Review of Professional Management

Search

Search

Ritu Sapra1  , Promila Bhardwaj2 , Rishabh Gupta3 and Shivani Abrol4

, Promila Bhardwaj2 , Rishabh Gupta3 and Shivani Abrol4

Affiliation: Department of Commerce, Dyal Singh Evening College, University of Delhi

1 Department of Commerce, University of Delhi, India

2 Dyal Singh Evening College, University of Delhi, India

3 Shaheed Bhagat Singh College, University of Delhi, India

4 Zakir Husain Delhi College, University of Delhi, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

India has a three-tier federal tax structure involving central, state and local municipal bodies, which collect funds from the taxpayers so as to meet its public spending and expenditure needs. The Indian taxation system has its traces in ancient India as well, wherein taxes were used to pay in the form of gold coins, cattle, grains, etc. In order to remove the complexity of the Indian tax system, a series of tax reforms have been introduced by the government from time to time. The main objective of the article is to examine the effect of personal income tax reforms on taxpayers. The article adopts a primary data collection method having a sample size of 250 respondents chosen from Haryana, Delhi and Delhi NCR. The ANOVA is applied for the analysis of the data. The findings of the article revealed that the income tax structure is still complicated despite reforms introduced by the government based on the recommendations of various tax reform committees. Further, it is found that taxpayers are satisfied with both their tax liability and the time allowed to them for paying off their taxes. It has been concluded that giving extra incentives to honest taxpayers will have a positive impact on the overall tax revenue.

Income tax structure, personal income tax reform, tax liability, tax revenue

Introduction

It is a subject of a common belief that taxes on income are of recent origin, but a close study of the historical record shows that taxes on income in some form or other were levied even in ancient times as well. A study of the ancient manuscripts Manusmriti, Rig Veda, Atharva Veda, Puranas and Arthshashtra, depicts that everyone has to pay tax, be it in cash or kinds like agricultural produce, silver, gold coins, cattle, or grains, and the ones who cannot pay taxes in cash or kind were required to work free for one day a month for the State (Prasad, 1987). It is clearly mentioned in Kautilya Arthashastra that everyone has to pay tax, whether they are poor or rich, like agriculturists were paid 1/6th of their grains grown and merchants were allowed to pay 1/10th of their sovereign dues (Kautilya, 2017, 1951, p. 67).

The foundation of the modern tax system in India, which was intellectualised by Sir James Wilson during British rule in 1860, was mainly based on Kautilya’s Arthashastra. After independence, the Government of India also followed the basic principles of Kautilya Arthashastra, which was considered to be the first authoritative text on public finance, administration, and fiscal laws in India. The tax structure in India was multifaceted, considering the length and breadth of India. Several income tax committees and commissions were constituted in the past for the simplification and rationalisation of tax structure, such as the Income Tax Investigation Commission (1948), Taxation Enquiry Commission (1954), Kaldor Committee (1956), Direct Taxes Administration Enquiry Committee (1959) and many more. However, the major attempt in the Indian Tax System took place in 1961 with the enactment of the new Income Tax Act, 1961. Presently, India has a three-tier federal tax structure involving central, state, and local municipal bodies. To remove the complications in the Indian tax system, three main bodies are constituted: that is, the Central Board of Direct Taxes (CBDT), the Central Board of Excise and Customs (CBEC), and the Central Board of Indirect Taxes & Customs (CBIC).

Fjeldstad and Raker (2003) in their empirical work found that many low-income countries face a trilemma with respect to taxation in Sub-Saharan Africa. The study concluded that, though there is undoubtedly a scope is available for improved fiscal and financial management in the public sector in the sample countries, as well as improved coordination between the different levels of government. But attempts to squeeze additional revenues from poorly designed taxes may exacerbate the negative effects of the tax system on the economy and society in general. Highlighting a slightly different view, Jensen and Di Gregorio (2017) supported Turnover Tax (TOT) and Pay as You Earn (PAYE) for personal income tax in Zambia, especially for firms with employees which depict that being a source of revenue, tax needs to be compulsory charge by the government and it’s non-compliance would result in tax evasion and tax avoidance (Alabede et al., 2011; Keen & Smith, 2007; Kesselman, 2001; Lymer & Oats, 2009; Phiri & Kabaso, 2012; Uremadu & Ndulue, 2011). However, Personal income tax is one of the major attractive sources of revenue than indirect taxes (Ahmad & Stern, 1983). The government is making amendments and reforms to make the tax structure simple, rational and generate high returns. The studies relating to tax reforms fail to show the effect of personal income tax reforms on taxpayers. There is no such study that measures the impact of personal income tax reforms on simplification & rationalisation of tax structure with high incentives to honest taxpayers.

Thus, the present article is an attempt to analyse the effect of personal income tax reforms on taxpayers. The study would also try to suggest and recommend workable suggestions to make the personal income tax reforms a successful process.

Literature Review

Gnangnon (2023) examined the effect of the shadow economy on tax reforms in developing countries. The study found that the shadow economy has its effect on various tax policies with tax revenue mobilisation and also reduces the dependency on international trade, also observed by Atkin and Donaldson (2022), Akitoby et al. (2020) and Schneider and Buehn (2018). Gupta and Jalles (2022) studied the tax reforms and their effect on income distribution, especially in developing countries. The study concluded that for faster reduction of the inequality, there should be highly effective implementation of tax reforms, but when the economy is growing steadily, with slow growth.

Alinaghi and Reed (2021) examined the effects of taxes on growth for OECD countries by using meta-analysis. The study found that an increase in taxes resulted in the reduction of deficit, which shows tax-positive fiscal policies increase to fund fecund investment or vice versa.

Nguyen et al. (2021) observed the impact of individual income and consumption taxes in the UK and found that substituting from an income to a consumption tax base has affirmative effects on progression. Further, consumption taxes do not significantly affect incentives to work and investments that are crucial for confirming economic growth in the long run. Delgado et al. (2020) found that removing deductions from the personal income tax system in the Andean region would have a less positive impact on tax revenue and put one step forward towards more sustainable and justifiable fiscal policies in this region.

Mertens and Olea (2018) studied the effect of marginal tax rates on an individual’s income. The study concluded that cuts in the tax rate for the top 1% not only have a constructive effect on other income groups but also increase the inequality between income groups. Zidar (2019) found that there is an affirmative association between tax cuts and employment growth, as it is mainly determined by tax cuts for lower-income groups and concluded that the impact of tax cuts for the top 10% on employment growth is small. Islam (2001) examined that if Asian developing countries want high economic growth, then such countries may have to simplify in tax systems and reduce their tax rates. Toye (2000) also found the same results in his study and suggested that a big-bang approach to reform produces a highly unpredictable and damaging impact on the economy of developing countries. To avoid these damages, economic reforms have to be actively managed. Gupta (2009) analysed that personal income tax reforms, like reduction in marginal tax rates, reduction in tax slabs, and increasing compliance, resulted in an increase in the number of assessees and tax revenue. The study concluded the favourable effect of tax reforms and is also found to be supported by Agarwal (1991) and Dalvi and Ansari (1986). Das-Gupta (2004) studied the economic theory of tax compliance and the effect of different forms of taxes on individual behaviour. The study concluded that a virtuous tax design and tax administration system resulted in low tax evasion & avoidance and high tax revenue. Rakshit (2003) critically examined tax reforms and the structure of the personal income tax rate in India and found that tax reforms measures have achieved remarkable growth over the period of more than a decade but unless and until the rate structure is designed in such a way so as to make it internationally comparable, all other efforts of tax reforms will not be able to bring in too much-added value in the area of tax compliance.

Rao (2000) studied the progression of the tax system in India since the early 1990s. The study also reviewed the new kinds of direct and indirect taxes, their returns and equity implications, and the achievements in their implementation. The author concluded that there have been a number of key fluctuations in tax systems in several countries during the last two decades for a variety of reasons. After eight years of reforms, only the revenue ratio of direct taxes is showing an upward trend, but a number of alarming features still remain in the tax system in India.

Chan et al. (1999) conducted a contradictory study and examined an evaluation of the impact of tax reform options in Vietnam, both at an aggregate level and household level in different expenditure classes. It was found that there are profits to Vietnam from indirect tax reform. But the redistributive effects associated with these reforms are large and tend to swamp the aggregate effects. Changes in Income tax has its effects on individuals like cuts in tax rates might inspire individuals to work, save, and invest, but it would result in a bigger federal budget deficit if these tax cuts were not financed by immediate spending cuts as observed by Mdanat et al. (2018), Gale and Samwick (2014), Macek (2015), Gemmell et al. (2011), Arnold et al. (2011), and Dennis et al. (2004).

Neog and Gaur (2020) also observed the long-run and short-run association between tax structure and the growth performance of Indian states and found that policymakers in India should give more focus on property tax with a reduction in income taxes.

Research Gap

Tax reforms introduced in 1991 have played an important role in revenue mobilisation and economic growth all over the world. The above studies discussed the effect of lowering the tax rate, increments in tax exemptions and deductions on revenue improvement and investment plans at large. Not even a single study has empirically shown the effect of personal income tax reforms on taxpayers. There is no study that measures the impact of personal income tax reforms on simplification & rationalisation of tax structure with high incentives to honest taxpayers, and reducing tax evasion & tax avoidance collectively. On the other hand, there is hardly any study which has studied such a large number of personal income tax reform variables that are covered in the present study. As Taxation is a wide area of research, hence, fresh and new studies are required to shed empirical light on this subject.

Objectives of the Study and Hypothesis

The objective of the current article is to examine the impact of personal income tax reforms on taxpayers.

Hypothesis

The major hypothesis is to be tested with a number of assumptions in support of the analysis, which are as follows:

H1: Personal Income Tax Reforms have a positive impact on taxpayers.

Methodology

Method and Tool

The study necessitates originality in work, so a well-structured questionnaire is equipped for original information. The questionnaire included 25 questions, of which 20 questions elicited the responses of respondents using a Likert 5 or 7-point scale, two questions were based on respondents’ descriptions, and the last three questions were optional for personal information of respondents. Both online (Google form) and offline modes (sent hard copy by post or by directly filling the questionnaire) are used for collecting data. Reliability test: Cronbach’s Alpha is applied for checking reliability on the questionnaire at a 0.05 significance level as used by Pettersen et al. (2005). Sunal et al. (2008) used Cronbach’s alpha at 0.5 to 0.72 with a total scale reliability of 0.85 as the final instrument of adequate internal consistency. Chu et al. (2010) suggested that Cronbach’s alpha at 0.7 and above is a good representation of a reliable test value is generally accepted. The Cronbach alpha value of the questionnaire used in the present study is 0.81. For the test of Homogeneity Levene Statistic is put into application. One-way ANOVA is applied for further analysis.

Sample Size

In order to cover all kinds of taxpayers in India, a prerequisite of a large sample size is essential, which is not practicable for a single researcher. Thus, in the current study, the respondents are chosen from Haryana, Delhi and Delhi NCR. The information is collected from 250 respondents. In the respondents, only taxpayers are included. Two hundred and fifty respondents were separated into four categories, that is, 50 businessmen, 50 private employees, 50 government employees and 100 professionals. In the category of Professionals- Chartered Accountants, Doctors, Advocates and Tax Advocates are included. Gurugram, Faridabad, Rohtak, Ghaziabad and Noida are chosen from Delhi NCR. In Delhi, a number of courts, that is, the High Court, Tis Hazari, Rohini Court and Dwarka Court are mainly chosen for the Professional category.

Research Design

A descriptive research design is espoused because the present article is analytical in nature. The respondent’s categories are used as a Factor variable, and their responses are considered as dependent variables.

Results and Discussion

Data are collected from 250 respondents, which requires the test of homogeneity. For the test of Homogeneity Levene Statistic is used, and one-way ANOVA is applied for further analysis. The respondent’s categories are used as a Factor variable, and their responses are considered as dependent variables.

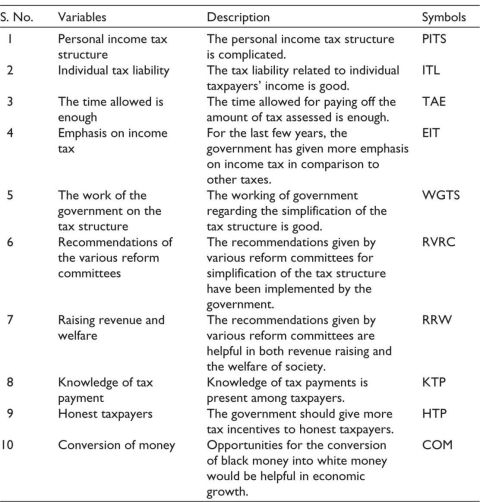

Table 1 gives the list of dependent variables. Symbols are assigned to variables so that the result discussion may become easy and simple.

Table 1. List of Dependent Variables for ANOVA.

Impact of Income Tax Reforms on Assessees in India

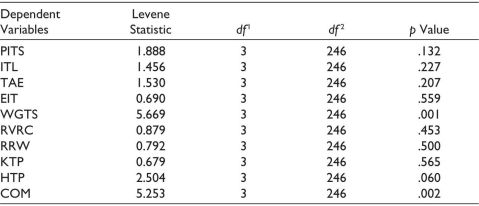

One of the assumptions of ANOVA is that there must be equal variance among variables. This supposition requires a test of homogeneity of variance between variables, as shown in Table 2, and it reveals a test of homogeneity of variances among dependent variables with the Levene Statistic as defined by Levine et al. (2009).

Table 2. Test of Homogeneity of Variances.

Note: *Significant at the 0.05 level.

Dependent variables which have a p value above .05 level of significance have equal variances (O’Donoghue, 2010). Equal variance is present among PITS, ITL, TAE, EIT, RVRC, RRW, KTP, and HTP, which show a p value higher than .05 significance level.

The study employs one-way ANOVA in order to know the F-ratio of these variables, as described in Table 3. Whereas, for WGTS and COM, the Levene statistic’s p value was found to be less than .05 level of significance, thereby indicating unequal variances in these variables. The study also adopted the Brown–Forsythe test for calculating ANOVA for WGTS and COM variables, which are disclosed in Table 4.

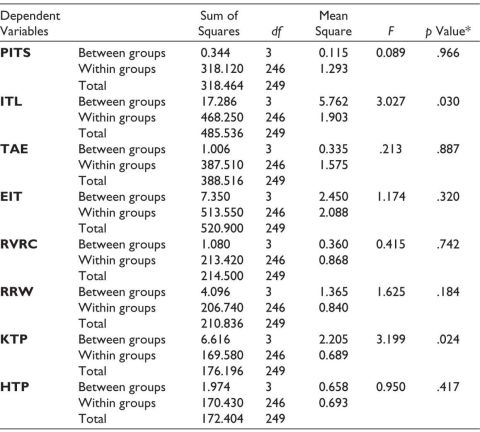

Table 3. ANOVA with Equal Variance.

Note: *Significant at the 0.05 level.

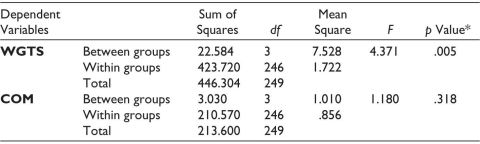

Table 4. Brown–Forsythe ANOVA with Not Equal Variance.

Note: *Significant at the 0.05 level.

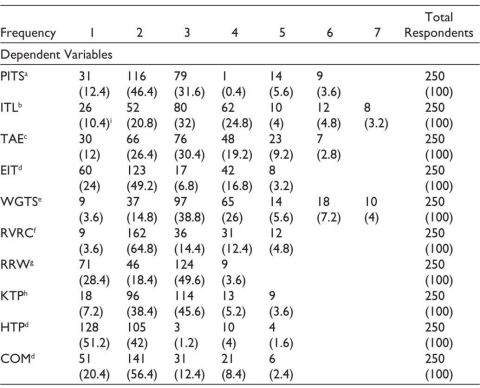

In Table 3, ITL (F = 3.027 & p = .030) and KTP (F = 3.199 & p = .024) demonstrate p < .05 level of significance thereby rejecting H1. It indicates that ITL, that is, the sense of tax liability related to the respondent’s income, is not much affected by reforms. Eighty respondents out of 250 respondents think their income tax liability is just fair, and 72 respondents sensed their income tax liability as average or even poor, as shown in Table 5. KTP means knowledge of tax payment is also not influenced by personal income tax reforms. As per the ANOVA results, knowledge of tax payment is not present among people, and they have a lack of acquaintance regarding the payment of taxes agreed by Damajanti and Karim (2017). The results of the study are in line with Palil (2010), who gave emphasis on the self-assessment system (SAS) and found that SAS improved tax collections for the tax authority without having an unacceptable detrimental effect on the other key characteristics of a well-designed tax system.

Table 5. Frequency.

Notes: a1: Very complicated, 2: complicated, 3: a little bit complicated, 4: cannot say, 5: quite simple, 6: simple, 7: very simple.

b1: Excellent, 2: good, 3: fair, 4: average, 5: poor, 6: very poor, 7: worst.

c1: More than enough, 2: quite enough, 3: enough, 4: average, 5: not enough, 6: not quite enough.

d1: Strongly agree, 2: agree, 3: neither agree nor disagree, 4: disagree, 5: strongly disagree.

e1: Excellent, 2: very good, 3: just up to the mark, 4: satisfactory, 5: not up to the mark, 6: poor, 7: very poor.

f1: Totally implemented, 2: partly implemented, 3: cannot say, 4: partly ignored, 5: totally ignored.

g1: Revenue raising only, 2: welfare of society, 3: both, 4: none of these.

h1: Well known, 2: known, 3: unaware, 4: ignored, 5: highly ignored.

1Percentage is shown in brackets.

Further, ITS (F = 0.089 & p = .966), TAE (F = 0.213 & p = .887), EIT (F = 1.174 & p = .320), RVRC (F = 0.415 & p = .742), RRW (F = 1.625 & p = .184) and HTP (F = 0.950 & p = .417) have value above 0.05 level of significance. The result shows that Personal Income Tax Reforms have a positive impact on assessees in India. Therefore, as per the result, the study found a complicated income tax structure, which was also explained by Creedy (2009) and Bernardi and Fraschini (2005). Carroll (1989) suggested the Alternative Distribution System (ADS), Mintz (1991) found auxiliary tax as useful, Sugarman (1948) studied inter-spouse transfers, and Bokil (2003) recommended transaction tax so as to decrease the complexity of the tax system and also increase the tax revenue.

Second, it is found that the time allowed for paying off the amount of tax assessed is enough, or in fact, in the survey, 68.8% of respondents out of the total, prop up with the statement, as shown in Table 5. On the same hand, EIT also shows significant results highlighting that the government is giving more emphasis on income tax in comparison to other taxes, which is also supported by Peters (1991). In the survey, 180 respondents also agreed with this proclamation. RVRC, that is, recommendations given by various reform committees, are partly implemented as represented by the F-ratio of RVRC in Table 3. The results are found to be in line with Rao (2000), who also found that recommendations given by tax reform committees are not properly implemented by the government. RRW shows recommendations given by tax reform committees are beneficial for the government in terms of increasing revenue, as well as it also supports welfare for society. Almost 50% of respondents were found to be in support of this statement, whereas 28.4% think that these recommendations are revenue-generating only; however, 18.4% were of the opinion that these are made only for the welfare of society. Ekpo and Ndebbio (1996) analysed that more exemptions in certain taxes and the elimination of some taxes like customs duties may solve the problem of economic crisis at the state level, or generate more revenue for the nation. Romer and Romer (2007) found a significant effect of tax changes on output. The analysis suggested that an exogenous tax increase of 1% of GDP lowers real GDP by roughly 3%.

Table 3 also shows government gives more tax incentives to honest taxpayers. It depicts that the government is very alert and always appreciates those who pay taxes honestly is also agreed by Brockmann et al. (2016), Ali et al. (2014) and Cummings et al. (2009). However, assesses require more tax benefits or incentives, and thus more incentives need to be given to those who pay tax sincerely; in fact, 93.2% of taxpayers taken under the survey say ‘yes’ regarding this assertion.

The study also included Brown–Forsythe test for WGTS and COM because of unequal variance among these variables. Table 4 shows the significant F-ratio for WGTS (F = 4.371 & p = .005), which means that the work of the government regarding the simplification of tax structure is not sufficient, but it requires multiple comparisons among respondents. On the other hand, Brown–Forsythe F-ratio for COM (F = 1.180 & p = .318) is not found to be significant, so it may be observed that if the government gives an opportunity to convert black money into white money, then it may help in boosting the economic growth of India. 192 respondents out of 250 respondents also support the observed avowal. Bonferroni multiple comparisons relating to ITL and KTP have publicised equal variance (Shao, 2003).

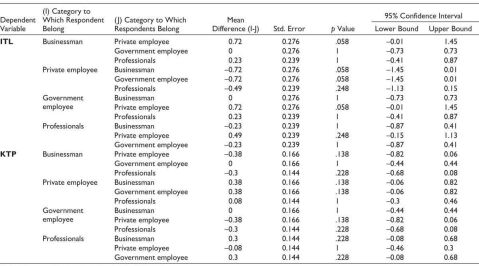

For ITL as well as KTP, as revealed in Table 6, there is no significant difference between Businessmen, Private Employees, Government Employees, and Professionals. Thus, it may be interpreted that all the respondents feel their tax liability related to their income is good, and also, the knowledge of tax payment is not present among taxpayers. In fact, 114 respondents think that people are unaware about their tax payments in the right way. Thus, there is a high degree of variation between respondents.

Table 6. Bonferroni Multiple Comparisons with Equal Variance.

Note: The mean difference is significant at the 0.05 level.

Table 7 shows Games–Howell multiple comparisons for the variable WGTS, which has depicted unequal variance. Games–Howell multiple comparison post-hoc test is used when any variable violates the assumption of homogeneity of variance. The Games–Howell test result for WGTS reveals that businessmen are significantly different from Professionals like Tax Advocates, Chartered Accountants, but are not different from Private and Government Employees. Whereas Private Employees are pronounced the same as the other three categories, on the other hand, Government Employees have the same opinion as given by Private Employees and Businessmen, but differ from Professionals. Professionals are going with Private Employees, but giving a dissimilar view from the rest of the respondents, as shown in Table 7.

Table 7. Games–Howell on WGTS Multiple Comparisons with Not Equal Variance.

.jpg/10_1177_09728686251363735-table7(1)__480x148.jpg)

Note: *The mean difference is significant at the 0.05 level.

Policy Implication

Apart from personal income tax among direct taxes, the government should also give other direct and indirect taxes top priority. The tax structure’s intricacy should be dropped. The government ought to create a scheme supporting tax incentives for regular and honest taxpayers. The tax base should also be broadened, the number of tax brackets dropped, and tax exemptions and deductions raised to inspire individuals to save and invest more.

Limitations of the Study

The present article has its own limitations with regard to the study area, data availability, respondents’ responses and other resources. Tax reforms are a wide area to study because they cover Direct and Indirect taxes. Direct Tax Reforms are also divided into Personal Income Tax, Corporate Income Tax and Wealth Tax, etc. It is not possible to cover all types of reforms in a single paper because of many reasons, like limited resources of the researcher and limited time, etc. So, the article is limited to Personal Income Tax Reforms only. Thus, the implications of the results may not be generalised beyond such tax reforms.

Conclusion

After having a discussion in the previous section, it may be concluded that the income tax structure in India is very complicated because people agree on the complexity of the income tax structure, as per the outcomes of the analysis, and it is also agreed by Creedy (2009) and Bernardi and Fraschini (2005). Taxpayers think that, as compared to other taxes, the government is giving more emphasis on income tax. Though the recommendations given by tax reform committees are helpful in both increasing revenue as well as the welfare of society but it has been seen from the analysis that such recommendations are partly implemented by the government. Honest taxpayers are demanding more tax benefits and tax incentives from the government. Results also show that assessees are satisfied with their tax liability, and they do not even have knowledge of tax payment. Taxpayers have a lack of acquaintance regarding the payment of taxes, supported by Damajanti and Karim (2017) and Adhikara et al. (2022). The working of the government is also not so good for rationalisation or simplification of tax structure, and moreover, not for raising national income.

Results depict that the reformed outlook of taxpayers, and frequent amendments in tax laws year after year, which are helpful in increasing tax revenue, also with declining tax evasion and tax avoidance. At last, personal income tax reforms may have a positive impact on Indian assesses.

The study may help to promote administrative and managerial support for personal income tax reforms and embolden personal income tax reforms in the simplification and rationalisation of the tax structure in India. The article also suggests that the Government of India should encourage tax incentives for those taxpayers who pay their taxes on time and with honesty. There should be a lowering of personal income tax rates, widening the tax base, decreasing the number of tax slabs, and enlarging the tax exemptions and deductions to encourage taxpayers to save more and invest more. No doubt, the personal income taxes generate more revenue for the government, but the policymakers should take care of other taxes too, so that collectively the complexity of the tax structure may also result in high returns for the government, which ultimately helps in raising national income.

However, considering the present research work, the following empirical investigation could be taken in the future with respect to the simplification and rationalisation of the tax structure in India. Future research could also attempt to find out the impact of corporate income tax reforms on corporate tax assessees. Further, a comparative study may be conducted empirically between personal and corporate income tax reforms and their effects on assessees, involving more variables, so as to bring a comprehensive understanding of the attitude of assessees regarding the tax system in India.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iDs

Ritu Sapra https://orcid.org/0000-0002-7720-1471

Promila Bhardwaj https://orcid.org/0009-0003-6098-4718

Rishabh Gupta https://orcid.org/0000-0001-5663-596X

Shivani Abrol https://orcid.org/0000-0002-5729-5319

Adhikara, M. A., Maslichah, N. D., & Basyir, M. (2022). Taxpayer compliance determinants: Perspective of theory of planned behavior and theory of attribution. International Journal of Business and Applied Social Science, 8(1), 395–407.

Agarwal, P. K. (1991). Income inequality and elasticity of personal income tax. Economic & Political Weekly, July 20, 1991. https://www.jstor.org/stable/41498470

Ahmad, E., & Stern, N. (1983). The evaluation of personal income taxes in India. Retrieved, 22 August 2025, from https://www.researchgate.net/publication/297318800_The_evaluation_of_personal_income_taxes_in_India

Akitoby, B., Baum, A., Hackney, C., Harrison, O., Primus, K., & Salins, V. (2020). Tax revenue mobilization episodes in developing countries. Policy Design and Practice, 3(1), 1–29. https://doi.org/10.1080/25741292.2019.1685729

Alabede, J. O., Ariffin, Z. Z., & Idris, K. M. (2011). Individual taxpayers’ attitude and compliance behaviour in Nigeria: The moderating role of financial condition and risk preference. Journal of Accounting and Taxation, 3(5), 91–104. http://www.academicjournals.org/JAT

Ali, M., Fjeldstad, O. H., & Sjursen, I. H. (2014). To pay or not to pay? Citizens’ attitudes toward taxation in Kenya, Tanzania, Uganda, and South Africa. World Development, 64, 828–842.

Alinaghi, N., & Reed, W. R. (2021). Taxes and economic growth in OECD countries: A meta-analysis. Public Finance Review, 49(1), 3–40. https://doi.org/ 10.1177/1091142120961775

Arnold, J. M., Bassanini, A., & Johansson, Å. (2011). Tax policy for economic recovery and growth. Economic Journal, 121(550), F59–F80. https://doi.org/10.1111/j.1468-0297.2010.02415.x

Atkin, D., & Donaldson, D. (2022). The role of trade in economic development. In Handbook of international economics (Vol. 5, pp. 1–59). Elsevier. https://doi.org/ 10.1016/bs.hesint.2021.11.001

Bernardi, L., & Fraschini, A. (2005). Tax system and tax reforms in India. Retrieved, 22 August 2025, from http://polis.unipmm.it/pubbl/RePEc/uca/ucapdv/fraschini51.pdf

Bokil, A. (2003). Tax reforms in India. The Indian Journal of Commerce, 56(2–3), 95–105.

Brockmann, H., Genschel, P., & Seelkopf, L. (2016). Happy taxation: Increasing tax compliance through positive rewards? Journal of Public Policy, 36(3), 381–406. https://doi.org/10.1017/S0143814X15000331

Carroll, S. (1989). Taxing wealth. Journal of Post Keynesian Economics, 12(1), 49–69.

Chan, N., Ghosh, M., & Whalley, J. (1999). Evaluating tax reform in Vietnam, using general equilibrium methods. Retrieved, 22 August 2025, from http://www.economics.uwo.ca/econref/WorkingPapers/researchreports/wp/1999/wp9906.pdf

Chu, S., Ritter, W., & Hawamdeh, S. (2010). Managing knowledge for global and collaborative innovations. World Scientific Publishing.

Creedy, J. (2009). The personal income tax structure: Theory and policy. Retrieved, 22 August 2025, from http://www.economics.unimelb.edu.au/downloads/wp/wp09/1063.pdf

Cummings, R. G., Martinez-Vazquez, J., McKee, M., & Torgler, B. (2009). Tax morale affects tax compliance: Evidence from surveys and an artefactual field experiment. Journal of Economic Behavior & Organization, 70(3), 447–457.

Dalvi, M. Q., & Ansari, M. M. (1986). Measuring fiscal performance of the central and the state governments in India: A study in resource mobilization. Indian Economic Journal, 33(4), 107–110.

Damajanti, A., & Karim, A. (2017). Effect of tax knowledge on individual taxpayers compliance. Economics & Business Solutions Journal, 1(1), 1–19. https://core.ac.uk/download/pdf/228864377.pdf

Das-Gupta, A. (2004). The economic theory of tax compliance with special reference to tax compliance costs. Retrieved, 22 August 2025, from http://www.nipfp.org.in/working_paper/wp13.pdf

Delgado, M. C. D., Jara, H. X., Oliva, N., & Torres, J. (2020). Simulating personal income tax reforms and fiscal gains in the Andean region. Inter-American Development Bank. Retrieved, 22 August 2025, from https://publications.iadb.org/publications/english/document/Simulating-Personal-Income-Tax-Reforms-and-Fiscal-Gains-in-the-Andean-Region.pdf

Dennis, R., Hamilton, D., Arnold, R., Demiroglu, U., Foertsch, T., Lasky, M., Nishiyama, S., Ozanne, L., Peterson, J., Russek, F., Sturrock, J., & Weiner, D. (2004). Macroeconomic analysis of a 10 percent cut in income tax rates. Congressional Budget Office. Retrieved, 22 August 2025, from https://www.cbo.gov/sites/default/files/cbofiles/ftpdocs/54xx/doc5485/2004-07.pdf

Ekpo, A. H., & Ndebbio, J. E. (1996). Fiscal operations in a depressed economy: Nigeria, 1960–90. International Development Research Centre. Retrieved, 22 August 2025, from http://idl-bnc.idrc.ca/dspace/bitstream/10625/13171/1/104735.pdf

Fjeldstad, O. H., & Rakner, L. (2003). Taxation and tax reforms in developing countries: Illustrations from sub-Saharan Africa. Chr. Michelsen Institute. Retrieved, 22 August 2025, from http://www.cmi.no/publications/file/?1551=taxation-and-tax-reforms-in-developing-countries

Gale, W. G., & Samwick, A. A. (2014). Effects of income tax changes on economic growth. Brookings Institution. Retrieved, 22 August 2025, from https://www.brookings.edu/wp-content/uploads/2016/06/09_effects_income_tax_changes_economic_growth_gale_samwick.pdf

Gemmell, N., Kneller, R., & Sanz, I. (2011). The timing and persistence of fiscal policy impacts on growth: Evidence from OECD countries. The Economic Journal, 121(550), F33–F58. https://doi.org/10.1111/j.1468-0297.2010.02414.x

Gnangnon, S. K. (2023). Effect of the shadow economy on tax reform in developing countries. Economies, 11(3), 96. https://doi.org/10.3390/economies11030096

Gupta, A. (2009). The trends and responsiveness of personal income tax in India. Indira Gandhi Institute of Development Research. Retrieved, 22 August 2025, from http://www.igidr.ac.in/pdf/publication/PP-062-29.pdf

Gupta, S., & Jalles, J. A. (2022). Do tax reforms affect income distribution? Evidence from developing countries. Economic Modelling, 110, 105804. https://doi.org/10.1016/j.econmod.2022.105804

Islam, A. (2001). Issues in tax reforms. Asia-Pacific Development Journal, 8(1), 1–12.

Jensen, A., & Di Gregorio, E. (2017). A study on personal income tax. International Growth Centre. Retrieved, 22 August 2025, from https://www.theigc.org/wp-content/uploads/2019/01/Jensen-and-Di-Gregorio-2017-Final-report.pdf

Kaldor, N. (1956). Indian tax reform: Report of a survey. Ministry of Finance, Government of India. https://elibrary.sansad.in/server/api/core/bitstreams/51161156-47ec-4967-b53f-774519cf76b4/view

Kautilya. (2017). Kautilya’s Arthasastra (R. Shamasastry, Trans.). Mysore Press. (Original work published ca. 321–286 BCE; Original published 1951). Retrieved, 22 August 2025, from https://archive.org/details/in.gov.ignca.900/page/n67/mode/2up?q=tax

Keen, M., & Smith, S. (2007). VAT fraud and evasion: What do we know, and what can be done? SSRN. Retrieved, 22 August 2025, from https://doi.org/10.2139/ssrn.964339

Kesselman, J. R. (2001). Payroll taxes in the finance of social security. In A. Berry (Ed.), Labor market policies in Canada and Latin America: Challenges of the new millennium. Springer. https://doi.org/10.1007/978-1-4757-3347-1_6

Levine, D. M., Krehbiel, T. C., Berenson, M. L., & Viswanathan, P. K. (2009). Business statistics: A first course (4th ed.). Pearson Education South Asia.

Lymer, A., & Oats, L. (2009). Taxation: Policy and practice (16th ed.). Fiscal Publications. http://www.accenture.com

Macek, R. (2015). The impact of taxation on economic growth: Case study of OECD countries. Review of Economic Perspectives, 14(4), 309–328. https://doi.org/10.1515/revecp-2015-0002

Mathai, J. (1954). Taxation enquiry commission. Ministry of Finance, Government of India. https://elibrary.sansad.in/server/api/core/bitstreams/7c2be29b-1352-4cbebe32-96208c6db7ce/view

Mdanat, M. F., Shotar, M., Samawi, G., Mulot, J., Arabiyat, T. S., & Alzyadat, M. A. (2018). Tax structure and economic growth in Jordan, 1980–2015. EuroMed Journal of Business, 13(1), 102–127. https://doi.org/10.1108/EMJB-11-2016-0030

Mertens, K., & Olea, J. L. M. (2018). Marginal tax rates and income: New time series evidence. The Quarterly Journal of Economics, 133(4), 1803–1884. https://doi.org/10.1093/qje/qjy008

Mintz, J. M. (1991). The role of wealth taxation in the overall tax system. Canadian Public Policy, 17(3), 248–263.

Neog, Y., & Gaur, A. K. (2020). Tax structure and economic growth: A study of selected Indian states. Economic Structures, 9, 38. https://doi.org/10.1186/s40008-020-00215-3

Nguyen, A. D. M., Onnis, L., & Rossi, R. (2021). The macroeconomic effects of income and consumption tax changes. American Economic Journal: Economic Policy, 13(2), 439–466. https://doi.org/10.1257/pol.20170241

O’Donoghue, P. (2010). Research methods for sports performance analysis. Routledge.

Palil, R. M. (2010). Tax knowledge and tax compliance determinants in self-assessment system in Malaysia (Doctoral dissertation, University of Birmingham). Retrieved, 22 August 2025, from http://etheses.bham.ac.uk/id/eprint/1040/

Peters, B. G. (1991). The politics of taxation: A comparative perspective. Blackwell.

Pettersen, K. I., Reikvam, A., & Stavem, K. (2005). Reliability and validity of the Norwegian translation of the Seattle Angina Questionnaire following myocardial infarction. Quality of Life Research, 14(3), 883–889. http://www.jstor.org/stable/4038837

Phiri, C. S., & Kabaso, P. N. (2012). Taxation of the informal sector in Zambia. Retrieved, 22 August 2025, from https://media.africaportal.org/documents/taxation_of_the_informal_sector_in_zambia.pdf

Prasad, B. (1987). Principles of taxation in ancient India (pp. 66–110). Mittal Publications. https://books.google.co.in/books?id=D7Ql9mX3gqUC&pg=PP7&source=gbs_selected_pages&cad=1#v=onepage&q&f=false

Rakshit, D. (2003). Tax reforms in India and rate structure of personal income tax. The Indian Journal of Commerce, 56(2–3), 130–145.

Rao, M. G. (2000). Tax reforms in India: Achievement and challenges. Asia-Pacific Development Journal, 7(2), 59–74.

Romer, C. D., & Romer, D. H. (2007). The macroeconomic effects of tax changes: Estimates based on a new measure of fiscal shocks. Retrieved, 22 August 2025, from https://eml.berkeley.edu/~cromer/RomerDraft307.pdf

Schneider, F., & Buehn, A. (2018). Shadow economy: Estimation methods, problems, results and open questions. Open Economics, 1(1), 1–29. https://doi.org/10.1515/openec-2017-0001

Shao, J. (2003). Mathematical statistics (2nd ed., pp. 519–520). Springer Science + Business Media, LLC.

Sugarman, N. A. (1948). Estate and gift tax equalization: The marital deduction. California Law Review, 36(2), 223–280.

Sunal, D. W., Wright, E., & Sundberg, C. (2008). The impact of the laboratory and technology on learning and teaching science K-16 (Vol. 3, pp. 126–127). IAP–Information Age Publishing Inc.

Toye, J. (2000). Fiscal crisis and fiscal reforms in developing countries. Cambridge Journal of Economics, 24(1), 21–44. https://www.jstor.org/stable/23600379

Tyagi, M. (1959). Direct taxes administration enquiry committee. Ministry of Finance, Government of India.

Uremadu, S. O., & Ndulue, J. C. (2011). A review of private sector tax revenue generation at local government level: Evidence from Nigeria. Journal of Public Administration and Policy Research, 3(6), 174–183. http://www.academicjournals.org/jpapr

Varadachariar, S. (1948). Income tax investigation commission. Ministry of Finance, Government of India.

Zidar, O. (2019). Tax cuts for whom? Heterogeneous effects of income tax changes on growth and employment. Retrieved, 22 August 2025, from https://www.journals.uchicago.edu/doi/pdf/10.1086/701424