Review of Professional Management

Search

Search

Swathy Krishna1 and Shacheendran V2

and Shacheendran V2

1 Department of Management Studies, Kannur University, Palayad, Kannur District, Kerala, India

2 GPM Government College, Manjeshwaram, Kasaragod District, Kerala, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Consumption tax evasion (CTE) is an ethical dilemma that can enlarge the presence of the shadow economy. The empirical literature mainly focused on the ethical dimension of the business community, thus there is insufficient literature related to the ethical decision-making process on the consumer’s side. So, the present study attempts to explore the ethical decision-making process of consumers regarding CTE. The study used three major components of Jones’s Issue Contingent Model to study the consumer’s ethical decision-making regarding CTE. The study proposes a conceptual model by linking idealism, relativism, religiosity and attitude with the three components of the issue contingent model. The result of the study was based on primary data collected from consumers in the Kerala State. The data obtained was examined using the PLS-SEM technique which confirms the influence of idealism, relativism and attitude on the moral recognition of consumers regarding CTE. The result also concludes that moral recognition leads to moral judgement, which in turn, plays a vital role in inculcating moral compliance intention in the minds of consumers.

Consumption tax evasion, ethical decision-making, moral intention, moral recognition

Introduction

Raising government revenue is an essential priority for sourcing public expenditure. However, the revenue base of the Indian economy has been weakened by the accelerated growth of the parallel economy (Sarkar, 2010). Tax evasion has become a major roadblock to the smooth functioning of the administrative system. Feige (1994) describes the shadow economy as the activities contributing to the GDP but not properly recorded. Consumption tax evasion (CTE) is an integral component of the parallel economy. The presence of tax evasion not only affects the government’s revenue performance but also degrades the overall welfare of the economy. This challenging situation creates a need for intense effort on the part of the government to minimise the tax gap. But, the rigorous efforts of the administrative tiers are often outwitted by various forms of informal schemes adopted by businesses to reduce tax obligations (Saxunova & Szarkova, 2018).

Over the years, the size of the shadow economy has shown an upward trend (Schneider, 2003). The negative externalities resulting from the tax evading practices will hinder the progress of the economies (Menon, 2019). There are several studies which have thrown insights into the association between ethics and tax evasion (Culiberg & Bajde, 2014; Drogalas et al., 2018; McGee et al., 2008; Seralurin & Ermawati, 2019). But the empirical results focused on the side of taxpayers and not on the consumers’ perspectives. So, the present study emphasises consumers’ perspectives with respect to CTE. CTE is a global phenomenon that occurs when consumers use cash with the deliberate intention of reducing tax obligations (Culiberg & Bajde, 2014). Empirical findings indicate various forms of economic, moral, psychological and social consequences related to tax evasion. CTE practices grant the evaders an unfair advantage over the business which obediently comply with the legal requirement of the tax system. This unfair implication can be avoided when consumers perform their part of moral duties by asking for invoices, which in turn, will prevent the businesses from evading taxes.

The empirical results of studies corroborate the relevance of moral values in controlling non-compliance behaviour (Badaracco & Webb, 1995; De George, 1987; Jones, 1991; Stark, 1993). An individual’s moral beliefs can govern the moral decision-making process, that is, to decide whether to take part in CTE or not. Empirical results show that various factors influence tax compliance, which includes consumer ethics (Fukukawa, 2002), tax morality (Maciejovsky et al., 2012), tax ethics (Kirchler et al., 2008), but, only limited attention has been given to the consumer decision-making perspective. So, to fill this literature gap the present study examines the ethical decision-making perspective of consumers regarding CTE.

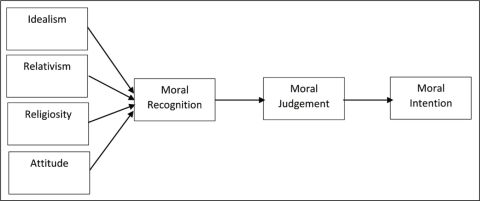

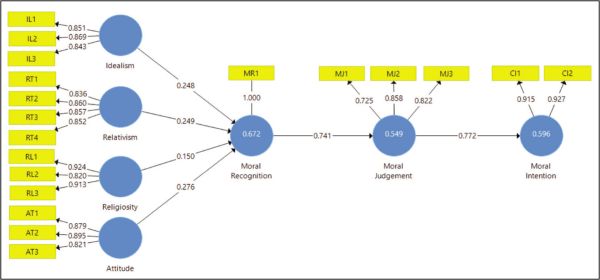

Empirical studies identified a significant association between religiosity and tax compliance (Ababio & Mangueve, 2021; Carsamer & Abbam, 2020; Srivastava et al., 2018). Religious considerations can subdue non-compliance behaviour (Torgler & Murphy, 2004). Furthermore, the influence of religiosity on compliance behaviour is highlighted in a study conducted by Abdullah and Sapiei (2018). Similarly, evidences show that attitude can mould an individual’s compliance behaviour. Hofmann et al. (2008) discuss the role of attitude towards government in promoting voluntary tax compliance. An Individual’s perception of government can enhance compliance (Wahl et al., 2010) since the ability of the government to meet the public requirements can enhance the compliance rate. Feld and Frey (2007) assert that tax compliance is moulded by creating a positive attitude towards the administrative system. Thus, the study further explored the role of religiosity and attitude towards government in affecting the ethical decision-making process regarding CTE (Figure 1).

Figure 1. Conceptual Model.

Source: Jone’s Issue Contingent Model (1991).

Literature Review and Hypotheses Development

The concept of tax compliance has been explored by authors from different dimensions. Some studies used the theory of planned behaviour (Bobek & Hatfield, 2003; Taing & Chang, 2021), while some studies relied on the theory of reasoned action to investigate more about compliance behaviour (Bidin et al., 2014; Hessing et al., 1988). The study employs an extended Jones issue contingent model to gain insights into the ethical decision-making process. The ethical decision-making process begins with moral recognition, which is followed by moral judgement, moral intention and finally leading to moral compliance. Consumers’ ethical decision-making processes related to CTE have received little attention up to this point. The moral decision-making process constitutes a well-defined phase (Hunt & Vitell, 1986), where the factor of moral recognition precedes a person’s moral judgement (Jones, 1991). Moral recognition is the acknowledgement of the moral responsibilities towards common welfare (Hollingworth & Valentine, 2015). Rest (1986) identified the need for morally recognising an issue, followed by establishing a moral judgement, then by moral intention and for finally resulting in moral behaviour. Similarly, Jones (1991) highlights the need to recognise a moral issue for the development of a moral judgement towards a well-defined situation. The recognition of a moral concern can influence the moral behaviour by influencing an individual’s moral judgement, which in turn affects moral intention. O’Fallon and Butterfield (2012) identified various variables attributing to the ethical decision-making process. The study found that knowledge level, situational aspects and issues-based factors strongly influence ethical decision-making. While there also exist studies that found a negative association between moral judgement and moral intentions (Pan & Sparks, 2012). Moral judgement is a major construct under the Jones-issue-contingent model. Various studies have found a significant association between moral judgement and moral intentions (Culiberg & Bajde, 2014; Culiberg & Mihelic, 2016; Ferrell et al., 1989; Hofmann et al., 2007; Yang & Wu, 2009). Valentine and Rittenburg (2004) extended an investigation to study international ethical compliance among business professionals and confirmed the existence of a positive association between tax judgement and tax compliance among taxpayers. With respect to the findings of the previous studies, the study proposes that:

H1: Moral recognition positively influences moral judgement regarding Consumption Tax Evasion

H2: Moral judgement positively influences moral intentions regarding Consumption Tax Evasion

Ethical Ideologies

The moral beliefs of an individual can influence the moral decision-making process. Numerous studies have found a strong association between ethical ideologies and ethical behaviour (Culiberg & Bajde, 2014; Forsyth, 1980; Henderson & Kaplan, 2005). The two major determinants of ethical ideology are idealism and relativism (Forsyth, 1980; Wiggins, 1990). Sidani et al. (2014) investigated and found the role of ethical ideologies, that is, idealism and relativism in bringing down tax evasions. According to Forsyth (1980), the concept of idealism gives emphasis to others’ welfare dimension. The empirical study highlighted the relevance of idealism in fostering positive outcomes in the ethical decision-making process (Henle, 2005). The higher an individual’s level of idealism greater will be the level of ethical recognition. Meanwhile, relativism refers to a situation where other people’s perspectives are also considered along with the universally recognised principles. A relativist’s perspective depends on the universal principles and the circumstances which a person is put into. Relativism deals with the situational ethics rather than relying solely on the absolute truth (Forsyth et al., 2008).

According to Hunt and Vitell (1986), the first phase in the ethical decision-making process is the development of ethical or moral recognition. Existing literature confirms that moral recognition can enhance the chance of resolving ethical or moral concerns (Hunt & Vitell, 1986). Moral recognition is influenced by various factors to varying degrees. These factors include relativism (Culiberg & Bajde, 2014; Harman, 1978) and idealism (Bateman et al., 2013; Culiberg & Bajde, 2014; Henle, 2005). Based on the results obtained by the above studies, the study proposes the following hypotheses:

H3: Idealism positively influences moral recognition of the consumers regarding Consumption Tax Evasion

H4: Relativism positively influences moral recognition of the consumers regarding Consumption Tax Evasion.

Religiosity

Religious perception shapes the general understanding of an individual towards what can be considered as moral or not (Weaver & Agle, 2002). Consumers can indirectly contribute to the economy by reducing the non-compliance of the business concerns and by preventing the business entity from becoming a part of CTE. Religion can shape consumer perception by encouraging an individual to abstain from tax-evading practices (Srivastava et al., 2018). However, there are also studies that found no significant difference in the ethical behaviour of religious or non-religious individuals (Spilka et al., 2003). Similarly, Agle and Buren (1999) identified a weak association between religious beliefs and tax compliance behaviour (Abdullah & Sapiei, 2018; Eiya et al., 2016; Mohdali & Pope, 2014). While Srivastava et al. (2018) confirmed the influence of religiosity on the moral recognition concerning CTE. Based on the findings of the previous studies, the study hypothesis:

H5: Religiosity positively influences moral recognition of the consumers regarding Consumption Tax Evasion

Attitude

Attitude plays a vital role in influencing the tax behaviour of consumers (Alabede et al., 2011; Guerra & Harrington, 2018; Night & Bananuka, 2019; Palil & Mustapha, 2011; Sadress et al., 2019; Webley et al., 2001). Skitka et al. (2015) state that peoples’ attitude influences their moral convictions. Many empirical studies have found a strong association between perception towards government and taxpayers’ compliance behaviour (Cummings et al., 2005; Feld & Frey, 2007; Modugu & Anyaduba, 2014; Torgler, 2007). Srivastava et al. (2018) ascertain the relevance of trust in the administrative system for influencing the moral recognition, by acting as a mediator for tax compliance. Therefore, the study proposes that:

H6: Attitude towards the government positively influences moral recognition of the consumers regarding Consumption Tax Evasion.

Research Methodology

Sample and Procedures

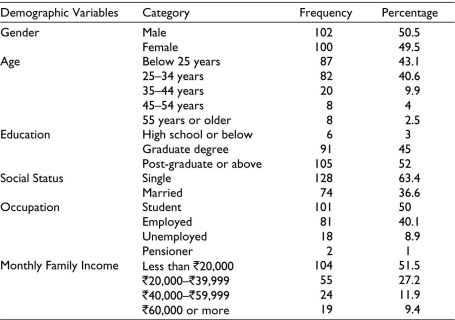

A quantitative analysis was performed based on primary data collected using a survey questionnaire. The study was conducted among consumers in the Kerala State. The data were collected from the respondents using an online survey. To avoid possible errors in the survey instrument, a pilot study was conducted among 30 respondents. The result of the preliminary study showed Cronbach’s alpha for each item under the construct scale was greater than 0.7, indicating the construct reliability and making the instrument suitable for studying consumers’ ethical decision-making process regarding CTE. The responses were gathered using Google Forms using convenience sampling. A total of 250 questionnaires were distributed, however, 202 fully completed questionnaires were obtained from the respondents. A qualifying question was used to identify the individuals who come within the context of the study. In line with the study objectives, an individual who makes payment without receiving receipts may intentionally or unintentionally become part of CTE and thus, becomes the target population of the study. The questionnaire was divided into two sections, the initial section comprised questions regarding the demographic characteristics of the respondents, followed by dimensions indicated in the proposed model. Table 1 reveals the demographic characteristics of the respondents. Regarding the demographic information, the respondents were asked about their gender, age, education, social status, occupation and monthly income. In the present study, 50.5% of respondents were males and 49.5% were females. The majority of the respondents belonged to the age categories below 35 years old, that is, 43.1% under the group. Below 25 years and 40.6% under the group 25–34 years. The highest (52%) had the educational qualification of Post Graduate or above, followed by 45% with Graduate degree. Apart from these, most of the respondents were students and the majority had a monthly family income of less than `20,000 (51.5%).

Table 1. Demographic Information.

Measures

The study used standardised scales to examine the ethical decision-making process regarding CTE. The term CTE here refers to the situation where the goods or services are acquired without receipts (i.e., paying without receipts). Structured questionnaires contained the items represented on a five-point Likert scale ranging from Strongly Disagree-1 to Strongly Agree-5. Moral recognition was measured using a single statement indicating the ethical scenario, which was developed by Singhapakdi et al. (1996). Similar approaches, involving a single item to study the ethical decision-making process have been used in the previous studies (Culiberg & Bajde, 2014; Srivastava et al., 2018). To measure moral judgement, the study used a multidimensional scale involving three items (Robin et al., 1996). Moral Judgement was measured following the methodology outlined by Cherry and Fraedrich (2002), using a 3-item scale. The constructs idealism and relativism were measured using the scale developed by Forsyth (1980). The construct idealism was studied using 3-item scale and relativism by using 4-item scale, the same elements were used in a study conducted by Culiberg and Bajde (2014). Religiosity was measured using 3-item taken from a scale designed by Worthington et al. (2003). The construct attitude towards the government was measured using the 3-item scale (Frey & Weck-Hanneman, 1984). Several other studies have employed this attitude scale to measure tax compliance (Srivastava et al., 2018; Taing & Chang, 2021).

Data Analysis

The study employed partial least square structural equation modelling (PLS-SEM) to examine the conceptual model. PLS-SEM is a non-parametric that can accommodate data distributions lacking the characteristics of normality. And also, PLS-SEM only requires a lesser number of samples compared to the CB-SEM method (Hair et al., 2011). Smart PLS 3 software package was used to examine the relation stated in the conceptual model. Bootstrapping was performed using 5,000 samples (at 95% confidence interval) for corroborating the result obtained using the original sample in PLS-SEM.

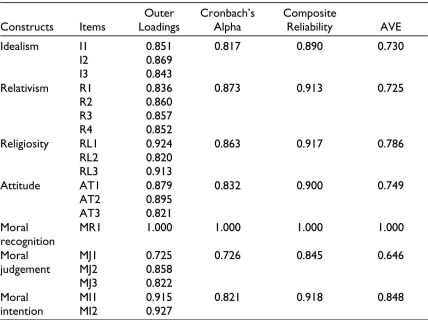

The reliability of the constructs under the measurement model was determined using Cronbach’s alpha and composite reliability. As shown in Table 2, the construct reliability is ensured when Cronbach’s alpha is greater than 0.7 (Hair et al., 2019). Similarly composite reliability above 0.7 is considered to be good, indicating internal consistency of the data. The analysis provides strong confirmation of internal consistency for all the constructs specified.

Table 2. Measurement Model.

In the measurement model, the convergent validity was analysed using average variance extracted (AVE). The values of AVE greater than 0.5 come under the acceptable limit for ensuring the validity of the constructs (Fornell & Larcker, 1981). The result confirms the acceptability limit since all the constructs had AVE greater than 0.5.

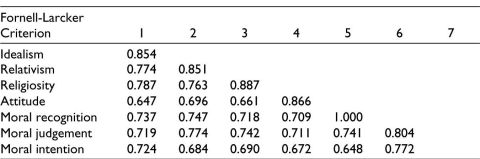

Fornell and Larcker (1981) guidelines were followed that were used to assess the discriminant validity. The square root of AVE was compared with the correlation between the constructs for computing discriminant validity. The results obtained for the constructs meet the acceptance criteria, thus indicating strong discriminant validity among the individual constructs (Table 3). The measurement model demonstrated good reliability and validity making, the model fit for further analysis.

Table 3. Discriminant Validity.

Structural Model

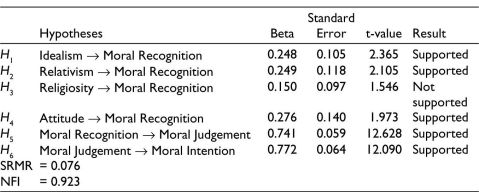

The path loadings and significance level were used for making an assessment of the structural model. From Table 4, it is evident that there exists a strong relation between ethical ideologies (i.e., idealism and relativism) and moral recognition. Idealism is found to be significant at p < .05(β = 0.248, t = 2.412) and relativism is significant at p < .05 (β = 0.249, t = 2.112). Moreover, the relationship between attitude towards government and moral recognition is also significant at p < .05 (β = 0.276, t = 1.974). Thus, H1, H2, H4 were accepted with the t-statistics greater than 1.96. However, religiosity did not significantly influence the moral recognition of the consumers towards CTE, thus H3 was rejected (β = 0.150, t = 1.546) (Figure 2).

Table 4. Path Coefficient.

Figure 2. Path Coefficient.

The PLS-SEM method lacks an established goodness-of-fit measure, and the indices for measuring model fitness under PLS-SEM approach are still evolving. In the present study, the model fitness was assessed using the standardised root mean square residual (SRMR) and the normed fit index (NFI). A good model fit for SRMR is typically indicated by a value of 0.08 or less (Hu & Bentler, 1999). In this case, the SRMR value obtained, SRMR = 0.076, falls within the acceptable threshold. Similarly, an NFI value of 0.90 or above is considered indicative of good model fit (Bentler, 1990), and the obtained value of 0.923 confirms that the model fits well.

A strong relationship between moral recognition and moral judgement towards CTE is confirmed (p < .001, β = 0.741, t = 12.610), thereby indicating the acceptance of H5. Similarly, the value of the path coefficient confirms that moral judgement is positively associated with moral intention (p < .001, β = 0.772, t =12.105), therefore H6 is supported.

Discussion and Conclusion

CTE leaves less revenue available to the government for financing public expenditure. CTE is an economic downturn that causes significant detrimental effects on the economy. Tax authorities are continually framing and modifying existing regulations to control tax evasion. While numerous studies have been conducted on CTE, the literature has primarily focused on the perspective of business owners. Till now, only limited attention has been given to the role of consumers towards CTE. The consumers who choose to make payments without receiving receipts create a scenario in which the sellers can easily evade taxes. Managing CTE by influencing consumer perception is the most cost-effective method to control evading practices in the economy. The moral perspective of consumers can play a decisive role in eradicating the unethical business practices. Thus, the present study uses Jones’s Issue Contingent Model to investigate consumers’ ethical decision-making process regarding CTE. Moreover, the Indian economy witnessed a significant change in the indirect tax system through the implementation of the goods and services tax. The new reform aims to improve the tax compliance level, but the Kerala economy witnessed an increase in the tax gap due to non-compliance after GST was introduced. Thus, studying CTE in the context of Kerala can provide new insights into the subject area.

The study demonstrates that a person’s moral perspective can instil moral intention by recognising CTE as a moral issue. Recognition of a moral issue can shape the formation of moral judgement, which further can inculcate moral intention in the mind of individuals. The study found that idealism, relativism and attitude towards government had a significant impact on moral recognition. Consumers’ ethical ideologies (i.e., idealism and relativism) play a significant role in influencing moral recognition regarding CTE. The results confirm that a higher level of ethical ideologies can improve the level of moral recognition. These findings are in line with the result of the study by Culiberg and Bajde (2014).

Existing literature has considered different psychographic factors for measuring tax compliance intention (Culiberg & Bajde, 2014; Srivastava et al., 2018; Trivedi et al., 2003), but only limited literature is available on the role of religiosity and attitude on compliance intention, especially in the context of the consumers. The religious perspective of the consumers can narrow down their intention to participate in CTE (Srivastava et al., 2018). But the present study found a contradictory result compared to the study conducted by Srivastava et al. (2018). The findings show no significant influence of religiosity on moral recognition regarding CTE. Meanwhile, an individual’s attitude towards the government was found to have a significant influence on the ethical decision-making process of the consumers towards CTE. This result abides by the findings of the study by Culiberg (2018) and Srivastava et al. (2018).

The research found a strong linkage between moral recognition and the moral judgement of consumers, and moral judgement has an effect on consumers’ intention to participate in CTE. Consumers’ moral recognition of CTE as unethical organises their judgement and results in better compliance decisions. A consumer with positive ideologies and a favourable attitude towards the system will voluntarily comply with all the rules and regulations, even if they are not receiving any monetary benefits for complying with the laws.

Implications

The research study establishes a conceptual model indicating the ethical decision-making process of consumers regarding CTE using Jones’s Issue Contingent Model. The study found ethical ideologies and attitudes towards government authority play a crucial role in instilling moral recognition in the minds of the consumers. Furthermore, the study explored the influence of moral recognition on moral judgement and its influence on moral intention. The insight gained from the study about consumers’ intentions can assist in measuring the consumers’ compliance behaviour regarding CTE. Meanwhile, religiosity was found to have no significant influence on the consumers’ moral recognition, while there also exist studies that found a positive association between religiosity and moral recognition. Thus, the findings of the study provide an opportunity for researchers to confirm the association between these factors.

The results of the study hold relevant implications for policymakers in addressing issues concerning tax performance. The evidence found suggests that consumers can indirectly influence the level of non-compliance among business dealers. So, understanding consumers’ ethical decision-making process could serve as a significant trigger for discouraging questionable tax-evading behaviour. Through social marketing campaigns, policymakers could raise awareness among consumers about the adverse consequences of paying without receipts. This approach allows consumers to recognise CTE as a moral issue, preventing them from engaging in any form of shady transactions and thereby minimising the harm caused to the economy. Moreover, the study’s results show that an attitude towards the government can encourage better decision-making. This provides an avenue for the government to foster a better relationship with its citizens by making them aware of the consequences of participating in CTE for the nation at large.

Limitations and Future Scope

The present study acknowledges certain drawbacks, as the responses were only collected from consumers and did not analyse the opinion of the other stakeholders. Therefore, the findings of the study reflect consumers’ perceptions regarding CTE. Future studies could be conducted among different stakeholders to obtain a more comprehensive understanding of tax compliance. Furthermore, a larger sample size across different locations could yield more robust results.

The study uses Jones’s Issue Contingent Model to investigate consumers’ ethical decision-making process regarding CTE, but there are other dimensions and behavioural models that could potentially explain compliance behaviour more efficiently. Therefore, the future researcher could consider incorporating additional dimensions or factors and explore other economic or non-economic models to gain better insights into compliance intentions regarding consumption taxes. In addition, the research only focuses on the moral intention of the consumers but did not incorporate their actual compliance behaviour, future studies can expand the model by considering the actual compliance behaviour of the consumers regarding CTE.

Conclusion

The ethical compliance decision of consumers can impact the behaviour of businesses. A consumer’s decision plays a determinantal role in controlling the non-compliance practices existing in the economy. A consumer’s moral recognition regarding CTE can positively influence their judgement and intention to comply. The consumers’ decision to buy only after receiving proper tax invoices or receipts can reduce the scope of businesses to evade taxes, thus improving the revenue collection of the government. The consumers’ decision can facilitate higher compliance levels among businesses, thereby reducing the need for administrative action to prevent tax evasion by the business community. The positive involvement of consumers can eradicate CTE and improve indirect revenue performance in a cost-effective manner.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Swathy Krishna https://orcid.org/0000-0002-9477-5303

Ababio, A. G., & Mangueye, A. G. (2021). State legitimacy and tax compliance among small and medium scale enterprises: A case study of Dodowa district, Ghana. Journal of Financial Crime, 28(3), 858–869. https://doi.org/10.1108/JFC-09-2020-0195

Abdullah, M., & Sapiei, N. S. (2018). Do religiosity, gender and educational background influence zakat compliance? The case of Malaysia. International Journal of Social Economics, 45(8), 1250–1264. https://doi.org/10.1108/IJSE-03-2017-0091

Agle, B. R., & Van Buren, H. J. (1999). God and mammon: The modern relationship. Business Ethics Quarterly, 9(4), 563–582. https://doi.org/10.2307/3857935

Alabede, J. O., Ariffin, Z. Z., & Idris, K. M. (2011). Individual taxpayers attitude and compliance behaviour in Nigeria: The moderating role of financial condition and risk preference. Journal of Accounting and Taxation, 3(3), 91–104. https://doi.org/10.5897/JAT11.010

Badaracco Jr, J. L., & Webb, A. P. (1995). Business ethics: A view from the trenches. California Management Review, 37(2), 8–28. https://doi.org/10.2307/2F41165786

Bateman, C. R., Valentine, S., & Rittenburg, T. (2013). Ethical decision making in a peer-to-peer file sharing situation: The role of moral absolutes and social consensus. Journal of Business Ethics, 115(2), 229–240. https://doi.org/10.1007/s10551-012-1388-1

Bentler, P. M. (1990). Comparative fit indexes in structural models. Psychological Bulletin, 107(2), 238. https://psycnet.apa.org/doi/10.1037/0033-2909.107.2.238

Bidin, Z., Mohd Shamsudin, F., & Othman, Z. (2014). Using theory of reasoned action to explain taxpayer intention to comply with goods and services tax. International Journal of Business and Social Science, 5(5 (1)), 131–139.

Bobek, D. D., & Hatfield, R. C. (2003). An investigation of the theory of planned behavior and the role of moral obligation in tax compliance. Behavioral Research in Accounting, 15(1), 13–38. https://doi.org/10.2308/bria.2003.15.1.13

Carsamer, E., & Abbam, A. (2020). Religion and tax compliance among SMEs in Ghana. Journal of Financial Crime. https://doi.org/10.1108/JFC-01-2020-0007

Cherry, J., & Fraedrich, J. (2002). Perceived risk, moral philosophy and marketing ethics: mediating influences on sales managers’ ethical decision-making. Journal of Business Research, 55(12), 951–962. https://doi.org/10.1016/S0148-2963(00)00215-0

Culiberg, B. (2018). How can governments tackle consumption tax evasion? Shedding light on the antecedents of consumer attitudes and intentions. Journal of Nonprofit & Public Sector Marketing, 30(4), 367–386. https://doi.org/10.1080/10495142.2018.1452824

Culiberg, B., & Bajde, D. (2014). Do you need a receipt? Exploring consumer participation in consumption tax evasion as an ethical dilemma. Journal of Business Ethics, 124(2), 271–282. https://doi.org/10.1007/s10551-013-1870-4

Culiberg, B., & Mihelic, K. K. (2016). Three ethical frames of reference: Insights into Millennials’ ethical judgements and intentions in the workplace. Business Ethics: A European Review, 25(1), 94–111. https://doi.org/10.1111/beer.12106

Cummings, R. G., Martinez-Vazquez, J., McKee, M., & Torgler, B. (2005). Effects of tax morale on tax compliance: Experimental and survey evidence (CREMA Working Paper).

De George, R. T. (1987). The status of business ethics: Past and future. Journal of Business Ethics, 6(3), 201–211. https://doi.org/10.1007/BF00382865

Drogalas, G., Anagnostopoulou, E., Pazarskis, M., & Petkopoulos, D. (2018). Tax ethics and tax evasion, evidence from Greece. Theoretical Economics Letters, 8(05), 1018–1028. https://doi.org/10.4236/tel.2018.85070

Eiya, O., Ilaboya, O. J., & Okoye, A. F. (2016). Religiosity and tax compliance: Empirical evidence from Nigeria. Igbinedion University Journal of Accounting, 1(1), 27–41.

Feige, E. L. (1994). The underground economy and the currency enigma. Public Finance= Finances Publiques, 49, 119–136.

Feld, L. P., & Frey, B. S. (2007). Tax compliance as the result of a psychological tax contract: The role of incentives and responsive regulation. Law & Policy, 29(1), 102–120. https://doi.org/10.1111/j.1467-9930.2007.00248.x

Ferrell, O., Gresham, L. G., & Fraedrich, J. (1989). A synthesis of ethical decision models for marketing. Journal of Macromarketing, 9(2), 55–64. https://doi.org/10.1177/2F027614678900900207

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/2F002224378101800104

Forsyth, D. R. (1980). A taxonomy of ethical ideologies. Journal of Personality and Social Psychology, 39(1), 175. https://doi.org/10.1177/2F014616728172006

Forsyth, D. R., O’boyle, E. H., & McDaniel, M. A. (2008). East meets west: A meta-analytic investigation of cultural variations in idealism and relativism. Journal of Business Ethics, 83(4), 813–833. https://doi.org/10.1007/s10551-008-9667-6

Frey, B. S., & Weck-Hanneman, H. (1984). The hidden economy as an unobserved variable. European Economic Review, 26(1–2), 33–53. https://doi.org/10.1016/0014-2921(84)90020-5

Fukukawa, K. (2002). Developing a framework for ethically questionable behavior in consumption. Journal of Business Ethics, 41, 99–119. https://doi.org/10.1023/A:1021354323586

Guerra, A., & Harrington, B. (2018). Attitude–behavior consistency in tax compliance: A cross-national comparison. Journal of Economic Behavior & Organization, 156, 184–205. https://doi.org/10.1016/j.jebo.2018.10.013

Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–152. https://doi.org/10.1504/IJMDA.2017.087624

Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review. https://doi.org/10.1108/EBR-11-2018-0203

Harman, G. (1978). What is moral relativism?. In Values and morals (pp. 13, 143–161). Springer. https://doi.org/10.1007/978-94-015-7634-5_9

Henderson, B. C., & Kaplan, S. E. (2005). An examination of the role of ethics in tax compliance decisions. Journal of the American Taxation Association, 27(1), 39–72. https://doi.org/10.2308/jata.2005.27.1.39

Henle, C. A., Giacalone, R. A., & Jurkiewicz, C. L. (2005). The role of ethical ideology in workplace deviance. Journal of Business Ethics, 56(3), 219–230. https://doi.org/10.1007/s10551-004-2779-8

Hessing, D. J., Elffers, H., & Weigel, R. H. (1988). Exploring the limits of self-reports and reasoned action: An investigation of the psychology of tax evasion behavior. Journal of Personality and Social Psychology, 54(3), 405.

Hofmann, E., Hoelzl, E., & Kirchler, E. (2008). Preconditions of voluntary tax compliance: Knowledge and evaluation of taxation, norms, fairness, and motivation to cooperate. Zeitschrift für Psychologie, 216(4), 209–217. https://doi.org/10.1027/0044-3409.216.4.209

Hofmann, E., Meier-Pesti, K., & Kirchler, E. (2007). The decision process for ethical investment. Journal of Financial Services Marketing, 12(1), 4–16. https://doi.org/10.1057/palgrave.fsm.4760057

Hollingworth, D., & Valentine, S. (2015). The moderating effect of perceived organizational ethical context on employees’ ethical issue recognition and ethical. Journal of Business Ethics, 128(2), 457–466. https://doi.org/10.1007/s10551-014-2088-9

https://doi.org/10.1016/0148-2963(95)00155-7

Hu, L. T., & Bentler, P. M. (1999). Cut off criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal, 6(1), 1–55. https://doi.org/10.1080/10705519909540118

Hunt, S. D., & Vitell, S. (1986). A general theory of marketing ethics. Journal of Macromarketing, 6(1), 5–16. https://doi.org/10.1177/2F027614678600600103

Jones, T. M. (1991). Ethical decision making by individuals in organizations: An issue-contingent model. Academy of Management Review, 16(2), 366–395. https://doi.org/10.5465/amr.1991.4278958

Kirchler, E., Hoelzl, E., & Wahl, I. (2008). Enforced versus voluntary tax compliance: The “slippery slope” framework. Journal of Economic Psychology, 29(2), 210–225. https://doi.org/10.1016/j.joep.2007.05.004

Maciejovsky, B., Schwarzenberger, H., & Kirchler, E. (2012). Rationality versus emotions: The case of tax ethics and compliance. Journal of Business Ethics, 109(3), 339–350. https://doi.org/10.1007/s10551-011-1132-2

McGee, R. W., Ho, S. S., & Li, A. Y. (2008). A comparative study on perceived ethics of tax evasion: Hong Kong vs the United States. Journal of Business Ethics, 77(2), 147–158. https://doi.org/10.1007/s10551-006-9304-1

Menon, P. (2019). The rise of the shadow economy: An Indian perspective. Journal of Public Affairs, 19(1), 1–7. https://doi.org/10.1002/pa.1880

Modugu, K. P., & Anyaduba, J. O. (2014). Impact of tax audit on tax compliance in Nigeria. International Journal of Business and Social Science, 5(9), 207–215.

Mohdali, R., & Pope, J. (2014). The influence of religiosity on taxpayers’ compliance attitudes: Empirical evidence from a mixed-methods study in Malaysia. Accounting Research Journal, 27(1),71–91. https://doi.org/10.1108/ARJ-08-2013-0061

Night, S., & Bananuka, J. (2019). The mediating role of adoption of an electronic tax system in the relationship between attitude towards electronic tax system and tax compliance. Journal of Economics, Finance and Administrative Science, 25(49), 73–88, https;//doi.org/10.1108/JEFAS-07-2018-0066

O’Fallon, M. J., & Butterfield, K. D. (2013). A review of the empirical ethical decision-making literature: 1996–2003. Citation Classics from the Journal of Business Ethics, 213–263. https://doi.org/10.1007/978-94-007-4126-3_11

Palil, M. R., & Mustapha, A. F. (2011). Factors affecting tax compliance behaviour in self assessment system. African Journal of Business Management, 5(33), 12864–12872. https://doi.org/10.5897/AJBM11.1742

Pan, Y., & Sparks, J. R. (2012). Predictors, consequence, and measurement of ethical judgments: Review and meta-analysis. Journal of Business Research, 65(1), 84–91. https://doi.org/10.1016/j.jbusres.2011.02.002

Rest, J. R. (1986). Moral development: Advances in research and theory (p. 224). Praeger. http://hdl.handle.net/10822/811393

Robin, D. P., Reidenbach, R. E., & Forrest, P. J. (1996). The perceived importance of an ethical issue as an influence on the ethical decision-making of ad managers. Journal of Business Research, 35(1), 17–28. https://doi.org/10.1016/0148-2963(94)00080-8

Sadress, N., Bananuka, J., Orobia, L., & Opiso, J. (2019). Antecedents of tax compliance of small business enterprises: a developing country perspective. International Journal of Law and Management, 61(1), 24–44. https://doi.org/10.1108/IJLMA-10-2017-0234

Sarkar, S. (2010). The parallel economy in India: Causes, impacts and government initiatives. Economic Journal of Development Issues, 11, 124–134. https://doi.org/10.3126/ejdi.v11i0.6111

Saxunova, D., & Szarkova, R. (2018). Global efforts of tax authorities and tax evasion challenge. Journal of Eastern Europe Research in Business and Economics, 1–14. https://doi.org/10.5171/2018.511388

Schneider, F., Chaudhuri, K., & Chatterjee, S. (2003). The size and development of the Indian shadow economy and a comparison with other 18 Asian countries: An empirical investigation (Working Paper, 302).

Seralurin, Y. C., & Ermawati, Y. (2019). Influence of self-assessment system, taxation understanding, and discrimination toward ethics of tax evasion: A case in Papua Indonesia. International Research Journal of Management, IT and Social Sciences, 6(5), 267–278. https://doi.org/10.21744/irjmis.v6n5.745

Sidani, Y. M., Ghanem, A. J., & Rawwas, M. Y. (2014). When idealists evade taxes: the influence of personal moral philosophy on attitudes to tax evasion—A Lebanese study. Business Ethics: A European Review, 23(2), 183–196. https://doi.org/10.1111/beer.12046

Singhapakdi, A., Vitell, S. J., & Kraft, K. L. (1996). Moral intensity and ethical decision-making of marketing professionals. Journal of Business Research, 36(3), 245–255.

Skitka, L. J., Washburn, A. N., & Carsel, T. S. (2015). The psychological foundations and consequences of moral conviction. Current Opinion in Psychology, 6(1), 41–44. https://doi.org/10.1016/j.copsyc.2015.03.025

Spilka, B., Hood, R. W., Hunsberger, B., & Gorsuch, R. (2003). The psychology of religion: An empirical approach. Guilford Press.

Srivastava, H. S., Singh, G., & Mishra, A. (2018). Factors affecting consumers’ participation in consumption tax evasion. Journal of Indian Business Research, 10(3), 274–290. https://doi.org/10.1108/JIBR-10-2017-0191

Stark, A. (1993). What’s the matter with business ethics? Harvard Business Review, 71(3), 38–40.

Taing, H. B., & Chang, Y. (2021). Determinants of tax compliance intention: focus on the theory of planned behavior. International Journal of Public Administration, 44(1), 62–73. https://doi.org/10.1080/01900692.2020.1728313

Torgler, B. (2007). Tax compliance and tax morale: A theoretical and empirical analysis. Edward Elgar Publishing.

Torgler, B., & Murphy, K. (2004). Tax morale in Australia: what shapes it and has it changed over time? Journal of Australian Taxation, 7(2), 298–335.

Trivedi, V. U., Shehata, M., & Lynn, B. (2003). Impact of personal and situational factors on taxpayer compliance: An experimental analysis. Journal of Business Ethics, 47(3), 175–197. https://doi.org/10.1023/A:1026294332606

Valentine, S. R., & Rittenburg, T. L. (2004). Spanish and American business professionals’ ethical evaluations in global situations. Journal of Business Ethics, 51(1), 1–14. https://doi.org/10.1023/B:BUSI.0000032384.74020.a8

Wahl, I., Kastlunger, B., & Kirchler, E. (2010). Trust in authorities and power to enforce tax compliance: An empirical analysis of the ‘Slippery Slope Framework’. Law & Policy, 32(4), 383–406. https://doi.org/10.1111/j.1467-9930.2010.00327.x

Weaver, G. R., & Agle, B. R. (2002). Religiosity and ethical behavior in organizations: A symbolic interactionist perspective. Academy of Management Review, 27(1), 77–97. https://doi.org/10.5465/amr.2002.5922390

Webley, P., Cole, M., & Eidjar, O. P. (2001). The prediction of self-reported and hypothetical tax-evasion: Evidence from England, France and Norway. Journal of Economic Psychology, 22(2), 141–155. https://doi.org/10.1016/S0167-4870(01)00026-5

Wiggins, D. (1990). Moral cognitivism, moral relativism and motivating moral beliefs. Proceedings of the Aristotelian Society, 91, 61–85.

Worthington Jr, E. L., Wade, N. G., Hight, T. L., Ripley, J. S., McCullough, M. E., Berry, J. W., Bursley, K. H., & O’Connor, L. (2003). The Religious Commitment Inventory–10: Development, refinement, and validation of a brief scale for research and counseling. Journal of Counseling Psychology, 50(1), 84–96. https://doi/10.1037/0022-0167.50.1.84

Yang, H. L., & Wu, W. P. (2009). The effect of moral intensity on ethical decision making in accounting. Journal of Moral Education, 38(3), 335–351. https://doi.org/10.1080/03057240903101606