(2), 139–156. https://doi.org/10.1108/09675421111160709

Sharma, M., & Choubey, A. (2021). Green banking initiatives: A qualitative study on Indian banking sector. Environment Development and Sustainability, 24(1), 293–319. https://doi.org/10.1007/s10668-021-01426-9

Tilt, C. A. (2006). Linking environmental activity and environmental disclosure in an organisational change framework. Journal of Accounting & Organizational Change, 2(1), 4–24. https://doi.org/10.1108/18325910610654108

Yadav, M. P., & Sinha, N. (2021). Investigating the impact of corporate social responsibility on competitive performance: An empirical study based on panel data analysis. FIIB Business Review, 11(2), 165–173. https://doi.org/10.1177/23197145211015443

Ye, K., & Zhang, R. (2011). Do lenders value corporate social responsibility? Evidence from China. Journal of Business Ethics, 104(2), 197–206. https://doi.org/10.1007/s10551-011-0898-6