Review of Professional Management

Search

Search

1 Department of Commerce, Janki Devi Memorial College, University of Delhi, Delhi, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

As firms invest in foreign countries, they face additional costs of doing business in the form of liabilities of foreignness. The liabilities of foreignness are aggravated by the distance in the institutional environment of the home country in which the firms are embedded and the host country in which they invest. Within this context, the aim of this research paper is to examine if a specific form of institutional distance, that is, corruption distance, affects the quantum of inward foreign direct investment (FDI) in India, which is a large emerging market and an important receiver of global FDI flows. Using country-wise FDI inflows data from 2008 to 2020, the results of panel autoregressive distributed lag (ARDL) method reveal the presence of a long-run relationship between FDI inflows and corruption distance between India and the home country of the investor firm. The disequilibrium in the long-run relationship, if any, gets adjusted at the rate of 38.1% per year. The findings also suggest that an improvement in the control of corruption is expected to lead to greater FDI inflows in the country, thereby providing an important policy implication. To attract FDI and to fully realise its benefits which are essential for an emerging country like India, policymakers need to make concerted efforts to control the level of corruption.

FDI, corruption distance, panel ARDL, India, governance, institutional environment, liability of foreignness

Introduction

Foreign direct investment (FDI) has been one of the important manifestations as well as drivers of globalisation (Pekarskiene & Susniene, 2015). Not just as a source of finance, but developing and emerging economies make considerable effort to attract FDI inflows that bring in with it advanced technological and managerial knowledge, increased employment opportunities and spillovers. The recognition of positive effects of FDI on the host economy has been instrumental in making countries adopt market based economic reforms, improve the quality of institutions and liberalise foreign investment policies (United Nations, 2021). These efforts are directed at reducing the cost of doing business abroad (CDBA)which foreign companies face on the top of local companies in the latter’s home country (Eden & Miller, 2004). The CDBA refers to the social cost of doing business, manifested in the form of liability of foreignness that concerns the firms while investing abroad (Ramachandran & Pant, 2010). Existing research has suggested that the extent of liability of foreignness that investing firms (or MNEs) face in host countries may not only be the function of host’s institutional quality but also that of the home country (Cuervo-Cazurra, 2006; Nayyar et al., 2021). Firms learn from the institutional environment that they are embedded in (Peng et al., 2008) and this affects their ability and willingness to invest in particular locations. Hence, studying the difference between the institutional quality of home and host countries can provide more nuanced insights on the determinants of quantum of FDI inflows.

An important aspect of institutions, especially in emerging economies, is the level of corruption (Ghosh et al., 2022; Malanski & Póvoa, 2021; Rodina, 2022). Corruption distance is expected to influence the FDI flows as investors from low-corruption countries would face greater liabilities of foreignness in the host countries with higher levels of corruption, thereby making them hesitant of making the investment. We test this proposition in the context of FDI inflows in India which is an important receiver of global FDI flows.

We examined the impact of corruption distance on the inward FDI flows in India over the period 2008 to 2020—time period considered according to accessibility to data. More particularly, we attempted to examine if there exists any long-term relationship between corruption distance and FDI inflows in India. The results of panel autoregressive distributed lag (ARDL) show the existence of a long-term relationship between FDI inflows in India and corruption distance with the host countries. The better the control of corruption, the more FDI is India expected to receive. The results have important suggestions for policymakers.

Review of Literature

FDI is one probable choice when the firms want to do international expansion (Harrison, 2003). ‘FDI encourages the transfer of technology and know-how by creating direct, stable long-lasting links between countries’ (OECD, 2014). FDI inflows are particularly important for developing and emerging economies. This is for the reason that as compared to domestic investment, FDI provides more financial resources and contributes more significantly to nation’s economic growth (Borenzstein et al., 1998). ‘The transfer of intangible assets, such as knowledge, technology, skills and management know-how through FDI helps in boosting productivity and growth’ (Wong & Adams, 2002). Alam and Ali Shah (2013) posited that factors such as market size, labour costs and the quality of infrastructure are important for attracting FDI.

Cost of Doing Business Abroad and the Liability of Foreignness

The theoretical concept of CDBA was first introduced by Professor Stephen Hymer in his 1970/1976 theses. Hymer defined CDBA as the additional cost faced by an MNE over local firms in the foreign market (Hymer, 1976). Depending on the industry and host country context, the liability of foreignness may be due to simple factors such as greater travelling and transportation costs, coordination costs, firm’s lack of local market knowledge or because of more covert issues such as lack of information networks, political sway in the host nation or the foreign company’s incapacity to appeal to nationalistic customers (Hymer, 1976; Zaheer, 1995). It could also arise in the form of lack of legitimacy for the foreign firms due to specific factors in the home country. Whatever the source, the liability of foreignness means that an MNE faces higher costs than local firms in the host market, which ceteris paribus, leads to lower profitability and lower chances of survival of the foreign firm in host country (Zaheer, 1995).

The terms ‘CDBA’ and ‘liability of foreignness’ are not the same, even though they have been used interchangeably (Zaheer, 2002). The cost of doing business is a broad notion that includes the cost of production, marketing and distribution, that is, economic activity-based costs because of the physical distance as well as the social cost of conducting business abroad known as the liability of foreignness. Liability of foreignness is therefore a key factor of the cost of doing business overseas that arises from the newness, relational and unfair dangers that multinationals face in the overseas market (Eden & Miller, 2004). As the economic activity-based cost is finite and can be measured and controlled for by the MNE, it is the social cost of doing business as represented by liability of foreignness that concerns the firms while investing abroad. This article, therefore, focused on the liability of foreignness faced by investors of FDI in India.

Institutional Theory

Institutions are well-defined as ‘the rules of the game in a society or, more formally, are the humanly devised constraints that shape human interaction’ (North, 1990). Scott (1995) described institutions as ‘cognitive, normative and regulative structures and activities that provide stability and meaning to human behaviour’. Organisations are a part of the larger institutional environment, and institutional theory emphasises how influential institutions can be in getting such organisations to adopt procedures, rules and structures that are in line with their preferences (Meyer & Rowan, 1977), thereby imposing isomorphic behaviour on foreign firms (DiMaggio & Powell, 1983). The institutions differ between the countries and greater the institutional distance (defined as ‘the degree of difference/similarity between the regulatory, cognitive and normative institutions of two countries’ (Kostova, 1996), the greater is the pressure on MNE for local responsiveness (Doz, 1980; Prahalad & Doz, 1987) and higher the liability of foreignness (Zaheer, 2002). Higher institutional distance exerts greater pressure on MNEs to adapt their strategies to comply with local institutions (Kostova & Roth, 2002). Kostova and Zaheer (1999) argued that liability of foreignness was more affected by informal institutions in the form of normative and cognitive institutions than by formal regulatory institutions. The normative institutions imply ‘social norms, values, beliefs and assumptions about human nature and human behaviour that are socially shared and are carried by individuals’ (Kostova, 1996). An example of an informal normative institution is public sector corruption (Calhoun, 2002; El Said & McDonald, 2002). In this context, ‘corruption distance’ can be viewed as a unique aspect of normative institutional distance (Godinez & Ling, 2015).

Corruption Distance and Its Effect on FDI

Corruption is defined narrowly as the abuse of public office for personal gain (Roy & Oliver, 2009). Corruption in a host country may decrease a company’s expected profitability of an investment project. These costs of corruption can be seen as additional costs of doing business and are sometimes referred to as ‘additional tax on profits’. Hence, firms will take into account the level of corruption in the host country in consideration before investing there(Al-Sadig, 2009). It is an informal institutional constraint where bribery is socially acc eptable. It is the social cost of doing business as represented by liability of foreignness that concerns the firms while investing abroad. This article, therefore, focuses on the liability of foreignness faced by investors of FDI in India.

Studies have shown that it is not solely the host nation’s institutional quality (Baniak et al., 2003; Chen et al., 2010; Kostova, 1996), but also that of home country that influences the decision of making an investment in a highly corrupt foreign location (Habib & Zurawicki, 2002). Empirical studies on level of corruption in a country and FDI have not found consistent results—with some authors reporting that high level of corruption deterred the flow of FDI into country (Cuervo-Cazurra, 2006; Smarzynska & Wei, 2000; Woo & Heo, 2009) while others have reported that it can have a positive impact as it enabled speedy transactions in countries with stringent and time-consuming regulations (Egger & Winner, 2005; Huntington, 1968; Leff, 1964). ‘One possible explanation for the inconsistency in these studies is that not all foreign investors are equal and therefore are not equally affected by corruption abroad’ (Cuervo-Cazurra, 2006). ‘Another explanation is that foreign investors are not affected by the level of corruption of the host country per se but by the difference in the levels of corruption between the home and host countries’ (Habib & Zurawicki, 2002). Depending on how corrupt their home nation is, investors may be affected differently by corruption in the host country. Firms that deal with domestic corruption might face less pressure from threats to their legitimacy because they have learnt to deal with this corruption (Cuervo-Cazurra, 2006). This implies that a home country with a lesser level of corruption as compared to a more corrupt host country (negative corruption distance) would be affected by corruption in the host country, while a home country which has greater corruption levels than host location (positive corruption distance) would not be (Godinez & Ling, 2015). ‘Lower corruption distance (between parent home and host countries) and higher perceived corruption (in host country) are positively related, and mutually reinforcing, when considering a foreign subsidiary’s propensity to formally contract with government-sponsored financial institutions’ (White et al., 2022).

Habib and Zurawicki (2002) used ‘the corruption distance (CD) as a measure of the absolute difference in the corruption levels between the source and the host country’. Wu (2006) used this and according to him ‘it is CD which affects the behaviour of foreign investors rather than the level of corruption in the host country’. As per Wu (2006), ‘the negative effect of CD on a corrupt country seeking FDI from a less corrupt country is stronger than the effect would be for a transparent country looking for FDI from a more corrupt country’. Hence, we could say that there is an asymmetric impact of CD on FDI. Qian and Sandoval-Hernandez (2016), also, ‘found an asymmetric influence between corruption distance and FDI’. Adamoglou et al. (2022) found that

MNEs presence reduces the level of corruption in the seventeen emerging economies’ studied during 2012–2019. ‘The larger the corruption distance, more likely the firms will invest. Additionally, it was found that policy uncertainty has a negative moderating effect on the relationship between corruption distance and FDI location choice. (Rodina, 2022)

There is insufficient and inconclusive research on the impact of corruption on FDI flow. Al-Sadig (2009) and Hakkala et al. (2005) found a positive influence of corruption on FDI, while Cuervo-Cazurra (2008), Dahlström and Johnson (2007), Drabek and Payne (2002), Habib and Zurawicki (2002), Shleifer and Vishny (1993), Smarzynska and Wei (2000) and Wei (1997, 2000a, 2000b) suggested a negative influence of corruption on FDI.

Research Objective

The goal of the current study was to determine whether there is any long-term association between corruption distance and FDI inflows in India as the results on the relationship between corruption and FDI inflows in a country remain inconclusive.

Data and Methodology

Sample

We examined the relationship between corruption distance between the home country of the investing firm (or investor country) and India (which is the host country in this study), and FDI inflows in India for the period 2008–2020—time period because of accessibility to data on all the required variables. The cut-off point of year 2020 was also suitable as the global FDI flows collapsed post 2020 as a result of the COVID-19 pandemic.

Inward FDI in India has shown consistent increase since the onset of economic reforms in the year 1991. From the moderate amount of USD 14 billion during the 1990s, inward FDI in India has grown remarkably to be recorded at USD 160 billion during the decade ending 2010 and USD 436 billion in the decade ending 2020 (UNCTADSTAT, n.d.). The third largest economy in PPP terms, India is an attractive investment destination for the market seeking FDI. This increasing FDI inflows in India despite the country’s consistent low score on the control of corruption dimension published as part of the World Governance Indicator (WGI) by the World Bank, made it an interesting context to examine the research objective of this study.

Data Source and Description

As per WGI, control of corruption explains the extent to which public power is exploited for private gain, covering both petty and grand forms of corruption, and ‘capture’ of the state by elites and private interests (World Bank, n.d.). The value of the variables ranges from –2.5 to 2.5 where higher values indicate better control of corruption in the country.

Using this data, we calculated the control of corruption distance using the following formulae:

Control of Corruption value in the home country of the investing firm (or investor country)it – Control of Corruption value in Indiat

where i refers to the home countries of the investing firms (i = 1 to 11) and t refers to 2008–2020.

Methods

The presence of a long-run relationship between the variables was tested by applying the Cointegration tests. Some conditions need to be fulfilled to use the panel cointegration models. First, we have to examine the nature of stationarity of the panel variables. This was done with the help of unit root tests. There are various methods for panel unit root testing, including. Levin et al. (2002) test and Kyung et al. (2003) test, Fisher-ADF test (Maddala & Wu, 1999) and Fisher–PP test (Choi, 2001). Each of these presumes the presence of unit root in the null hypothesis. The acceptance of the null hypothesis means the data was non-stationary. In this study, we used the Fisher type Phillips–Perron Unit Root test that allowed for individual unit root processes.

Depending on the nature of stationarity of the variables, the appropriate cointegration tests were used to examine if there existed any long-term relationship between the considered variables. There are number of ways to test for panel cointegration, just as there are for panel unit root tests. These include the Johansen Fisher (Maddala & Wu, 1999), the Pedroni (1999) test and the Kao (1999) test. We used panel ARDL method in this study as our two variables were found to be integrated in different orders (as shown in the results section).

Results

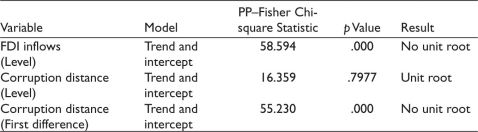

Unit-root Test (Fisher Type Phillip–Perron Unit Root Testing)

As can be seen from Table 1, the null hypothesis of unit root for FDI inflows was rejected at its level (p < .01), suggesting that the variable was stationary. In other words, FDI inflows were integrated at its level, that is, I (0). The variable corruption distance, on the other hand, was found to be stationary only in its first difference. The null hypothesis of unit root could not be rejected at its level (p > .10) but was significantly rejected at the first difference of the variable (p < .01). In other words, the variable corruption distance is integrated of order 1, that is, I (1).

Table 1.Results of Phillip–Perron Unit Root Test.

Source: Stata computations based on collected data.

Test of Cointegration—Panel Autoregressive Distributed Lag

Since two variables are integrated of different orders, FDI-I (0) and Corruption distance-I (1), Panel ARDL, that is, ARDL method can be used to find out if the two variables are cointegrated with each other. We selected the optimal lag using automatic lag length selection based on Akaike Information Criteria. As per the criteria, the selected model was ARDL (2,1). The findings are presented in Table 2. The p value of corruption distance was less than 0.01. The null hypothesis of no cointegration was rejected at 1% level of significance. This suggests that there exists a long-term relationship between FDI inflows in India and corruption distance.

Table 2.Results of Panel ARDL.

Source: Stata computations based on collected data.

The negative and significant coefficient of cointegration coefficient suggests that any short-term disequilibrium in the relationship adjusts at the rate of 38.1% per year.

Discussion of Findings

The results of panel ARDL revealed that there is a long-term relationship between FDI inflows in India and the corruption distance between India and the investor country. The greater (lesser) the control of corruption in the host country (India, in our case), the more (less) FDI inflows it is expected to receive. This suggests that the control of corruption, which is an important element of the institutional environment in a country, adds to the location advantages that a country has to offer. Investors, in general, are attracted to invest in countries having stronger institutions where the value of their investment is safe and the cost of doing business is less. While investing in such countries, it is easier for the foreign firms to deal with the liabilities of foreignness.

Policy Implications

Our findings provide a robust empirical support to the notion of institutional difference (or distance) as an important explanation of FDI decisions and therefore contribute to the institutional theory. We also contribute to the institutional theory by looking at often ignored, informal or normative pillars of institutions (Liedong et al., 2020).

As FDI constitutes a vital source of finance for developing and emerging economies, the findings provide a strong case for Indian policymakers to focus on devising effective checks and balances to combat corruption. Furthermore, the importance of FDI is restricted not only to the financial resources it brings in but also to other benefits such as increased employment, advanced technological and managerial skills, and productivity benefits to the host countries. An increased level of corruption not only deters FDI inflows but also the confidence of the foreign direct investors to transfer advanced technological and managerial knowledge and skills to the host country. As a result of which, the potential benefits of FDI may be lost. Hence, better control of corruption can result in increased FDI inflows and the associated benefits.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Adamoglou, X., Kounnou, V., Hajidimitriou, Y., & Kyrkilis, D. (2022). MNEs institutional entrepreneurship: The effect on corruption. An analysis of emerging economies. In P. Sklias, P. Polychronidou, A. Karasavvoglou, V. Pistikou & Nikolaos (Eds), Business development and economic governance in Southeastern Europe (pp. 109?132). Springer.

Alam, A., & Ali Shah, S. (2013). Determinants of foreign direct investment in OECD member countries. Journal of Economic Studies, 40(4), 515?527.

Al-Sadig, A. (2009). The effects of corruption on FDI inflows. Cato Journal, 29(2), 267?294.

Baniak, A., Cukrowski, J., & Herczyski, J. (2003). On the determinants of foreign direct investment in transition economies. Problems of Economic Transition, 48(2), 6?28.

Borenzstein, E., De Gregorio, J., & Lee, J.-W. (1998). How does foreign direct investment affect economic growth. Journal of International Economics, 45(1), 115?135.

Calhoun, C. (2002). Imagining solidarity: Cosmopolitanism, constitutional patriotism and the public sphere. Public Culture, 14(1), 147?172

Chen, C. J., Huang, J. W., & Hsiao, Y. C. (2010). Knowledge management and innovativeness: The role of organizational climate and structure. International Journal of Manpower, 31(8), 848?870,

Choi, I. (2001). Unit root tests for panel data. Journal of International Money and Finance, 20(2), 249?272.

Cuervo-Cazurra, A. (2006). Who cares about corruption Journal of International Business Studies, 37(6), 807?822

Cuervo-Cazurra, A. (2008). Better the devil you don?t know: Types of corruption and FDI in transition economies. Journal of International Management, 14(1), 12?27.

Dahlström, T., & Johnson, A. (2007). Bureaucratic corruption, MNEs and FDI [Working Paper Series in Economics and Institutions of Innovation from Royal Institute of Technology, No 82]. Centre of Excellence for Science and Innovation Studies.

DiMaggio, P. J., & Powell, W. W. (1983). The Iron cage revisited: Institutional isomorphism and collective rationality in organisational fields. American Sociological, 48, 147?160.

Doz, Y. (1980). Strategic management in multinational companies. Sloan Management Review, Winter, 27?46.

Drabek, Z., & Payne, W. (2002). The impact of transparency on foreign direct investment. Journal of Economic Integration, 17(4), 777?810.

Eden, L., & Miller, S. R. (2004). Distance matters: Liability of foreignness, institutional distance and ownership strategy. Advances in International Management, 16(4), 187?221.

Egger, P., & Winner, H. (2005). Evidence on corruption as an incentive for foreign direct investment. European Journal of Political Economy, 21(4), 932?952.

El, S. H., & McDonald, F. (2002). Institutional reform and entry mode by foreign firms: The case of Jordan. Journal for Institutional Innovation, Development and Transition, 6, 76?88.

Ghosh, C., Narayan, P. C., Prassad, R. S., & Thenmozhi, M. (2022). Does corruption distance affect cross-border acquisitions Different tales from developed and emerging markets. European Management Journal, 28(2), 345?402.

Godinez, J. R., & Ling, L. (2015). Corruption distance and FDI flows into Latin America. International Business Review, 24(1), 33?42.

Habib, M., & Zurawicki, L. (2002). Corruption and foreign direct investment. Journal of International Business Studies, 33(2), 291?307.

Hakkala, N., Norbäck, P. J., & Svaleryd, H. (2005). Asymmetric effects of corruption on FDI: Evidence from Swedish multinational firms [Working Paper No. 641]. The Research Institute of Industrial Economics.

Harrison, M. (2003). Can corrupt countries attract foreign direct investments A comparison of FDI inflows between corrupt and non-corrupt countries. International Business & Economics Research Journal, 2(9), 93?100.

Huntington, S. P. (1968). Political order in changing societies. Yale University Press.

Hymer, S. H. (1976). The international operations of national firms: A study of direct foreign investment. MIT Press

Kao, C. (1999). Spurious regression and residual-based tests for cointegration in panel data. Journal of Econometrics, 90, 1?44.

Kostova, T. (1996). Success of the transnational transfer of organizational practices within multinational companies. University of Minnesota

Kostova, T., Beugelsdijk, S., Scott, W. R., Kunst, V. E., Chua, C. H., & van Essen, M. (2020). The construct of institutional distance through the lens of different institutional perspectives: Review, analysis, and recommendations. Journal of International Business Studies, 51(4), 467?497.

Kostova, T., & Roth, K. (2002). Adoption of an organizational practice by subsidiaries of multinational corporations: Institutional and relational effects. Academy of Management Journal, 45, 215?223.

Kostova, T., & Zaheer, S. (1999). Organizational legitimacy under conditions of complexity: The case of the multinational enterprise. Academy of Management Review, 24, 64?81.

Kyung, S, Pesaran, I. M., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115(1), 53?74

Leff, N. H. (1964). Economic development through bureaucratic corruption. American Behavioral Scientist, 8, 8?14.

Levin, A., Lin, C. F., & Chu, C. S. J. (2002). Unit root tests in panel data: asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1?24.

Liedong, T. A., Peprah, A. A., Amartey, A. O., & Rajwani, T. (2020). Institutional voids and firms? resource commitment in emerging markets: A review and future research agenda. Journal of International Management, 26(3). https://doi.org/10.1016/j. intman.2020.100756

Maddala, G. S., & Wu, S. (1999). A comparative study of unit root tests with panel data and a new simple test. Oxford Bulletin of Economics and Statistics, 61(S1), 631?652.

Malanski, L. K., & Póvoa, A. C. S. (2021). Economic growth and corruption in emerging markets: Does economic freedom matter International Economics, 166, 58?70.

Meyer, J. W., & Rowan, B. (1977). Institutionalized organizations: Formal structure as myth and ceremony. American Journal of Sociology, 83, 340?363.

Nayyar, R., Mukherjee, J., & Varma, S. (2021). Institutional distance as a determinant of outward FDI from India. International Journal of Emerging Markets, 17(10), 2529?2557.

North, D. (1990). A transaction cost theory of politics. Journal of Theoretical Politics, 2(4), 355?367.

OECD. (2014). FDI statistics and data. https://www.oecd.org/daf/inv/investment-policy/fdistatisticsanddata-frequentlyaskedquestions.htm

Pedroni, P. (1999). Critical values for cointegration tests in heterogeneous panels with multiple regressors. Oxford Bulletin of Economics and Statistics, 61, 653?670.

Pekarskiene, I., & Susniene, R. (2015). Features of foreign direct investment in the context of globalization. Procedia-Social and Behavioral Sciences, 213, 204?210.

Prahalad, C. K., & Doz, Y. (1987). The multinational mission: Balancing local demands and global vision. The Free Press.

Qian, X., & Sandoval-Hernandez, J. (2016). Corruption distance and foreign direct investment. Emerging Markets Finance and Trade, 52(2), 400?419.

Ramachandran, J., & Pant, A. (2010). The liabilities of origin: An emerging economy perspective on the costs of doing business abroad. Advances in International Management, 23. https://doi.org/10.1108/S1571-5027(2010)00000230017

Reserve Bank of India. (2021). Foreign direct investment flows to India: Country-wise and industry-wise?Annual report. https://m.rbi.org.in/Scripts/AnnualReportPublications.aspxId=1336

Rodina, Z. (2022). Corruption distance and FDI location choice. Victoria University of Wellington. https://openaccess.wgtn.ac.nz/articles/thesis/Corruption_distance_and_FDI_ location_choice_/21191554

Roy, J-P., & Oliver, C. (2009). International joint venture partner selection: The role of the host-country legal environment. Journal of International Business Studies, 40(5), 779?780.

Scott, W. R. (1995). Institutions and organisations: Ideas, interests and identities. SAGE Publications.

Shleifer, A., & Vishny, R. (1993). Corruption. Quarterly Journal of Economics, 108(3), 599?617.

Smarzynska, B., & Wei, S. J. (2000). Corruption and composition of foreign direct investment: Firm level evidence [Working Paper No. 7969]. National Bureau of Economic Research.

UNCTADSTAT. (n.d.). Foreign direct investment: Inward and outward flows and stock, annual.https://unctadstat.unctad.org/wds/TableViewer/tableView.aspxReportId= 96740

United Nations. (2021). World investment report 2021: Investing in sustainable recovery. https://unctad.org/system/files/official-document/wir2021_en.pdf

Wei, S.-J. (1997). Why is corruption so much taxing than tax Arbitrariness kills [Working Paper No. 6255]. National Bureau of Economic Research.

Wei, S.-J. (2000a). How taxing is corruption on international investors The Review of Economics and Statistics, 82(1), 1?11.

Wei, S.-J. (2000b). Local corruption and global capital flows. Brooking Papers on Economic Activity, 31, 303?354.

White III, G. O., Chintakananda, A., & Rajwani, T. (2022). Seeds of corruption The contingent role of ties to politicians and foreign subsidiary relations with government-sponsored financial institutions. British Journal of Management. https://doi.org/10.1111/1467-8551.12589

Wong, Y. C., & Adams, C. (2002). Trends in global and regional foreign direct investment flows [Paper presentation]. Conference on Foreign Direct Investment. International Monetary Fund and State Bank of Vietnam.

Woo, J. Y., & Heo, U. (2009). Corruption and foreign direct investment attractiveness in Asia. Asian Politics & Policy, 1(2), 223?238.

World Bank. (n.d.). Control of corruption. http://info.worldbank.org/governance/wgi/pdf/cc.pdf?

Wu, S.-Y. (2006). Corruption and cross-border investment. Journal of Comparative Economics, 34(4), 839?856.

Zaheer, S. (1995). Overcoming the liability of foreignness. The Academy of Management Journal, 38(2), 341?363.

Zaheer, S. (2002). The liability of foreignness, redux: A commentary. Journal of International Management, 8(3), 351?358.

?