Review of Professional Management

Search

Search

A Systematic Literature Review on the Impact of Capital Structure on Corporate Financial Performance

Nidhin John1 and Siby Joseph K.1

and Siby Joseph K.1

1 Department of Business Administration, St. Berchmans College, Kottayam, Kerala, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

The study attempts to consider the theoretical foundations and empirical literature on the relationship between the capital structure of a firm and corporate financial performance using a systematic literature review approach. Systematic literature review methodology attempts to study the existing literature on a research question in a scientific manner that is transparent and replicable. It is a methodology that is becoming increasingly popular in research due to the transparency and replicability of the approach. Research papers reviewed were compiled based on a systematic approach, using research papers indexed in web of science database. Literature surveyed reveals that Studies have been conducted at the economy level, sectoral level (manufacturing, services) and for specific industries. While most researches conclude that there is indeed a significant impact of capital structure of a firm on the financial performance, they differ in their opinions on the nature of the impact. The studies lack unanimity on whether the level of debt employed in the capital has a positive or negative impact on financial performance. Differences have been observed in terms of the impact of short-term debt and long-term debt on financial performance as well.

Capital structure, leverage, financial performance, profit, systematic literature review, financial economics, business policy

Introduction

Capital structure is among the key financial decisions in a firm. Capital structure represents the proportionate relationship between debt and equity (Pandey, 2010). Long-term sources of finance are said to constitute the capital structure rather than short-term sources. It is a decision which influences the shareholders’ return and risk. Thus, capital structure decision has implications on the financial performance of a company. This study examines the state of literature on the relationship between these two critical aspects, namely capital structure and corporate financial performance. Although there are many theories pertaining to the relation between these two variables, there is a need for empirical testing as financial performance is a key variable for the survival of a firm. The objective of this study is to focus on studies specific to the relation between capital structure and financial performance, integrate the results, and synthesise and present them in a summarised manner.

One of the early studies focussing on capital structure was conducted by Modigliani and Miller in 1958. The study focussed on capital structure and the market value of a firm, wherein they argued that in perfect capital markets, the market value of a firm is not affected by changes in capital structure (Pandey, 2010). A later study by Modigliani and Miller in 1963 showed that in the presence of taxes, the debt component in the capital structure of a firm can enhance the value of the firm (Pandey, 2010). Miller in 1977 conducted a study which considered both corporate and personal taxes and concluded that the benefits due to the use of corporate borrowing in the capital structure are reduced by personal tax loss (Pandey, 2010). According to the trade-off theory, although debt in the capital structure is beneficial due to the tax advantage, it also brings the disadvantages associated with financial distress and agency costs (Pandey, 2010). The optimum level of debt could be in the scenario where the advantage due to tax benefits of debt is balanced by the cost of financial distress (Pandey, 2010). As per the pecking order theory, the preferred option for financing by managers is internal finance, followed by debt and finally issue of shares (Pandey, 2010).

The theories related to capital structure are not new. Yet, a consensus on what could be the optimal capital structure has not been arrived at yet (Abor, 2005). There has been no dearth of empirical papers trying to test the impact of capital structure on various parameters of financial performance. But when it comes to the outcomes of these empirical papers, the results have been divergent on the nature of the impact whether positive or negative. The significance of capital structure decision is indisputable, but assessments of the nature of the impact have been inconclusive. Apart from the divergent conclusions, various papers have resorted to varying theories to support their conclusions, including trade-off theory, agency costs approach and pecking-order theory. Thus, when the conclusions of empirical studies have been divergent, can researches enable a practising manager to get reliable guidance while taking such a critical decision. Faced with such diverging conclusions and divergent reasoning for the same, the current study has been performed with the objective to analyse, interpret, synthesise and arrive at coherent conclusions and practical implications from the current literature on the impact of capital structure on financial performance by adopting a systematic approach that is replicable, scientific and transparent. The paper is divided into keywords, introduction, methodology, systematic literature review, results and discussion, findings, policy implications and conclusion and finally bibliography.

Methodology

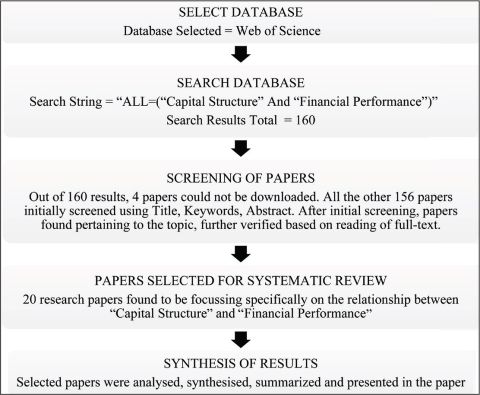

Systematic literature review, as compared to normal literature reviews, performs the review in a systematic manner. Tranfield et al. (2003) state that systematic literature review involves adopting a replicable, scientific and transparent process for conducting the review of literature; consequently, the bias in the review gets reduced. Systematic literature review helps in identifying the key scientific contributions in a field (Tranfield et al., 2003). The systematic literature review for this paper was conducted over multiple stages. In the first stage, ‘Web of Science’ was selected as the search database. Within Web of Science, the search was limited to the ‘Core Collection’. Web of Science Core Collection is the world’s leading citation database containing records of articles from the highest-impact journals worldwide (Web of Science Core Collection, 2021). In the second stage, the keywords were decided. The keywords decided were ‘capital structure’ and ‘financial performance’. The Web of Science database was searched to get the list of all research papers with the keywords in any of the fields. The search string used was ‘ALL = “Capital Structure” and “Financial Performance”’. The keyword ‘ALL’ searches for the terms in all the fields in the record. The Boolean operator ‘And’ was used to ensure that Web of Science finds records with both the terms ‘Capital Structure’ and ‘Financial Performance’ (Search Operators, 2023). The search string was given in quotations to ensure exact text match. Overall ‘160’ research papers came in the search results, of which 4 research papers were not retrievable for download. In the third stage the 156 Web of Science indexed research papers were studied. These papers were initially analysed based on title, abstract and keywords. Apart from the subject focus on capital structure and financial performance, studies focussing primarily on profit-oriented corporate firms were selected. Only papers published in English language were selected. Tranfield et al. (2003) suggests detailed evaluation of the full text for finally selecting the papers for the systematic literature review. So, subsequent to the initial screening, from among the articles found as relevant, a further reading of the full text of the articles were done. This ensured that only articles pertaining to the specific topic were included. Based on such detailed analysis in multiple stages, it was found that 20 research papers were focussing specifically on the relationship between capital structure on Corporate Financial Performance. These papers were used for the systematic literature review. A systematic literature should be able to bring out the key emerging themes and research questions (Tranfield et al., 2003). The key themes from the selected papers are discussed in this study, along with the key findings, policy implications and possible research questions. The steps involved in the systematic literature review process are shown in Figure 1. The Web of Science database search was conducted during November 2023.

Figure 1. Systematic Literature Review Flowchart.

Systematic Literature Review

Gleason et al. (2000) studied the nature of influence of capital structure on financial performance for retailers in 14 European countries. The relationship between capital structure and performance was found to be negative. The possible reason was that excess debt was taken to tackle agency issues, which may ultimately be lowering the performance of a firm.

Phillips and Sipahioglu (2004) studied the capital structure and corporate performance with regard to hotel companies. The study relied on data collected from quoted organisations in the United Kingdom. The study resulted in the conclusion that no significant relationship could be established between the proportion of debt in a firm’s capital structure and financial performance.

Dawar (2014) studied the impact of the choice of capital structure on the performance in the case of listed Indian firms, using return on assets (ROA) and return on equity (ROE) as measures of financial performance. The results indicated that debt has a negative effect on profitability.

Bayaraa (2017) examined the ratios which determine the financial performance of Mongolian companies. The companies were categorised into six major sectors. The results confirmed that capital structure is one of the determinants of financial performance in Mongolia. Sector wise, only for the mining and agricultural sector was the ratio of long-term debt to total assets found to be significant. The ratio of short-term debt to total assets was found to be a significant determinant in the case of the service sector alone.

B.png) rbu

rbu.png) -Mi

-Mi.png) u et al. (2019) investigated how financial variables influence firms’ financial performance. Results indicated that leverage positively affected firm performance.

u et al. (2019) investigated how financial variables influence firms’ financial performance. Results indicated that leverage positively affected firm performance.

Botta (2019) investigated an optimal capital structure for Italian small and medium enterprises (SME) in the hotel sector. The study analysed the relationship between financing decisions and financial performance. The results pointed towards an optimal capital structure, while too little or too much debt both adversely impacted the financial performance. The results give support to the predictions of the trade-off theory.

Özcan (2019) examined how the capital structure affects profitability in the case of publicly traded airports. The study relied on a sample from 20 countries. The results showed that long-term leverage and total leverage reduced the ROA, but were associated with higher ROE.

Ramli et al. (2019) examined the determinants of capital structure for its impact on financial performance of firms in Malaysia and Indonesia. Also, the mediation effect of firm leverage was studied. The finding of the study was that there is a positive significant correlation between firm leverage and firm financial performance in the case of the Malaysian sample.

Mardones and Cuneo (2020) analysed the financial performance of Latin American companies with regard to the relationship with capital structure and ownership structure. The study focussed on companies from Brazil, Chile, Mexico and Peru. As for the effect of leverage on financial performance, as mixed results were seen regarding the impact of short-term debt and long-term debt, the results were inconclusive.

Parvin et al. (2020) analysed the effect of capital structure on financial performance focussing on micro-finance institutions from Bangladesh. The effect of equity to asset ratio (EAR) on ROA was found to be positive and significant.

Ullah et al. (2020) studied the role of capital structure in determining the financial performance. The study focussed on 90 textile firms listed in Pakistan Stock Exchange (PSX). Return on equity was used for measuring for financial performance. A negative and significant relationship was found between debt-to-equity ratio and financial performance.

Xu et al. (2021) studied how capital structure impacts financial performance in the case of listed agricultural companies from China. ROA and ROE were the variables used as measures of financial performance. Total debt, short-term debt and long-term debt ratios were used as measures for capital structure. The variables total debt ratio and short-term debt ratio were found to negatively impact the financial performance, whereas the variable long-term debt ratio was found to have no significant impact on ROA and ROE.

Ghardallou (2022) studied the relationship between financing decisions and firm performance. Quantile regression methodology was employed in the study. The sample studied included 120 listed non-financial companies. The companies were listed in Tadawul Stock Exchange during the period 2017–2020. Results demonstrated that more debts adversely affected the performance.

Luo and Jiang (2022) studied the impact that corporate capital structure has on financial performance. The methodology employed was based on convolutional neural network. The conclusion arrived at was that short-term liabilities can have a favourable influence on the operating income of a company.

Ulbert et al. (2022) studied whether the golden ratio–based capital structure had a positive impact on financial performance. They used data from manufacturing and service firms from the United States and Europe. The results affirmed that capital structure based on golden ratio could enhance financial performance. The relationship was found to be more obvious in the case of the United States. Moreover, the relationship was found to be stronger in the case of service firms.

Vukovi.png) et al. (2022) analysed the major factors that impact financial performance. The sample consisted of 460 European agricultural companies. Short-term debt to total asset ratio, long-term debt to total asset ratio and debt to asset ratio were found to have a negative correlation with performance.

et al. (2022) analysed the major factors that impact financial performance. The sample consisted of 460 European agricultural companies. Short-term debt to total asset ratio, long-term debt to total asset ratio and debt to asset ratio were found to have a negative correlation with performance.

Adam et al. (2023) analysed the influence of leverage on financial performance. The study focussed on Brazilian and Mexican family businesses. Higher debt was found to be associated with lower financial performance in terms of ROA.

Amin and Cek (2023) studied the deviation of capital structure from the golden ratio for the impact on financial performance. The study used a sample of non-financial firms from France and the United Kingdom. The results revealed that capital structure based on golden ratio can have a positive significant impact on the financial performance in both the countries. Also, deviation from the golden ratio did have a negative significant effect on financial performance.

Mazanec (2023) estimated business performance using selected indicators including capital structure of transport companies in Central Europe. As per the results, a high debt ratio negatively impacts corporate performance.

Sz.png) llsi and Erds (2023) studied companies engaged in crop production, focussing on the V4 countries, namely Poland, Slovakia, Czechia and Hungary. With respect to capital structure, higher financial profitability was found to be associated with a lower debt rate.

llsi and Erds (2023) studied companies engaged in crop production, focussing on the V4 countries, namely Poland, Slovakia, Czechia and Hungary. With respect to capital structure, higher financial profitability was found to be associated with a lower debt rate.

Results and Discussion

Review of the literature reveals that some of the studies point to a positive relation between the proportion of debt present in the capital structure and the financial performance of the firm. Ramli et al. (2019) found a positive relation between firm leverage and firm financial performance with regards to the Malaysian sample. Debt can indeed have a positive impact on financial performance, as it brings with it tax advantages. As we know the interest paid on debt is deductible while computing tax, it thus provides what is known as interest tax shield to the firm. This interest tax shield reduces the cost of capital of the firm. Brbu-Miu et al. (2019) observed leverage and performance as having a positive relationship. The study explained the result based on agency theory: that in order to reduce agency costs associated with free cash flows, it would be beneficial for profitable firms to take on higher leverage.

On the contrary, some of the studies, including Gleason et al. (2000), pointed towards a negative relationship between the level of debt present in the capital structure and the financial performance. This could be due to the fact that, although debt does bring in tax advantages, it also brings with it the disadvantages of possible financial distress and agency costs of debt. Financial distress refers to the situation in which the firm is not able to meet the interest obligations. Even when a formal default is avoided, there could be indirect costs that the firm might have to incur, due to the increased possibility of financial distress, as the level of debt in capital structure increases. There could also be agency costs of debt, which include the cost to the firm due to restrictive covenants which creditors might impose. Parvin et al. (2020) suggest that, as institutions use leverage as a measure to avoid agency conflicts, the resultant overleveraging can negatively affect performance.

Interestingly, there were also some studies such as Mardones and Cuneo (2020) which could not arrive at a definitive conclusion on the relationship between the proportion of debt in the capital structure and financial performance.

Ramli et al. (2019) pointed out that attributes specific to the countries studied, such as development of stock markets in the country, development of bond market in the country and inflation, may influence the relationship between leverage and financial performance of the firm. This study was conducted using a Malaysian sample and an Indonesian sample. Interestingly, a positive significant correlation between the studied variables was found only in the case of the Malaysian sample. Such sector-based and country-based differences were also pointed out by Ulbert et al. (2022). The study, relying on data from manufacturing and service firms from the United States and Europe, affirmed the beneficial effects of golden ratio–based capital structure. Such beneficial effects were more observable in the case of firms from the United States as compared to Europe. Also, the effect was more pronounced in the case of service firms as compared to manufacturing companies.

The question here is what could be the reason for these differences in conclusion by various researchers. Let us analyse the possible reasons for the same. As we know even today that there is a large gap in the level of development of capital markets and financial institutions among the countries globally. Consequently, the lack of a developed capital market can increase the cost of equity faced by business organisations in such nations, leading to equity being a less-preferred component in the capital structure. Alternatively, if the financial institutions including the banking sector is underdeveloped in a nation, it can increase the cost of debt incurred by the business organisations, leading to debt being a less-preferred component in the capital structure. Further, it needs to be kept in mind that the development capital market in a nation is a continuously evolving process. To take the case of India, prior to the 1990s, capital markets in India were under the regime of the ‘Controller of Capital Issues’. Since liberalisation was undertaken in the financial sector in the 1990s, the capital markets in India have grown manifold. Joshi (2020) highlighted that in the Indian corporate sector, the reliance on debt has been on the decline especially after the mid-1990s. Globally, many emerging market economies around the world have seen such rapid development in capital markets in the last couple of decades, thereby making equity capital much more easily accessible in these nations. Another reason for the observed difference could be the intrinsic differences between the industries being focussed as part of the study. As we are aware, various industries such as steel industry and cement industry differ in various respects, including the investment in raw materials, the production process and the level of investment in current assets and fixed assets, to name a few.

Another interesting aspect observed in the studies is that even within an industry, there could be a difference between the impact of the short-term and long-term debt component in the capital structure on financial performance, as observed by Xu et al. (2021). The study used ROA ratio and ROE ratio as measures of financial performance. As per the study, short-term debt ratio and total debt ratio had a negative influence on financial performance of firms in the agricultural sector in China. But when it comes to long-term debt ratio, there was no significant impact. The difference in interest costs, with higher costs usually associated with long-term debt, could be a reason for this contradiction in impact between short-term debt component and long-term debt component.

The question also deserves attention from a theoretical standpoint as many theories have been propounded on the relationship between the capital structure and the financial performance: trade-off theory, agency costs theory and pecking order theory to name a few. Kraus and Litzenberger (1973) stated that achieving optimum financial structure in a firm involves considering the trade-off between the benefit of tax advantage due to debt and the adverse impact of possibility of bankruptcy. Jensen (1986) highlighted the role of debt in mitigating the agency costs associated with free cash flows available with managers. The danger of not being able to make interest payments of debt can motivate organisations to become more efficient. But it needs to be kept in mind that debt also has agency costs associated with it. As the level of debt increases, the agency cost of debt also increases. So, achieving optimal capital structure would involve considering both the benefits and costs associated with debt. Brbu-Miu et al. (2019) explained the positive relationship between leverage and ROA found in the study using the ‘Agency Theory’. The study suggested more profitable firms have a necessity to take on higher levels of debt to mitigate the adverse impacts associated with agency costs of free cash flow. Botta (2019), on the other hand, pointed towards the adverse impact of agency costs of debt; that is, incurring excessive debt can hamper profits. Myers and Majluf (1984) highlighted that for the purpose of sourcing funds, firms look first for internal sources. Among the external sources of funds, debt is preferred over equity. This points towards a hierarchy or ‘Pecking Order’ in terms of preferences for sources of finance (Myers, 1984). Botta (2019), while studying the financial decisions of Italian hotel SMEs, also found a financing pattern consistent with such a pecking order model with a hierarchy in terms of financing preferences with a strong reliance on internal funds among Italian hotel SMEs.

As for the methodology employed by the researchers, as observed in the systematic literature review, the most common methodology was regression analysis–based techniques using panel data (Dawar, 2014). Panel data are multi-dimensional in the sense that they are about multiple entities or firms over multiple years (Parvin et al., 2020). Specific models coming under panel data–based analysis include pooled OLS, fixed effects model and random effects model (Ulbert et al., 2022). Hausman test can be used to choose whether the fixed effects model or the random effects model should be used (Dawar, 2014). Panel unit root tests can be used to check for stationarity of the data (Amin & Cek, 2023; Ullah et al., 2020). Checks for multicollinearity (Amin & Cek, 2023; Mazanec, 2023), heteroskedasticity (Amin & Cek, 2023) and autocorrelation (Amin & Cek, 2023; Özcan, 2019) are also performed.

As for the proxy variables used to study capital structure, debt to asset ratios have been most commonly used. Dawar (2014) used short-term debt to total assets ratio and long-term debt to total assets ratio as measures for representing the capital structure. As for the proxy for measuring financial performance, many of the studies used ROE and ROA (Dawar, 2014; Phillips & Sipahioglu, 2004). The other variables which were identified to have an effect on financial performance and, therefore, whose effect has been controlled for in the studies include asset tangibility and size of the firm. Dawar (2014), relying on prior research, states that the impact of tangibility on profitability is inconclusive. The study proposes that tangible assets may play a role in mitigating agency conflicts. But at the same time, firms with intangible assets may have more funds to invest, thus leading to a negative relationship between tangibility and profitability (Dawar, 2014). Vukovi et al. (2022) found that the relationship between asset tangibility and financial performance is negative in the case of agricultural companies in Europe. The study suggested that this could be the result of the lack of optimal use of fixed assets by these companies. Mardones and Cuneo (2020) found a positive relation between size and performance and suggested that this could be due to the fact that large companies face lower bankruptcy costs, leading to higher profitability. Vukovi et al. (2022) also found the relationship between firm size and financial performance as positive in the case of European agricultural companies and suggested that reasons could be that larger companies would have easier access to financial resources and advantages from economies of scale.

Findings of the Literature Review

The literature review gave valuable insights on the existing literature on the impact of capital structure on financial performance. It is seen that studies have been conducted at the economy level, sectoral level (manufacturing sector, services sector) and for specific industries (such as cement industry, steel industry, hotel industry, etc.). The conclusions of the studies point to the fact that they lack unanimity on whether the level of debt present in the capital structure has a positive or negative impact on the financial performance. Further, there is a difference between the nature of the impact of short-term debt on financial performance and the nature of the impact of long-term debt on financial performance. Studies reveal that industry specific differences have a role in the impact of the different sources of finance in the capital structure on the corporate financial performance. Trade-off theory, the Agency costs theory and the Pecking-order theory are among theories used to explain the findings regarding the relationship between capital structure and corporate financial performance. As for the variables employed in the studies, commonly used proxy variables for capital structure are the ratios of Short-Term Debt to Total Assets ratio and Long-Term Debt to Total Assets ratio. Commonly used proxy variables for financial performance are return on equity ratio and return on assets ratio. Control variables commonly studied include Asset tangibility and size of the firm. Multiple regression analysis methods using panel data is commonly adopted in many of the studies.

Policy Implications

Each source of capital has advantages and disadvantages. Debt has beneficial tax shield effects. Moreover, debt can reduce the agency costs associated with free cash flows. These factors do make debt an interesting proposition. But there are disadvantages of debt, including the cost of financial distress. There is agency cost associated with debt as well. Thus, while taking a decision on capital structure, all these advantages and disadvantages of the respective source of capital need to be kept in mind. Inter-industry differences also need to be kept in mind while taking capital structure decisions. Country-based differences, including the development of bond markets, capital markets and inflation levels, should also be kept in mind. Within the debt component of capital, the term of debt, whether short-term or long-term, is also a crucial aspect. From a theoretical perspective, the study indicates the scope for a more comprehensive theory, which can explain the impact of capital structure on financial performance. The country-based differences imply that the rules established by regulatory bodies, can impact the relationship between capital structure and financial performance, by facilitating the development of capital markets, bond market and banking sector. Such well-developed financial markets can very well reduce the costs associated with sourcing of capital and can have a salutary effect on enhancing the financial performance of firms.

Conclusion

The study is an attempt to perform a systematic literature review on the important topic of the impact of capital structure on financial performance and to summarise the conclusions arrived at by the existing literature. The systematic literature review invariably shows that capital structure indeed does have an impact on the financial performance of the firm. But studies conducted in various nations and various sectors differ in their assessment of the nature of impact. Differences are also observed in the impact of short-term debt and long-term debt as sources of finance. The contradictory results suggest the need for further sector-specific and industry-specific empirical studies, focussing on specific countries, using recent data. The variations in the empirical results and the purported reasons for such behaviour, also suggests the possibility of building further theories which might be able to better explain the relation between capital structure and financial performance in a more comprehensive manner. The review also highlights the need to assess the impact of other determinants of financial performance apart from capital structure including firm size, asset tangibility among others. Overall, the systematic literature review reveals that capital structure decision is indeed a significant decision, which necessitates more empirical research while keeping in mind the country-based and industry-based differences and nuances of the source of capital, such as short-term or long-term in case of debt.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Nidhin John https://orcid.org/0000-0003-1589-7095

Abor, J. (2005). The effect of capital structure on profitability: An empirical analysis of listed firms in Ghana. The Journal of Risk Finance, 6(5), 438–445. https://doi.org/ 10.1108/15265940510633505

Adam, C., Domingues, D. G., Gomes, D. G. D., & Silva, T. P. D. (2023). Evidence of diversification and leverage in the performance of Brazilian and Mexican family businesses. Latin American Research Review, 58(4), 892–907. https://doi.org/10.1017/lar.2023.10

Amin, H. I. M., & Cek, K. (2023). The effect of golden ratio-based capital structure on firm’s financial performance. Sustainability, 15(9), 7424. https://doi.org/10.3390/su15097424

Bărbuță-Mișu, N., Madaleno, M., & Ilie, V. (2019). Analysis of risk factors affecting firms’ financial performance: Support for managerial decision-making. Sustainability, 11(18), 4838. https://doi.org/10.3390/su11184838

Bayaraa, B. (2017). Financial performance determinants of organizations: The case of Mongolian companies. Journal of Competitiveness, 9(3), 22–33. https://doi.org/10.7441/joc.2017.03.02

Botta, M. (2019). Financing decisions and performance of Italian SMEs in the hotel industry. Cornell Hospitality Quarterly, 60(4), 335–354. https://doi.org/10.1177/ 1938965518816948

Dawar, V. (2014). Agency theory, capital structure and firm performance: Some Indian evidence. Managerial Finance, 40(12), 1190–1206. https://doi.org/10.1108/MF-10-2013-0275

Ghardallou, W. (2022). Capital structure decisions and corporate performance: Does firm’s profitability matter? Journal of Scientific and Industrial Research (JSIR), 81(08), 859–865. https://doi.org/10.56042/jsir.v81i08.59697

Gleason, K. C., Mathur, L. K., & Mathur, I. (2000). The interrelationship between culture, capital structure, and performance: Evidence from European retailers. Journal of Business Research, 50(2), 185–191. https://doi.org/10.1016/S0148-2963(99) 00031-4

Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review, 76(2), 323–329.

Joshi, D. V. (2020). Indian corporate and its capital structure: Changing trends. International Journal in Management and Social Science, 08(02).

Kraus, A., & Litzenberger, R. H. (1973). A state-preference model of optimal financial leverage. The Journal of Finance, 28(4), 911–922. https://doi.org/10.1111/j.1540-6261. 1973.tb01415.x

Luo, Y., & Jiang, C. (2022). The impact of corporate capital structure on financial performance based on convolutional neural network. Computational Intelligence and Neuroscience, 2022, 1–7. https://doi.org/10.1155/2022/5895560

Mardones, J. G., & Cuneo, G. R. (2020). Capital structure and performance in Latin American companies. Economic Research/Ekonomska Istraživanja, 33(1), 2171–2188. https://doi.org/10.1080/1331677X.2019.1697720

Mazanec, J. (2023). Capital structure and corporate performance: An empirical analysis from Central Europe. Mathematics, 11(9), 2095. https://doi.org/10.3390/math11092095

Myers, S. C. (1984). The capital structure puzzle. The Journal of Finance, 39(3), 574–592. https://doi.org/10.1111/j.1540-6261.1984.tb03646.x

Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221. https://doi.org/10.1016/0304-405X(84)90023-0

Özcan, İ. Ç. (2019). Capital structure and firm performance: Evidence from the airport industry. European Journal of Transport and Infrastructure Research, 19(3), 177–195. https://doi.org/10.18757/ejtir.2019.19.3.4384

Pandey, I. M. (2010). Financial management (10th ed). Vikas Publications.

Parvin, S. S., Hossain, B., Mohiuddin, M., & Cao, Q. (2020). Capital structure, financial performance, and sustainability of micro-finance institutions (MFIs) in Bangladesh. Sustainability, 12(15), 6222. https://doi.org/10.3390/su12156222

Phillips, P. A., & Sipahioglu, M. A. (2004). Performance implications of capital structure: Evidence from quoted UK organisations with hotel interests. The Service Industries Journal, 24(5), 31–51. https://doi.org/10.1080/0264206042000276829

Ramli, N. A., Latan, H., & Solovida, G. T. (2019). Determinants of capital structure and firm financial performance: A PLS-SEM approach—Evidence from Malaysia and Indonesia. The Quarterly Review of Economics and Finance, 71, 148–160. https://doi.org/10.1016/j.qref.2018.07.001

Search Operators. (2023). Web of science help. https://webofscience.help.clarivate.com/en-us/Content/search-operators.html

Szőllősi, L., & Erdős, A. D. (2023). Income and asset situation of companies producing arable crops in the Visegrad countries. Agriculture, 13(8), 1589. https://doi.org/10.3390/agriculture13081589

Tranfield, D., Denyer, D., & Smart, P. (2003). Towards a methodology for developing evidence‐informed management knowledge by means of systematic review. British Journal of Management, 14(3), 207–222. https://doi.org/10.1111/1467-8551.00375

Ulbert, J., Takács, A., & Csapi, V. (2022). Golden ratio-based capital structure as a tool for boosting firm’s financial performance and market acceptance. Heliyon, 8(6), e09671. https://doi.org/10.1016/j.heliyon.2022.e09671

Ullah, A., Pinglu, C., Ullah, S., Zaman, M., & Hashmi, S. H. (2020). The nexus between capital structure, firm-specific factors, macroeconomic factors and financial performance in the textile sector of Pakistan. Heliyon, 6(8), e04741. https://doi.org/ 10.1016/j.heliyon.2020.e04741

Vuković, B., Milutinović, S., Mijić, K., Krsmanović, B., & Jakšić, D. (2022). Analysis of financial performance determinants: Evidence from the European agricultural companies. Custos e Agronegócio, 18(1), 285–306.

Web of Science Core Collection. (2021). Web of science help. https://webofscience.help.clarivate.com/Content/wos-core-collection/wos-core-collection.htm

Xu, J., Sun, Z., & Shang, Y. (2021). Capital structure and financial performance in China’s agricultural sector: A panel data analysis. Custos e Agronegócio, 17(2), 445–463.