Review of Professional Management

Search

Search

Purushottam Kumar Arya1 , Mamta Adhana1 and Anshika Agarwal2

, Mamta Adhana1 and Anshika Agarwal2

1Department of Commerce, Delhi School of Economics, University of Delhi, India

2 Faculty of Management Studies, University of Delhi, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Small and medium enterprises (SMEs) are crucial for economic development, contributing significantly to employment, innovation, and overall economic stability. However, SMEs face challenges such as asymmetric information and ex-ante uncertainty due to their relatively short operational histories, and also, SME exchanges have relatively fewer regulations and listing requirements as compared to mainboard exchanges. By leveraging various signals, such as the reputation of underwriters, these issues can be mitigated during the IPO process. This study aims to explore the signalling role of prominent underwriters and their effects on initial returns and post-issue stock performance of IPOs in India. This study includes the data of 298 IPOs of SME firms listed on the BSE SME platform and NSE EMERGE between April 2012 and March 2020, which were collected from CMIE Prowess. The signalling function of underwriters was tested using multiple regression analysis. The result shows that Underwriter reputation (UWR) positively affects underpricing, but in the long term, it does not have any impact on post-issue stock performance of an IPO Firm.

Underwriter reputation, IPO returns, underpricing, BHAR, Information asymmetry

Introduction

Small and medium enterprises (SMEs) are often considered the backbone of both developed and developing economies. SMEs contribute significantly to job creation, economic diversification, and innovation. In developing countries, they are particularly important in addressing unemployment and fostering inclusive growth of the nation. As stated by the World Bank, ‘small and medium enterprises (SMEs) make up roughly 90% of all businesses globally and contribute over 50% to worldwide employment’. According to the Reserve Bank of India (RBI), ‘SMEs are crucial to India’s socio-economic progress, as they significantly contribute to the country’s GDP, industrial development, job creation, and export activities’. Despite its importance, the sector faces significant challenges, such as insufficient and delayed access to credit, as well as limited availability of equity capital (SIDBI, 2013). A key challenge for the growth and development of SMEs today is securing access to external financing (Sestanovic, 2015). To offer a market-driven solution for equity resource mobilisation for SMEs, SEBI authorised the creation of dedicated platforms in 2012: the BSE SME and the NSE EMERGE to support these enterprises. However, SME exchanges are different from Main Boards in terms of their regulations and listing requirements, such as mandatory underwriting by investment banks, minimum participation of investors, market-making responsibilities by merchant banks, company characteristics required for listing, financial reporting and ongoing disclosure requirements.

The information gap arises from ex-ante uncertainty and asymmetric information between issuers and investors, primarily due to the issuer’s limited operational history and fewer disclosure obligations, which puts shareholders’ investments at risk. To minimise information asymmetry in SME IPOs, issuers employ various signalling mechanisms like selecting reputable underwriters, securing venture capital backing, engaging high-quality auditors, encouraging institutional investor participation, maintaining transparency, careful pricing strategies, issuing a prospectus, and strengthening board and management quality. These signals help build trust, attract investors, and enhance the perceived quality of the IPO, and by addressing the information gaps between issuers and investors, these measures help mitigate the ‘winner’s curse’ and reduce the likelihood of underpricing.

A high-quality underwriter can act as a certification of the firm’s credibility and stability. Reputable underwriters are selective in choosing which IPOs they support because their reputation is at stake. IPO issues backed by prestigious underwriters experience less underpricing, as underwriter reputation (UWR) signals firm quality to potential investors (Carter & Manaster, 1990). Many researchers attribute underpricing to information asymmetry, a theory proposed by several scholars, including Welch (1989), Beatty and Ritter (1986), Rock (1986), Allen and Faulhaber (1989), Ritter and Welch (2002), and Loughran and Ritter (2004).

A reputable underwriter signals the value of an issuing firm by conducting rigorous due diligence, which reassures investors about the firm’s quality and reduces the likelihood of post-IPO issues such as accounting irregularities or operational issues. The underwriter’s reputation acts as a certification of the IPO’s quality (Carter & Manaster, 1990). Loughran and Ritter (2004), in their study, highlight that reputable underwriters help reduce information asymmetry, which can positively affect long-term returns

The main goal of this study is twofold. First, it will explore the connection between UWR and the degree of underpricing in Indian SME IPOs. Second, it will analyse the link between UWR and the post-issue stock performance of Indian SME IPOs.

The article is organised into multiple sections to fulfil its objective. The second section provides reviews of previous research, while the third outlines the research methodology, including data analysis and interpretations. The fourth section presents the conclusions and implications.

Literature Overview

An IPO represents a crucial step for companies aiming to raise capital and expand their operations. According to Pagano et al. (1998), firms typically choose to go public to adjust their capital structure, secure funds for future investments, and improve their market visibility. Kim and Ritter (1999) highlight that IPOs come with substantial costs, such as underwriting fees, legal expenses, and the preparation of regulatory documents, which can present significant challenges for smaller companies, especially SMEs. Additionally, the timing of an IPO plays a pivotal role in its success. As Ljungqvist et al. (2006) found, companies often opt for IPOs when market conditions are favourable—such as during periods of investor optimism or bull markets.

IPO success is influenced by a combination of internal factors, such as the company’s size, financial performance, governance, and external factors, such as market conditions, UWR, and institutional investor participation. UWR has long been recognised as a key factor influencing both the short-term and long-term outcomes of IPOs

Carter and Manaster (1990) introduced the concept of UWR as a significant determinant of IPO pricing. According to him, reputable underwriters provide a certification role, signalling to investors that the firm is of high quality, leading to reduced underpricing. Subsequent studies in developed markets, particularly in the US, consistently support this view, demonstrating that renowned underwriters decrease IPO underpricing by reducing information asymmetry between the issuing firm and investors (Beatty & Ritter, 1986; Carter & Manaster, 1990). Ljungqvist (2007) also reinforced this, noting that a strong UWR attracts institutional investors, reducing the need for significant price discounts.

However, studies in emerging markets such as India and China offer varying results. For instance, Katti and Phani (2016) found that while reputable underwriters play a role in reducing underpricing in India, the effect is not as pronounced as in developed markets due to differences in regulatory environments and investor behaviour. Similarly, Chen et al. (2004) observed that in the Chinese market, UWR had a limited impact on reducing underpricing due to less stringent disclosure requirements. Additionally, Michaely and Shaw (1994) noted that in high-risk or emerging industries, UWR does not significantly reduce underpricing, as market conditions and company-specific risks play a more prominent role.

According to Dhamija and Arora’s (2017) study, the reputation of underwriters has been shown to have a negative impact on the degree of IPO underpricing. Similar findings have been observed in other research, including works by Johnson and Miller (1988), Sundarasen et al. (2018) and Reutzel and Belsito (2015), all of which identified a negative correlation between UWR and underpricing.

While UWR is often linked to short-term IPO success, its effect on long-term performance, measured by BHAR, is less conclusive, especially in emerging markets where institutional frameworks and investor protections differ from those in developed economies.

Research by Krigman et al. (1999) in the US indicated that IPOs backed by reputable underwriters typically outperform the market over the long term. Similarly, Boehmer and Fishe (2004) emphasise that IPOs backed by reputable underwriters tend to have better liquidity and market support, contributing to stronger long-term performance.

In contrast, studies in emerging markets report differing outcomes. In India, Sahoo and Rajib (2010) observed that although reputable underwriters reduce initial underpricing, they do not significantly affect three-year BHAR, indicating that market conditions and firm fundamentals are more influential in determining long-term success. A study by Bhabra and Pettway (2003) also reported similar findings in Japan.

The impact of UWR on IPO outcomes is well-documented in developed markets like the US and Europe, where mature IPO ecosystems, stringent regulations, and high institutional participation enhance the underwriter’s certification role, reducing underpricing and improving post-issue performance (Carter & Manaster, 1990; Megginson & Weiss, 1991). However, in the Indian SME IPO context, these effects are less pronounced due to a retail-driven investor base and lower institutional involvement, which diminishes the perceived credibility of underwriters. Additionally, lenient regulatory norms and limited disclosure requirements, as outlined by SEBI (2012), further weaken the impact of UWR on IPO performance.

Liquidity constraints also play a significant role in shaping SME IPO performance in India. Unlike developed markets, where unrestricted secondary market trading allows organic price adjustments, Indian SME IPOs operate under mandatory market-making requirements for three years post-listing. While this stabilises prices, it also limits free price discovery and can distort long-term post-IPO stock performance (Pandey & Vaidyanathan, 2013). These differences create a unique IPO environment where UWR may not have the same long-term influence as observed in developed markets.

Information asymmetry significantly distinguishes Indian SME IPOs from those in developed markets. Due to lenient disclosure norms, Indian SME firms face higher information asymmetry, reporting only semi-annually with minimal corporate governance requirements, unlike developed markets where stricter quarterly reporting enhances underwriter credibility (Michaely & Shaw, 1994; SEBI, 2012). Additionally, while developed markets show that reputed underwriters reduce underpricing through rigorous due diligence (Booth & Chua, 1996), Indian studies (Katti & Phani, 2016; Sahoo & Rajib, 2010) reveal the opposite—reputed underwriters in India often experience higher underpricing, indicating that they might be leveraging market sentiment rather than mitigating information asymmetry.

While developed market studies provide a foundational understanding of IPO behaviour, their applicability to Indian SMEs is limited by structural differences, investor profiles, and market regulations. Unlike the NYSE or NASDAQ, Indian SME exchanges have lower liquidity and fewer regulatory obligations, which affects post-IPO stock behaviour. Additionally, market timing and regulatory influence play a crucial role in Indian SME IPO performance, as these firms are more susceptible to macroeconomic volatility and SEBI’s changing regulatory policies compared to developed markets. By addressing these distinctions, this study aims to bridge the research gap and provide a more nuanced understanding of how UWR functions in the Indian SME IPO ecosystem, acknowledging the limitations of direct comparisons with developed markets.

Research Gap

The majority of research examining the effect of UWR on underpricing and BHAR (a measure of post-issue stock performance) has primarily focused on developed countries. As a developing nation, India offers a unique context for investigating whether the well-established link of UWR with initial return and BHAR of an SME IPO Firm holds true or not. Additionally, there is relatively limited research to the best of our knowledge that explores how UWR influences both the initial returns and post-issue returns of SMEs in India. Consequently, this study aims to fill this gap by investigating the signalling role of underwriters with a particular emphasis on India.

Hypothesis

H1: The reputation of underwriters and the level of underpricing in IPOs of SME firms in India are positively correlated.

H2: There is a positive relationship between UWR and BHAR of IPOs of SME firms in India.

Research Methodology

Data Collection Methods

This study focuses on Initial Public Offerings listed on the Bombay Stock Exchange SME platform and National Stock Exchange Emerge platform between April 2012 and March 2020, and data for the year March 2012 to June 2023 for the variables analysis were sourced from CMIE Prowess, prospectuses of IPO firms and the authorised website of Bombay Stock Exchange and National Stock Exchange. The data includes a total of 298 IPOs that went public during this period. Data from financial companies is excluded from the sample, and also firms with extreme outliers and with missing data for certain variables have also been excluded.

Variable Measurement

Underpricing (Dependent Variable)

For measuring underpricing, market-adjusted excess return (MAER), that is, MAER, has been used in this study. It is used to evaluate the performance of IPO relative to the overall market and helps to determine whether the IPO outperformed or underperformed the broader market after adjusting for market movements.

Where,

RIPO is the return of IPO stock calculated based on the percentage change between the offer price and the closing price on the listing day.

RM is the return of the market index (S&P BSE SME INDEX) over the same period as the IPO.

Long-term Performance (Dependent Variable)

For measuring long-term performance, a 36-month period BHAR is viewed as the most appropriate method for the study. A 36-month period BHAR period begins in the fourth month after the completion of the initial fiscal year, subsequent to the Initial Public Offer of the firm. The S&P BSE SME INDEX has been used for calculating market return.

Formula for 36-month BHAR:

Where,

Ri,t is the return of the IPO stock in month t,

Rm,t is the return of the benchmark index in month t,

And t = 36-month period.

UWR (Independent Variable)

UWR is evaluated using its relative market share, based on the method proposed by Megginson and Weiss (1991).

UWR is calculated as: (IPO proceeds handled by the underwriter divided by total IPO size of all firms in the data) × 100.

Control Variables

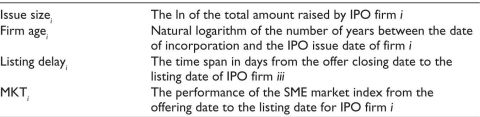

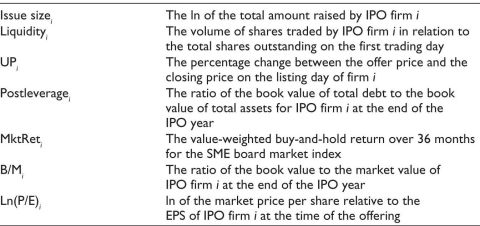

Several control variables have been used in this study, which are as follows:

This study utilises a multiple regression model to examine the hypothesis and assess the effect of UWR on a firm’s first day returns, that is, underpricing and post-issue stock performance, BHAR.

Multiple regression model for underpricing:

Multiple regression model for BHAR:

Data Analysis and Interpretation

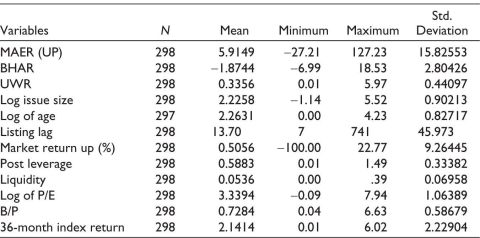

Table 3 provides the descriptive statistics of all the factors included in the study. The average MAER is 5.91%, indicating that, on average, IPOs tend to be positively underpriced. However, the range is quite broad, from –27.21% to 127.23%, showing that while some companies experienced negative underpricing, others saw exceptionally high performance on the launch day of trading. The standard deviation of 15.83 reflects considerable variability, suggesting a wide dispersion in performance among different companies.

Table 1. Control Variables for Underpricing.

Table 2. Control Variables for Post-issue Stock Performance.

Table 3. Descriptive Statistics.

For BHAR, the average value is –1.87, indicating that, on average, companies underperformed relative to their expected returns. The BHAR ranges from –6.99 to 18.53, with some companies significantly underperforming, while others achieved much higher returns than anticipated.

The mean UWR score is 0.34, indicating a generally low average reputation for underwriters. This score ranges from 0.01 to 5.97, highlighting a substantial disparity in UWR across different companies, with some IPOs backed by very reputable underwriters while others are associated with underwriters of lower standing.

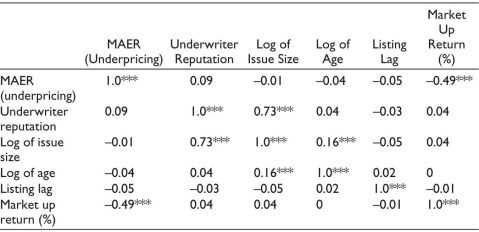

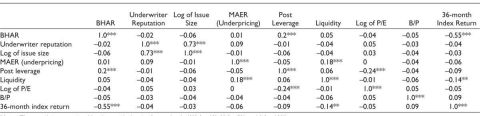

The correlation matrix presented in Table 4 provides insights into the factors influencing underpricing, measured by MAER. The analysis reveals that market conditions, as reflected by the Market UP Return, play the most significant role in explaining underpricing. When markets perform poorly, underpricing tends to increase, implying that companies may offer more substantial discounts to ensure the success of their IPOs. Control variables such as company age, issue size, and listing lag exhibit little to no relationship with underpricing, indicating that these factors may not strongly influence the level of underpricing. Overall, the analysis highlights that market return is the primary factor driving underpricing in this context, while other variables, including UWR, play a less prominent role.

Table 4. Correlation Matrix for Underpricing.

Note: The correlation matrix table, along with the significance levels (*** for 1%, ** for 5%, and * for 10%).

Table 5 displays the correlation table for BHAR. The analysis shows that post-IPO leverage has a significant positive impact on BHAR, indicating that firms with higher leverage after going public tend to achieve better abnormal returns. Conversely, the 36-Month Index Return exhibits a strong negative and significant relationship with BHAR, suggesting that companies tend to achieve higher abnormal returns during periods of weaker market performance. Other variables, such as UWR, issue size, and various control factors, do not show any significant effect on BHAR.

Table 5. Correlation Matrix for Post-issue Stock Performance.

Note: The correlation matrix table, along with the significance levels (*** for 1%, ** for 5%, and * for 10%).

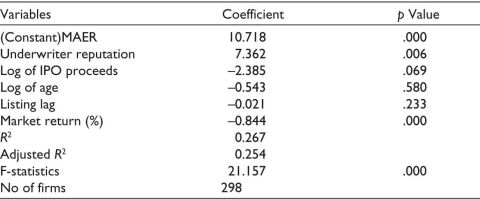

The regression analysis presented in Table 6 examines the relationship between underpricing, as measured by MAER, and various factors, with UWR as the primary independent variable. The control variables included in this model are summarised in Table 1. The findings show that UWR has a significant and positive effect on MAER, with a coefficient of 7.3625 and p value .0056, showing significance at both the 1% and 5% levels. This suggests that companies working with more reputable underwriters tend to experience more underpricing on the first day of listing. These results align with the findings of Beatty and Welch (1986), Arora and Singh (2019), Gao et al. (2015) and Liu and Ritter (2011). We, therefore, fail to reject the first hypothesis that a significant positive relationship exists between UWR and initial market return, that is, underpricing.

Table 6. Multiple Regression for Underpricing.

In contrast, the log of IPO proceeds shows a negative effect on underpricing, with a coefficient of -2.3852. Although this variable is only marginally significant at the 10% level, the negative relationship suggests that larger IPO sizes tend to be associated with lower underpricing. This result aligns with Booth and Chua (1996), who discovered an inverse relationship between IPO size and underpricing, noting that larger firms, with their greater visibility and reputation, face less uncertainty and thus experience lower underpricing. The studies by Beatty and Ritter (1986), Ritter (1984), and Megginson and Weiss (1991) also present similar findings, highlighting a negative correlation between IPO size and underpricing.

Other control variables, such as the log of the company’s age and listing lag, do not show statistically significant effects on underpricing. Although the listing lag has a negative coefficient, suggesting that a longer lag may reduce returns, this effect is not statistically significant.

In summary, the analysis highlights that UWR is a key factor in determining IPO underpricing, while other factors like IPO size and company age have a weaker or less consistent impact on MAER.

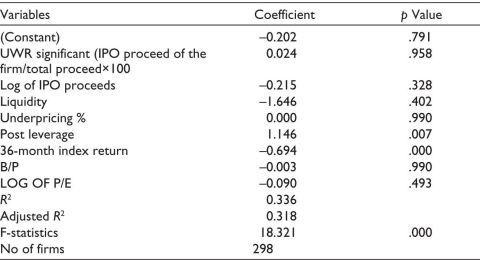

The regression analysis in Table 7 provides a comprehensive understanding of the factors affecting long-term stock performance, measured through Buy-and-Hold Abnormal Returns (BHAR), following an IPO. The control variables used in this model are presented in Table 2. One of the most significant findings is the strong positive relationship between the 36-month index return and BHAR, with a highly significant p value close to zero. This suggests that the overall market performance in the three years post-IPO plays a crucial role in influencing a company’s abnormal returns. In periods of positive market growth, companies tend to see better stock performance, while downturns can have a negative impact, highlighting the importance of broader market conditions on long-term returns.

Table 7. Multiple Regression for Post-issue Stock Performance.

In addition to market trends, company-specific financial decisions, particularly post-IPO leverage, have been found to exert a positive and significant influence on BHAR. The positive coefficient for post-IPO leverage suggests that companies with higher debt levels after going public often experience better stock performance. Investors may view increased leverage as a sign of the firm’s growth potential and expansion plans, which can drive higher returns. This indicates that, aside from market conditions, strategic financial choices made by the company play a key role in determining its post-IPO success. This finding aligns with Campello (2006), who observed that post-IPO leverage, particularly in capital-intensive industries, enhances long-term performance by enabling investment in profitable projects. Similarly, Zhang (2008) found that firms with moderate leverage post-IPO tend to perform better over time, as debt financing supports growth initiatives like expansion and acquisitions while maintaining a balanced financial structure.

On the other hand, UWR, which is typically considered important in the IPO process, does not show any meaningful influence on long-term stock performance. The p values are well above common significance levels, indicating they do not significantly impact BHAR in this model. These findings are in line with Sahoo and Rajib (2010) and Bhabra and Pettway (2003). We, therefore, reject the second hypothesis that says there exists a positive relationship between BHAR and UWR.

Other variables, including the log of IPO proceeds, underpricing, the book-to-price ratio, and the log of price-to-earnings ratio, also do not exhibit significant relationships with BHAR. Therefore, the analysis emphasises that while general market conditions and post-IPO financial decisions are pivotal in driving long-term abnormal returns, factors like UWR and initial underpricing have minimal impact.

The results of this study provide valuable insights into the role of UWR in the Indian SME IPO market. One of the most significant findings is that while UWR has a positive and significant impact on underpricing, it does not have a meaningful influence on long-term stock performance as measured by BHAR over a 36-month period. This finding challenges conventional theories in IPO literature that emphasise the role of underwriters in certifying firm quality and reducing information asymmetry in both the short and long run (Carter & Manaster, 1990; Megginson & Weiss, 1991).

A possible explanation for this disconnect between short-term and long-term IPO outcomes lies in the signalling theory and its limitations in the SME context. According to signalling theory (Spence, 1973), reputable underwriters act as credible certifiers of firm quality by engaging in rigorous due diligence, thereby reducing ex-ante uncertainty about the IPO firm. This explains why SME firms backed by reputed underwriters experience higher initial underpricing. However, the results indicate that this signal does not extend into the long term, implying that UWR is a weak predictor of a firm’s post-IPO performance.

Furthermore, the market-making requirements imposed on Indian SME IPOs further complicate the interpretation of long-term stock performance. Unlike developed markets, where stock prices adjust organically, Indian SME IPOs require mandatory market-making for three years post-listing, which creates artificial price support that may distort the true impact of UWR on stock performance in the long run.

Another theoretical perspective that supports this finding is the institutional voids theory (Khanna & Palepu, 2010), which suggests that emerging markets, like India, lack the mature financial infrastructure found in developed economies. Due to weaker investor protection laws, limited analyst coverage, and lower corporate transparency, the ability of underwriters to influence long-term stock performance is diminished. Instead, firm fundamentals, post-IPO financial strategies, and broader macroeconomic conditions play a larger role in shaping long-term returns. This theory provides a strong basis for understanding why the traditional certification role of underwriters, which works well in developed markets, does not hold the same weight in India’s SME segment.

In conclusion, this study contributes to IPO literature by demonstrating that UWR in Indian SME IPOs is a short-term signal rather than a long-term performance predictor. This challenges traditional signalling and certification theories and highlights the unique structural challenges of the Indian SME market.

Conclusion

This study contributes to the literature on IPO underpricing and post-issue stock performance by analysing the role of UWR in the Indian SME IPO market. The results reveal that while UWR significantly influences initial underpricing, it does not have a lasting impact on long-term stock performance as measured by BHAR. This challenges traditional signalling and certification theories, which suggest that underwriters play a crucial role in reducing ex-ante uncertainty and improving firm credibility beyond the IPO stage (Carter & Manaster, 1990; Megginson & Weiss, 1991).

By focusing on SME IPOs in an emerging market like India, this study expands the understanding of how market-specific dynamics, regulatory structures, and investor composition influence IPO outcomes. Unlike developed markets where institutional investors dominate IPO subscriptions and post-listing governance, the Indian SME segment is heavily retail-driven, with lower institutional oversight. This weakens the long-term signalling effect of UWR, suggesting that firm fundamentals and market conditions play a more decisive role in post-IPO performance. These findings align with studies in other emerging markets (Katti & Phani, 2016; Sahoo & Rajib, 2010) that indicate UWR is a stronger predictor of short-term rather than long-term success in less developed financial ecosystems.

This study also highlights the influence of market-making regulations on SME IPO outcomes. Unlike developed markets, where IPO pricing and performance adjust through unrestricted market forces, Indian SME exchanges impose a three-year mandatory market-making requirement. This could distort price discovery and dampen the impact of UWR on long-term stock performance. By identifying this regulatory factor, the study offers new insights into how institutional voids (Khanna & Palepu, 2010) and policy-driven mechanisms shape SME IPO trajectories in emerging economies.

Theoretical Contributions of the Study

This study challenges the universality of signalling theory by demonstrating that UWR’s impact on long-term performance is context-dependent. In emerging markets like India, factors such as market conditions, firm fundamentals, and post-IPO financial decisions have a greater influence than UWR, unlike in developed markets. Additionally, the study bridges SME IPO research with institutional voids theory, highlighting that weaker investor protection, limited financial transparency, and lower institutional involvement reduce the traditional role of underwriters as certifying agents. Furthermore, it introduces market-making as a structural factor affecting IPO performance, noting that mandatory market-making in SME exchanges can disrupt long-term stock performance, diminishing the predictive power of UWR compared to free-market environments.

Implications

The results of this study hold valuable implications for a range of stakeholders, including investors, SME IPO issuing firms, researchers, and regulators.

For investors, the study emphasises the need to consider UWR, company-specific factors and market conditions before investing in an IPO. As an underwriter, Reputation only impacts IPOs’ initial return and has little impact on long-term performance, so understanding the role of market trends and company-specific decisions can guide more informed investment choices in the SME sector.

For issuers, companies should be aware that while UWR is important, it may not be a decisive factor in IPO success. Instead, focusing on market conditions and strategic financial decisions before and after IPO could be more beneficial.

The policymakers can use the results of this study to formulate various rules and regulations for regulating SME IPOs.

For researchers, the study recommends that future research could investigate deeply into the aspects of market conditions and pre-IPO and post-IPO financial strategies to better understand their effects on IPO outcomes.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Purushottam Kumar Arya https://orcid.org/0000-0003-3744-5508

Allen, F., & Faulhaber, G. R. (1989). Signalling by underpricing in the IPO market. Journal of Financial Economics, 23(2), 303–323. https://doi.org/10.1016/0304-405X(89)90060-3

Arora, N., & Singh, B. (2019). Determinants of IPO underpricing: Evidence from India. Global Business Review, 20(1), 187–213. https://doi.org/10.1177/0972150918811232

Beatty, R. P., & Ritter, J. R. (1986). Investment banking, reputation, and the underpricing of initial public offerings. Journal of Financial Economics, 15(1–2), 213–232. https://doi.org/10.1016/0304-405X(86)90055-3

Bhabra, H. S., & Pettway, R. H. (2003). IPO prospectus information and subsequent performance. Financial Review, 38(3), 369–397. https://doi.org/10.1111/1540-6288.00052

Boehmer, E., & Fishe, R. P. H. (2004). Do underwriters encourage stock liquidity? Evidence from IPOs. Journal of Banking & Finance, 28(4), 835–859. https://doi.org/10.1016/j.jbankfin.2003.11.003

Booth, J. R., & Chua, L. (1996). Ownership dispersion, costly information, and IPO underpricing. Journal of Financial Economics, 41(2), 291–310. https://doi.org/10.1016/0304-405X(95)00863-F

Campello, M. (2006). Debt financing: Does it boost or hurt firm performance? Evidence from a cross-industry comparison. Journal of Financial Economics, 82(1), 135–172. https://doi.org/10.1016/j.jfineco.2005.04.001

Carter, R. B., & Manaster, S. (1990). Initial public offerings and underwriter reputation. Journal of Finance, 45(4), 1045–1067. https://doi.org/10.1111/j.1540-6261.1990.tb02426.x

Chen, G., Firth, M., & Kim, J. B. (2004). IPO underpricing in China’s new stock markets. Journal of Multinational Financial Management, 14(3), 283–302. https://doi.org/10.1016/j.mulfin.2004.03.002

Dhamija, S., & Arora, R. K. (2017). Impact of quality certification on IPO underpricing: Evidence from India. Global Business Review, 19(1), 69–84. https://doi.org/10.1177/0972150917749282

Johnson, J. M., & Miller, R. E. (1988). Investment banker prestige and the underpricing of initial public offerings. Journal of Finance. https://doi.org/10.1111/j.1540-6261.1988.tb04593.x

Katti, S., & Phani, B. V. (2016). Underpricing of initial public offerings: A literature review. Universal Journal of Accounting and Finance, 4(2), 35–52. https://doi.org/10.13189/ujaf.2016.040202

Khanna, T., & Palepu, K. (2010). Winning in emerging markets: A road map for strategy and execution. Harvard Business Press.

Kim, M., & Ritter, J. R. (1999). Valuing IPOs. Journal of Financial Economics, 53(3), 409–437. https://doi.org/10.1016/S0304-405X(99)00027-6

Krigman, L., Shaw, W., & Womack, K. (1999). The persistence of IPO mispricing and the predictive power of flipping. Journal of Finance, 54(3), 1015–1044. https://doi.org/10.1111/0022-1082.00136

Ljungqvist, A. (2007). IPO underpricing. In Handbook of corporate finance: Empirical corporate finance (Vol. 1, pp. 375–422). Elsevier. https://doi.org/10.1016/B978-0-444-53265-7.50018-3

Ljungqvist, A., Nanda, V., & Singh, R. (2006). Hot markets, investor sentiment, and IPO pricing. Journal of Business, 79(4), 1667–1702. https://doi.org/10.1086/503644

Loughran, T., & Ritter, J. (2004). Why has IPO underpricing changed over time? Financial Management, 33(3), 5–37. https://doi.org/10.2139/ssrn.331780

Megginson, W. L., & Weiss, K. A. (1991). Venture capitalist certification in initial public offerings. Journal of Finance, 46(3), 879–903. https://doi.org/10.1111/j.1540-6261.1991.tb03770.x

Michaely, R., & Shaw, W. H. (1994). The pricing of initial public offerings: Tests of adverse-selection and signaling theories. Review of Financial Studies, 7(2), 279–319. https://doi.org/10.1093/rfs/7.2.279

Pagano, M., Panetta, F., & Zingales, L. (1998). Why do companies go public? An empirical analysis. Journal of Finance, 53(1), 27–64. https://doi.org/10.1111/0022-1082.25448

Pandey, N., & Vaidyanathan, R. (2013). Determinants of IPO underpricing in the national stock exchange of India. IIM Bangalore Research Paper, 396, 1–38. https://doi.org/10.2139/ssrn.2293411

Reutzel, C. R., & Belsito, C. A. (2015). Female directors and IPO underpricing in the US. International Journal of Gender and Entrepreneurship, 7(1), 27–44. https://doi.org/10.1108/IJGE-01-2013-0003

Ritter, J. R. (1984). The hot issue market of 1980. Journal of Business, 57(2), 215–240. https://doi.org/10.1086/296260

Ritter, J. R., & Welch, I. (2002). A review of IPO activity, pricing, and allocations. Journal of Finance, 57(4), 1795–1828. https://doi.org/10.1111/1540-6261.00478

Rock, K. (1986). Why new issues are underpriced. Journal of Financial Economics, 15(1–2), 187–212. https://doi.org/10.1016/0304-405X(86)90054-1

Sahoo, S., & Rajib, P. (2010). Aftermarket pricing performance of IPOs: Indian IPO market 2002–2006. Vikalpa, 35(4), 27–43. https://doi.org/10.1177/0256090920100404

SEBI. (2012). Guidelines for SME listing on BSE and NSE Emerge. Retrieved from https://www.sebi.gov.in

Sestanovic, M. (2015). Initial public offerings: Success factors for underwriters and investors. Journal of Finance and Investment Analysis, 4(3), 45–60. https://doi.org/10.2139/ssrn.2754266

SIDBI. (2013). MSME sector: Performance and potential. SIDBI report on MSME sector, 2013. https://msme.gov.in/sites/default/files/ANNUALREPORT-MSME-2012-13P.pdf

Spence, M. (1973). Job market signaling. Quarterly Journal of Economics, 87(3), 355–374. https://doi.org/10.2307/1882010

Sundarasen, S. D., Khan, A., & Rajangam, N. (2018). Signalling roles of prestigious auditors and underwriters in an emerging IPO market. Global Business Review, 19(1), 69–84. https://doi.org/10.1177/0972150917749283

Welch, I. (1989). Seasoned offerings, imitation costs, and the underpricing of IPOs. Journal of Finance, 44(2), 421–449. https://doi.org/10.1111/j.1540-6261.1989.tb05064.x

World Bank. (2020). SMEs finance: Improving SMEs’ access to finance and finding innovative solutions to unlock sources of capital. https://doi.org/10.1596/978-1-4648-1406-7

Zhang, Y. (2008). The financial leverage effect on long-term IPO performance. Journal of Corporate Finance, 14(1), 28–45. https://doi.org/10.1016/j.jcorpfin.2008.10.004